Collections

Expert-curated collections organized by topic and theme.

Market (Overall)

280 documentsReports in the Market (Overall) category.

Market (Mobile)

175 documentsReports in the Market (Mobile) category.

Sensor Tower · 2023

ReportThe Mobile Economy and Digital Ad Space in 2022 and Beyond: An Analysis of the Global Trends Shaping the Mobile and Digital Advertising Industry

This analysis examines the global mobile economy and digital advertising landscape throughout 2022 and into early 2023, utilizing proprietary market intelligence data from the App Store and Google Play. While global app installs have slowed following the initial pandemic surge, they remain significantly above 2019 levels. Mobile games continue to be the primary driver of downloads globally, exceeding 50 billion installs in 2022, though the utilities category has recently emerged as a significant growth leader, particularly in emerging markets like India. A major shift occurred in 2022 as global consumer spending on mobile games declined for the first time, falling to $79 billion. This downturn was particularly pronounced on Android devices, which saw a 7 percent revenue drop driven by high inflation and the lifting of COVID-19 restrictions. Japan experienced the most significant contraction, with game revenue falling by $3.2 billion. Conversely, the entertainment category has become a primary engine for revenue growth, with spending on apps like TikTok, HBO Max, and Disney+ reaching record highs. In the United States, entertainment spending doubled compared to 2019 levels, while in Japan, a manga reader app became the top-grossing title for the first time, displacing traditional gaming leaders. The digital advertising sector reached $28 billion across North America and major European markets in the fourth quarter of 2022. While established platforms like Facebook maintain the largest market share, TikTok has emerged as the fastest-growing ad channel, recording a 60 percent quarterly increase in U.S. ad spend. Facing headwinds from Apple’s privacy changes and reduced marketing budgets, many developers are pivoting toward subscription models and diversified monetization strategies. Looking forward, the reopening of China and the high smartphone penetration growth in Africa are identified as critical factors for the next phase of global mobile adoption.

Sensor Tower · 2024

ReportSoutheast Asian Mobile Game Market Insights 2024

The report examines Southeast Asian mobile gaming in 2024, focusing on download volumes, in‑app purchase (IAP) revenue, genre performance, country dynamics, and top titles. In the first half of 2024, downloads rose 3.4 % to 4.2 billion, with Google Play accounting for 91 %. IAP revenue increased 3.4 % to $1.16 billion, though a slight 3 % decline in overall revenue was noted compared to the prior half‑year; Google Play contributed 57 % of total earnings. Mid‑core, simulation, arcade, puzzle and lifestyle games dominated downloads (67 % of total), while strategy and RPG titles captured 47 % of revenue, despite modest declines in downloads. Sports games experienced a 39 % revenue surge, representing 9 % of total market income. Indonesia remains the largest download hub, growing 10 % in January‑August 2024 and contributing over 41 % of regional downloads; Thailand follows with a 10 % revenue rise. The top downloaders include Garena Free Fire, Mobile Legends: Bang Bang, Roblox, and Honor of Kings, the latter achieving a 175 % month‑over‑month jump in July after its Southeast Asian launch. Revenue leaders are Mobile Legends: Bang Bang, eFootball 2024, Garena Free Fire, and Roblox, with eFootball showing a 90 % revenue spike. The analysis draws on Sensor Tower’s estimated download and IAP data from the App Store and Google Play, excluding ad revenue and third‑party sales.

Country Reports

42 documentsReports in the Country Reports category.

Dataspelsbranschen · 2021

ReportSwedish Games Industry 2021

The Swedish games industry experienced a transformative period of growth in 2020, reaching a record revenue of EUR 3.3 billion. This 43% increase significantly outpaced global market trends, marking the sector's twelfth consecutive year of profitability. The landscape is increasingly defined by corporate consolidation and international expansion, with 667 active companies and 19 listed entities commanding a combined market capitalization of EUR 10.7 billion. Major players such as Embracer Group, King, and Mojang have transitioned Sweden from a target for foreign acquisition into a dominant global investor, with Swedish-owned firms now employing more personnel abroad than domestically across 126 international studios. Despite this commercial success, the industry faces a critical bottleneck regarding skilled labor. While domestic employment rose to over 6,500 positions, a severe talent shortage and a cumbersome work permit process hinder further expansion. These systemic issues are compounded by a lack of early-stage financing and tax incentives for smaller developers, who must also navigate digital regulations often tailored for larger tech platforms. Furthermore, while Swedish-developed titles like Minecraft and Candy Crush have achieved over six billion downloads, the sector continues to grapple with internal demographic challenges. Women currently represent only 21% of the workforce, and over 100 companies remain entirely male-operated, prompting a surge in diversity initiatives aimed at leveling the playing field. Geographically, while Stockholm remains the primary hub with over 4,000 employees, regional development clusters and educational programs are expanding throughout Sweden to support the growing ecosystem. The industry is also pivoting toward long-term sustainability, addressing workplace culture and the environmental implications of energy-intensive cloud gaming. As the sector matures, its primary challenges have shifted from achieving market viability to managing rapid globalization, securing specialized talent, and fostering a more inclusive and sustainable professional environment.

Interactive Software Federation of Europe · 2022

ReportVideo Games – A Force for Good: Europe's Video Game Industry

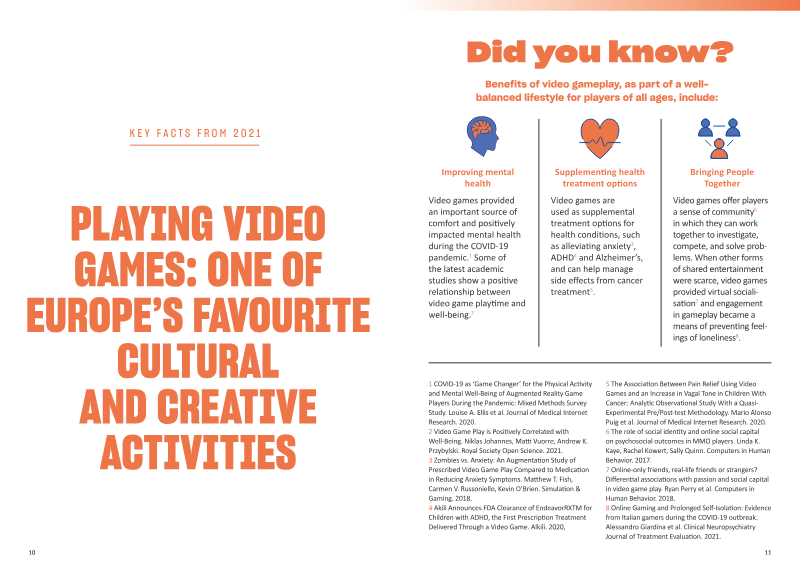

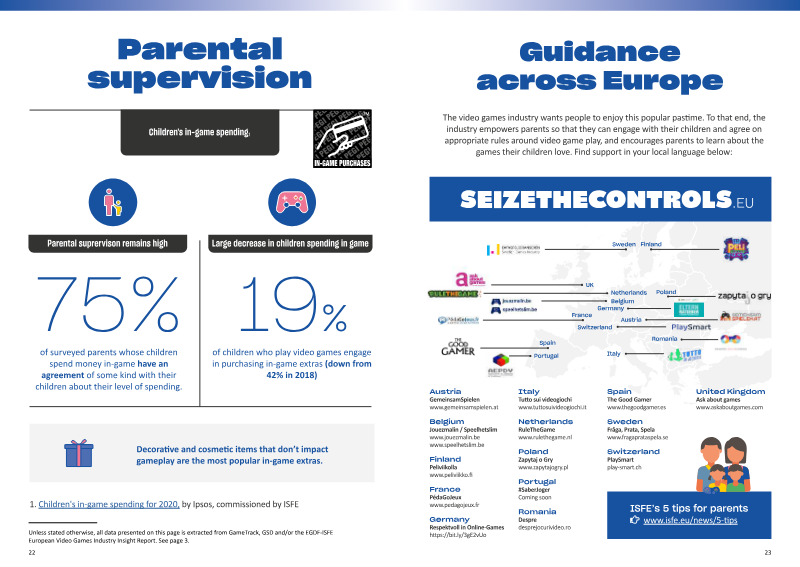

This analysis provides a comprehensive overview of the European video games industry as of 2021, detailing its economic impact, demographic reach, and social contributions. Jointly produced by ISFE and EGDF, the findings highlight a sector that remained stable following the pandemic-induced surge of 2020, maintaining a market value of €23.3 billion across key European territories. The industry supports a significant workforce, employing over 98,000 people across Europe, with 74,000 located within the EU. Data is primarily sourced from Ipsos, GameTrack, and GSD, covering major markets including France, Germany, Italy, Spain, and the United Kingdom. The demographic data reveals that video gaming is a mainstream cultural activity, with 52% of the European population aged 6 to 64 participating. The average player age is 31.3 years, and women represent nearly 48% of the total player base. While engagement remains high, average weekly playtime returned to pre-pandemic levels of nine hours. The digital ecosystem dominates the market, accounting for 81% of total revenue, driven largely by app-based gaming and in-game extras. A significant portion of the analysis focuses on industry responsibility and social impact. It underscores the effectiveness of the PEGI age rating system and the prevalence of parental control tools, noting a sharp decline in unsupervised in-game spending by minors. Furthermore, the industry is positioned as a driver for digital literacy and mental well-being, with specific initiatives targeting STEM education for girls and climate change through the Green Game Jam. The report concludes that the sector is a vital component of Europe’s digital economy, increasingly recognized for its pedagogical value and commitment to diversity and environmental sustainability.

eSports & Streaming

16 documentsReports in the Esports & Streaming category.

Newzoo · 2022

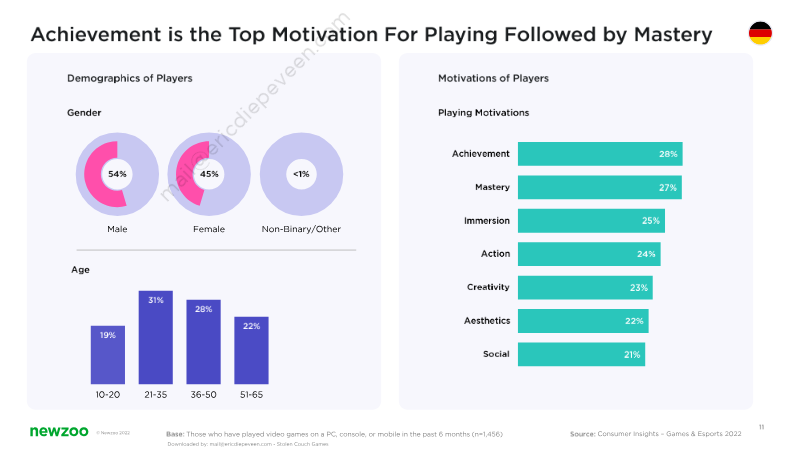

ReportConsumer Insights: Games and Esports 2022

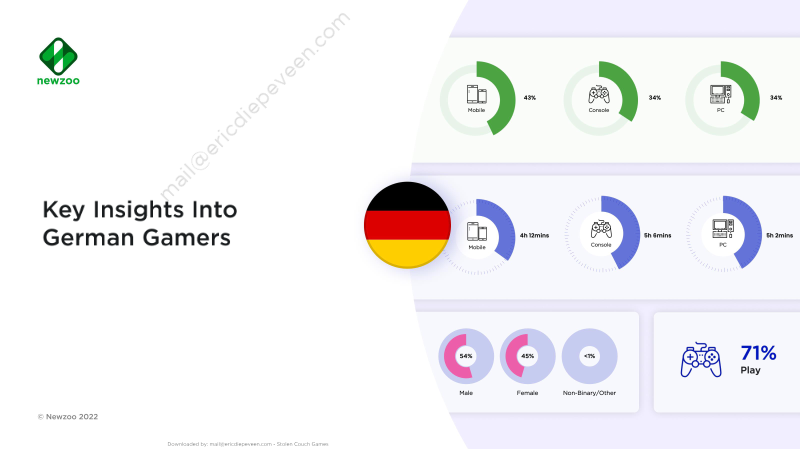

The Consumer Insights: Games and Esports 2022 report provides a comprehensive analysis of global gaming behaviors, motivations, and market engagement. The primary purpose of the research is to equip game developers, publishers, and industry stakeholders with actionable data to benchmark titles, understand player demographics, and identify growth opportunities across 36 diverse international markets. By examining over 100 key performance indicators, the analysis offers a granular view of how players interact with PC, console, and mobile platforms. The research is underpinned by a robust methodology, drawing on survey data from over 75,000 consumers worldwide. The findings highlight distinct engagement patterns, such as the prevalence of specific gaming personas—notably Time Fillers and Mainstream Gamers—and the interplay between playing and viewing habits. For instance, data from the German market indicates that while playing remains the dominant activity, a significant portion of the population also engages with gaming video content and esports. Furthermore, the report identifies key drivers for consumer spending, noting that price sensitivity, the desire for exclusive content, and social connectivity are primary motivators for financial investment in games. Covering a broad geographic scope that includes North America, Europe, Latin America, the Middle East, and the Asia-Pacific region, the report serves as a strategic tool for navigating the complex global gaming landscape. By synthesizing metrics such as monthly active users, daily active users, and lifetime player value, the analysis facilitates a deeper understanding of the motivations driving player behavior. Ultimately, the findings emphasize that a nuanced approach to audience segmentation and platform-specific engagement is essential for companies seeking to reach and retain diverse gaming populations in an increasingly competitive entertainment market.

Stream Hatchet · 2021

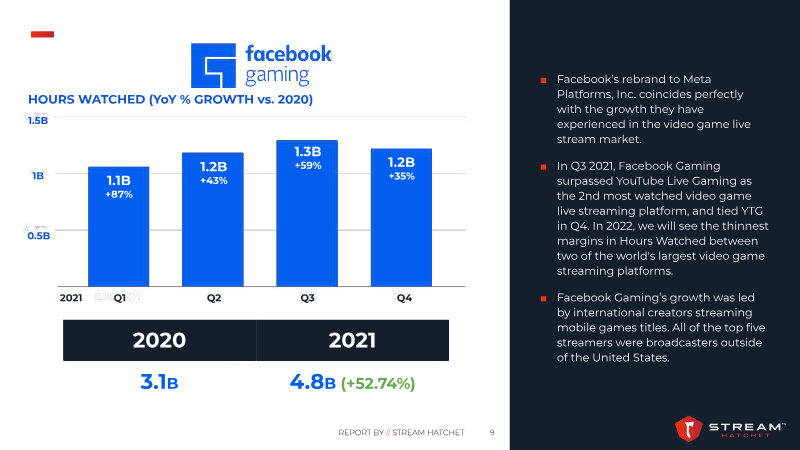

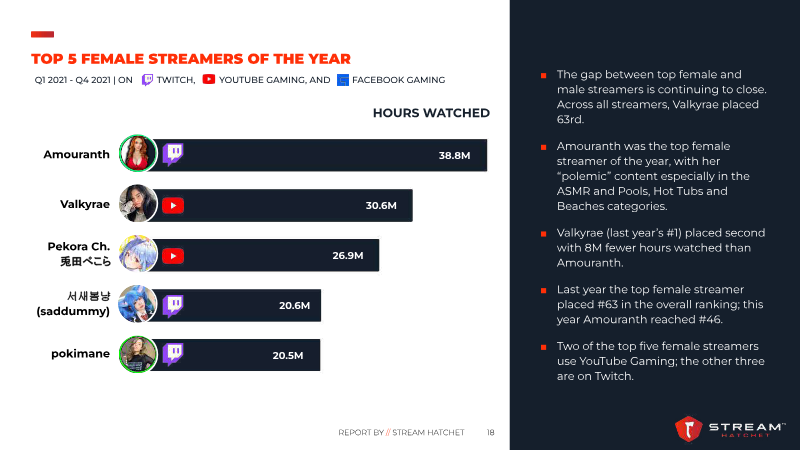

ReportVideo Game Streaming Trends Report 2021

The 2021 Video Game Streaming Trends Report provides a comprehensive analysis of the global live streaming landscape, documenting the industry's transition from a pandemic-driven surge to a permanent fixture in global pop culture. The report evaluates performance across major western platforms—Twitch, YouTube Gaming, and Facebook Gaming—throughout the 2021 calendar year. By aggregating data on hours watched, concurrent viewership, and creator demographics, the analysis highlights the evolving nature of the creator economy and the persistent challenges regarding inclusivity within gaming communities. Key findings indicate that total video game streaming watch time grew by 21% year-over-year, reaching 28.7 billion hours. Twitch maintained its market dominance, accounting for 71% of total hours watched, while Facebook Gaming experienced significant growth, eventually tying YouTube Gaming for the second-most-watched platform by the end of the year. The report identifies a shift toward mobile gaming, noting that titles like Garena Free Fire and PUBG Mobile are driving massive engagement, particularly in Asian markets. Furthermore, the data reveals that the creator economy remains highly concentrated; only 1.2% of influencers generate nearly 16% of total subscription and bit revenue on Twitch, with 93% of the platform's creators classified as micro-influencers. The report also addresses critical social issues, specifically the gender gap in streaming. Despite efforts by major platforms to implement inclusive policies, female representation among the top 200 creators remains low at 5%, a marginal increase from previous years. The analysis concludes that while the streaming industry has matured beyond its initial lockdown-era growth, success for creators now requires long-term consistency, with top-tier status often taking an average of five years to achieve. The findings are based on proprietary data analytics and industry insights provided by Stream Hatchet, focusing on western-facing platforms and global gaming trends.

Financial Reports

32 documentsReports in the Financial Reports category.

Krafton · 2025

FinancialFY2025 1Q Earning Results

The primary aim of the presentation is to convey KRAFTON’s financial performance and strategic direction for its PUBG intellectual property and related franchise initiatives during the first quarter of 2025. Consolidated results prepared under Korean IFRS show record quarterly revenue of KRW 874.2 billion, a 31.3 percent increase year‑on‑year, driven by strong growth across PC, mobile and console platforms. Operating profit reached KRW 457.3 billion, up 47.3 percent YoY, while adjusted EBITDA rose to KRW 505.1 billion, reflecting a 33.4 percent improvement. Net profit improved modestly to KRW 371.5 billion (+6.6 percent YoY) but fell 24.4 percent quarter‑on‑quarter due to foreign‑exchange effects and higher non‑operating expenses. Platform‑level analysis reveals mobile revenue of KRW 532.4 billion, up 32.3 percent YoY and 47.0 percent QoQ, while PC revenue climbed to KRW 323.5 billion, a 32.8 percent YoY rise. Console contributions increased 14.2 percent YoY to KRW 13.1 billion. The “Others” category declined sharply, falling 39.2 percent YoY, indicating a shift toward core PUBG services. Personnel costs grew 22.2 percent YoY, reflecting expanded development and publishing activities. Strategically, KRAFTON emphasizes expanding the PUBG franchise through new titles across diverse genres, including a life‑simulation spin‑off and an extraction‑RPG, with early‑access releases targeting 1 million copies sold within a week. The company is integrating advanced AI features such as on‑device language models to enhance gameplay, and it is strengthening its publishing foothold in India via collaborations on the BGMI platform and acquisition of a leading cricket game IP. These initiatives aim to sustain long‑term fan engagement, diversify revenue streams, and position PUBG as a globally influential, evergreen IP.

Everplay · 2024

FinancialAnnual Report and Financial Statements 2024

Everplay Group PLC, formerly known as Team17 Group PLC, achieved a significant financial recovery and strategic reorganization during the 2024 fiscal year. Following a loss in 2023, the Group returned to profitability with a profit before tax of £25.3 million and record revenues of £166.6 million, representing 5% year-over-year growth. This performance significantly outpaced the broader gaming market’s 0.6% growth, driven primarily by a resilient back catalogue that contributed 86% of total revenue. While the core Team17 publishing division saw a slight revenue decline, the astragon simulation and StoryToys edutainment divisions grew by 22% and 25% respectively, highlighting the success of the Group’s diversified multi-divisional structure. The Group’s financial position strengthened considerably, ending the period with £62.9 million in cash and a 97% operating cash conversion rate. This liquidity supports a transition toward high-quality first-party IP, which now accounts for 37% of total sales, and provides capital for future M&A activity. Operational highlights include the management of over 140 active titles and a subscription base for StoryToys exceeding 337,000 active users. Strategically, the Group underwent a major leadership transition and corporate rebranding in early 2025 to reflect its evolved identity as a platform-agnostic developer and publisher. Governance and sustainability remained central to the 2024 agenda, with the Group reporting significant progress in diversity and environmental targets. Women now hold approximately 50% of leadership roles, and the mean gender pay gap was reduced by over 7%. Despite recording impairments related to the underperformance of the US-based mobile unit "The Label," the Group reinstated a dividend of 2.7 pence per share. Looking toward 2025, the Group maintains a positive outlook with a pipeline of at least ten new title launches and a continued focus on lifecycle management and disciplined cost control.

Investment & M&A

8 documentsReports in the Investment & M&A category.

Drake Star Partners · 2026

ReportGlobal Gaming Report Q1 2026

LOS ANGELES | SAN FRANCISCO | NEW YORK | LONDON | PARIS | MUNICH | BERLIN | DUBAI PROVEN TRACK RECORD IN GAMING M&A AND GROWTH FINANCING ADVISORY PROVEN TRACK RECORD IN GAMING M&A AND GROWTH FINANCING ADVISORY MICHAEL METZGER JULIAN RIEDLBAUER Linkedin - Free social media icons MOHIT PAREEK Linkedin - Free social media icons MICHAEL METZGER JULIAN RIEDLBAUER ...

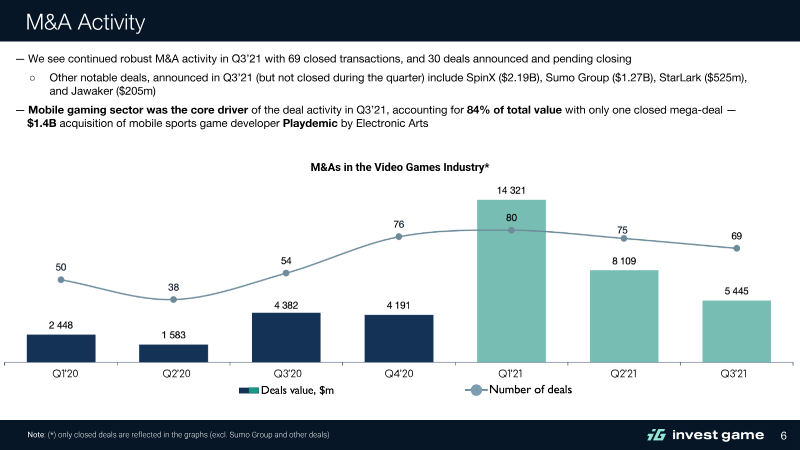

InvestGame · 2021

ReportGaming Deals Activity 2021: Smashing Previous Records

The global video game industry achieved unprecedented financial expansion in 2021, characterized by a surge in capital deployment that solidified the sector as a primary target for institutional and strategic investors. Total deal value reached $80.4 billion across 967 transactions, representing a 2.5-fold increase over the previous year. This growth was underpinned by a robust environment for mergers and acquisitions, which accounted for nearly half of the total transaction volume, alongside a significant intensification in early-stage venture capital funding. The investment landscape was defined by a shift toward emerging technologies and high-growth segments. Most notably, blockchain-integrated gaming experienced an explosive 68-fold year-over-year increase in deal value, signaling a fundamental pivot in investor interest toward decentralized gaming models. Simultaneously, the mobile gaming segment continued to serve as a critical engine for growth, attracting substantial capital as strategic players like Tencent maintained aggressive acquisition strategies to consolidate market share and secure long-term intellectual property. These findings reflect a broader trend of heightened investor confidence in the long-term viability of the gaming ecosystem. By spanning a diverse range of deal structures—including public offerings, venture capital, and strategic M&A—the 2021 activity highlights a maturing industry that is increasingly capable of attracting massive capital inflows. This record-breaking performance underscores the industry's transition from a niche entertainment sector to a dominant force in the global digital economy, setting a new benchmark for future investment activity across all major gaming segments.

Market (PC & Console)

34 documentsReports in the Market (PC & Console) category.

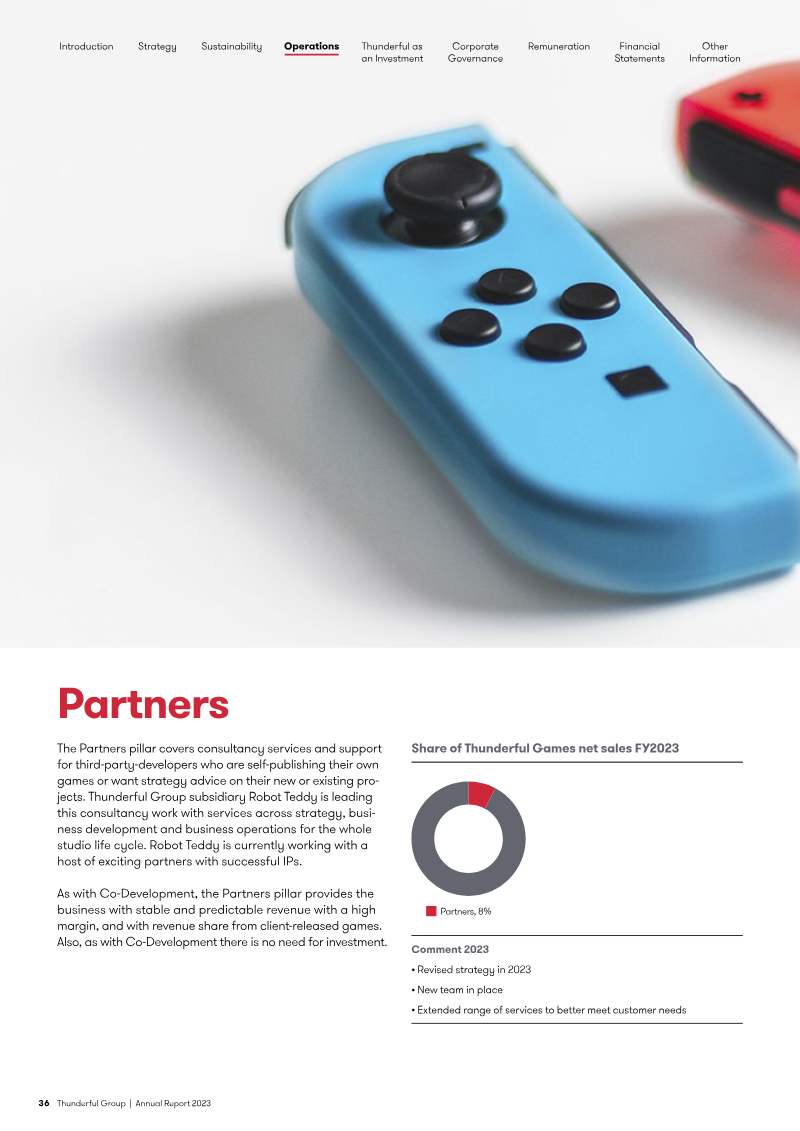

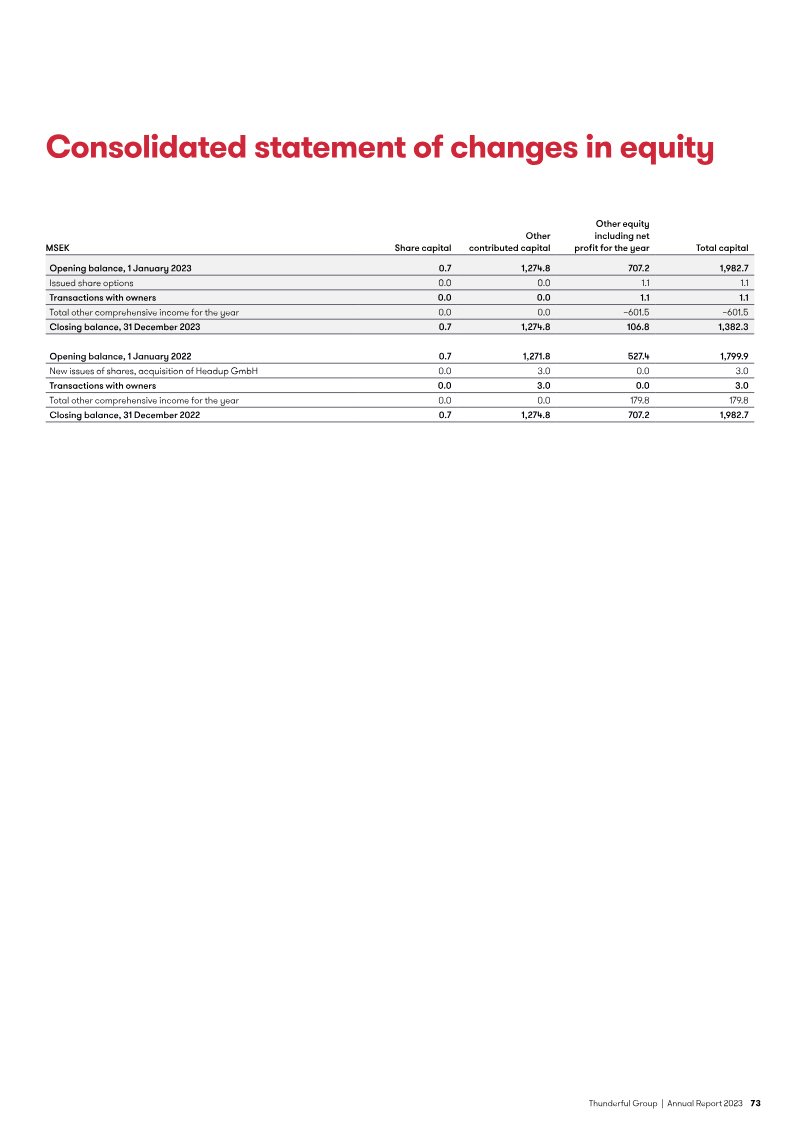

Thunderful · 2023

FinancialThunderful Group Annual Report 2023

Thunderful Group’s 2023 fiscal year was defined by a significant strategic pivot and financial restructuring aimed at addressing historical over-investment and stabilizing a volatile balance sheet. The Group reported net sales of SEK 2.8 billion, a 4.6% year-over-year decline, and swung to a substantial operating loss of SEK 609.3 million. This downturn was primarily driven by SEK 838.9 million in depreciation, amortization, and impairments—most notably a SEK 500.4 million goodwill impairment within the Games segment. In response, leadership initiated a major restructuring program to divest its legacy distribution businesses, including Bergsala and Amo Toys, for SEK 630 million to amortize debt and focus exclusively on high-potential "AA" game development. The geographic and operational scope of the Group remains centered in the Nordics, with a consolidated structure of 30 companies. While the Distribution segment, anchored by a long-standing partnership with Nintendo, contributed SEK 2.4 billion in net sales, the Group’s future thesis rests on the Games segment. This division released 15 titles in 2023, including SteamWorld Build, and maintains a pipeline of 29 projects. To ensure long-term viability, the Group implemented a rigorous "Go-ahead" approval process and a restructuring plan targeting annual cost savings of SEK 90–110 million. Sustainability and governance remained core priorities during this transition. The Group expanded its workforce to 519 employees, maintained a 26.5% female workforce, and integrated ESG metrics across its logistics and development cycles. Despite a 64.5% decline in share price and the expiration of unexercised incentive programs, the Group secured necessary bank waivers and maintained a positive cash flow from operating activities of SEK 315.4 million. Moving forward, the Group aims for 25% annual organic growth in its Games segment, supported by a centralized leadership team under CEO Martin Walfisz.

Newzoo · 2022

ReportGlobal Cloud Gaming Report: 2022

The global cloud gaming market is entering a phase of maturity, with 2022 revenues projected to reach $2.4 billion supported by a base of 31.7 million paying users. Despite high-profile shifts in the ecosystem, such as the closure of Google Stadia, the industry remains fundamentally viable as major platform holders like Xbox and PlayStation successfully integrate cloud technology to complement traditional hardware. This evolution is primarily driven by the increasing seamlessness of services, which allows players to bypass local hardware limitations and access high-end content instantly across a diverse range of devices. Market projections indicate a robust growth trajectory through 2025, at which point paying users are expected to reach 86.9 million and annual revenues are forecasted to climb to $8.2 billion. This expansion is underpinned by the global rollout of 5G networks, improved service profitability, and the emergence of cloud infrastructure as the foundational backbone for the metaverse. Strategic scaling by major players, including Alibaba’s YuanJing, aims to support massive concurrent user experiences while overcoming the constraints of physical hardware on a global scale. Technological innovation in infrastructure-as-a-service models is further accelerating adoption by lowering costs for both telecom operators and consumers. By utilizing GPU edge computing within carrier networks, providers can deliver high-quality gaming experiences with reduced latency. The industry is also refining its internal metrics and consumer segmentation, distinguishing between cloud-enabled and cloud-native content to better target diverse player demographics. These developments suggest that cloud gaming is transitioning from a niche technology into a central pillar of the broader interactive entertainment landscape.

Marketing

40 documentsReports in the Marketing category.

Sensor Tower · 2021

ReportMobile Ad Creative Report: August 2021

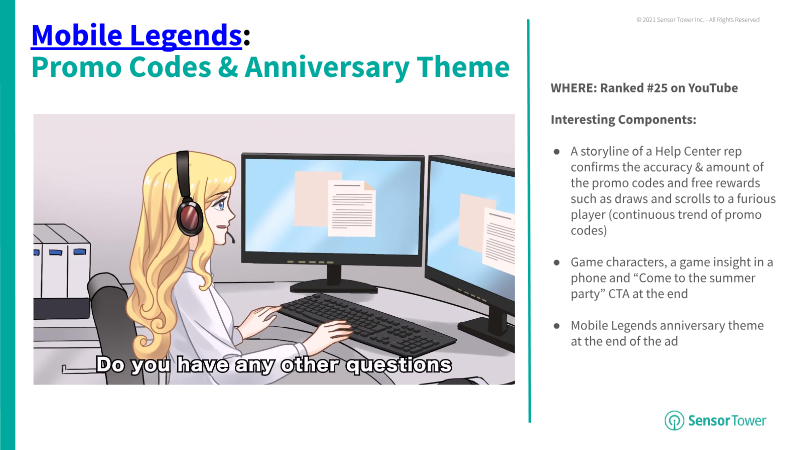

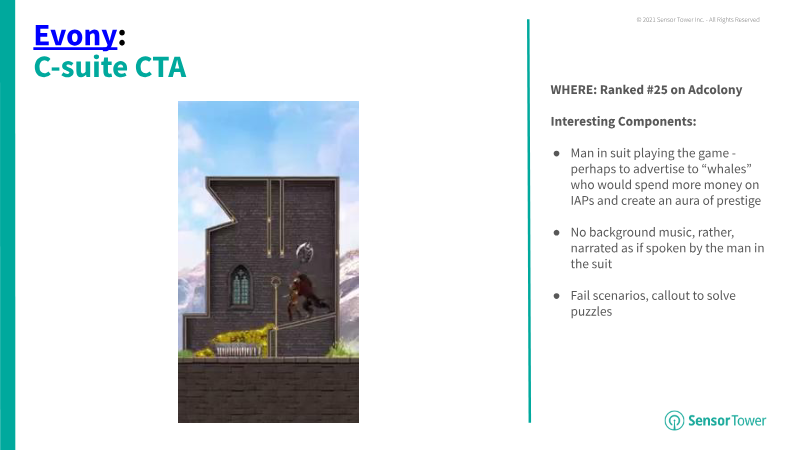

Mobile gaming creative trends in August 2021 centered on humanizing digital experiences and leveraging high-profile cultural partnerships. Analysis of top-performing ads across platforms like YouTube, Instagram, Snapchat, and Facebook reveals a heavy reliance on real-world celebrities, particularly musicians. Notable examples include Garena Free Fire featuring DJs Dimitri Vegas & Like Mike as playable characters and Call of Duty Mobile partnering with artist Ozuna. These collaborations often utilize cinematic storytelling and high-fidelity animations to bridge the gap between gaming and mainstream entertainment. The industry continues to utilize specific psychological triggers and visual formats to drive engagement. Fail-state elements, where ads demonstrate a player losing a level to pique viewer interest, remain prevalent in titles like Royal Match and Evony. Additionally, hyper-casual games are increasingly adopting popular music soundtracks and expressive callouts to appeal to younger demographics on Snapchat. Other emerging visual trends include split-screen layouts, the use of Bitmojis, and "search bar" call-to-actions that visually demonstrate how to find the app in stores. Geographically, the findings cover global releases with specific performance data from major ad networks including ironSource, Applovin, and Vungle. The scope encompasses diverse genres, from mid-core shooters and RPGs to hyper-casual and puzzle games. Methodology involves ranking creatives based on their performance and visibility across social media and ad networks during the August 2021 period. Conclusions suggest that successful creatives are moving away from pure gameplay footage in favor of narrative-driven content, anniversary themes, and interactive elements like Buzzfeed-style quizzes or "Christmas in July" promotions.

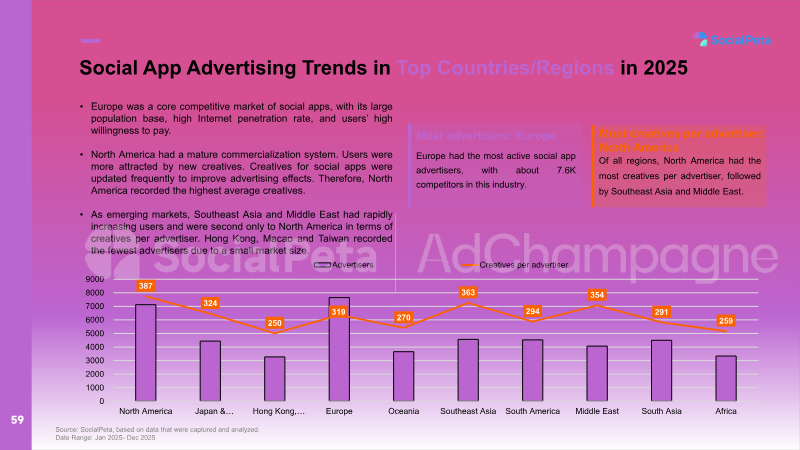

SocialPeta · 2021

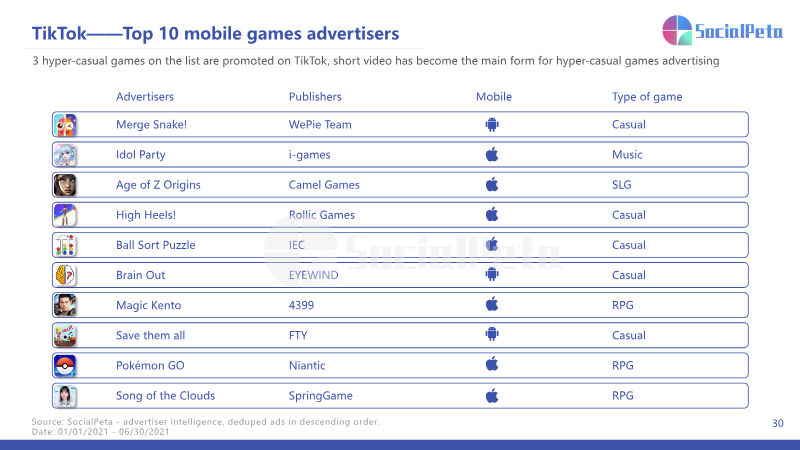

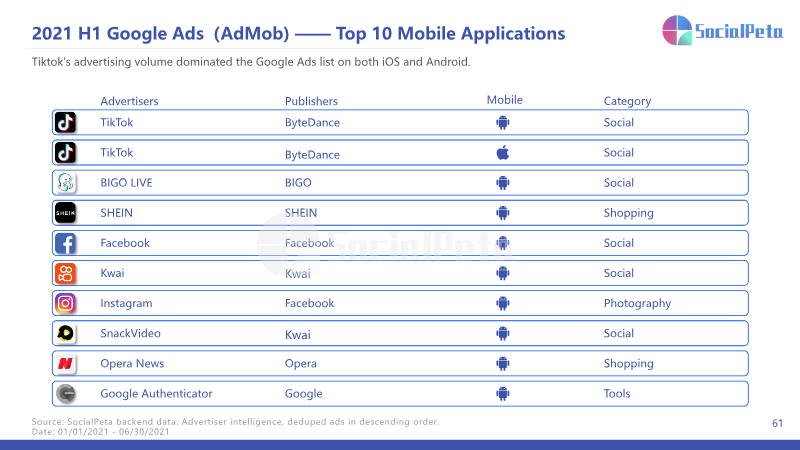

Report2021 H1 Global Mobile App Marketing Whitepaper

The global mobile marketing landscape experienced a massive surge in activity during the first half of 2021, characterized by a 108% year-on-year increase in advertising creatives totaling over 19 million. This growth was primarily driven by hard-core gaming titles and a significant expansion in the non-game sector, where creatives rose 38% to 47.6 million. Despite this volume increase, Apple’s IDFA policy changes caused a 13% decline in the share of iOS creatives, shifting more focus toward Android platforms. Geographically, the United States remained the largest advertising market, while Oceania emerged as the fastest-growing region for non-game advertisers. Chinese companies solidified their global dominance during this period, accounting for 70% of top-charting mobile game media buying and over 25% of the total global market share. These developers maintained a particularly strong presence on major social platforms, representing 100% of the top ten advertisers on Facebook’s News Feed. However, this increased competition contributed to a sharp rise in acquisition costs, with Facebook’s average CPC and CPM both climbing 128% year-over-year. RPG and Puzzle genres led in total creative volume, while Strategy games exhibited the highest media buying intensity per advertiser. Marketing strategies have evolved toward high-engagement, "snackable" short-form video content and influencer-led campaigns to combat rising costs and privacy-related tracking challenges. In the gaming sector, creative tactics shifted toward live-action footage and gameplay extensions, while non-game apps—particularly in the education and shopping sectors—capitalized on pandemic-related lifestyle shifts. As the industry navigates the post-IDFA era, the integration of high-quality in-game ads and diverse creative formats has become essential for maintaining user retention and driving monetization across both domestic Chinese and international markets.

Country & Regional Reports

39 documentsReports in the Country & Regional Reports category.

App Annie · 2021

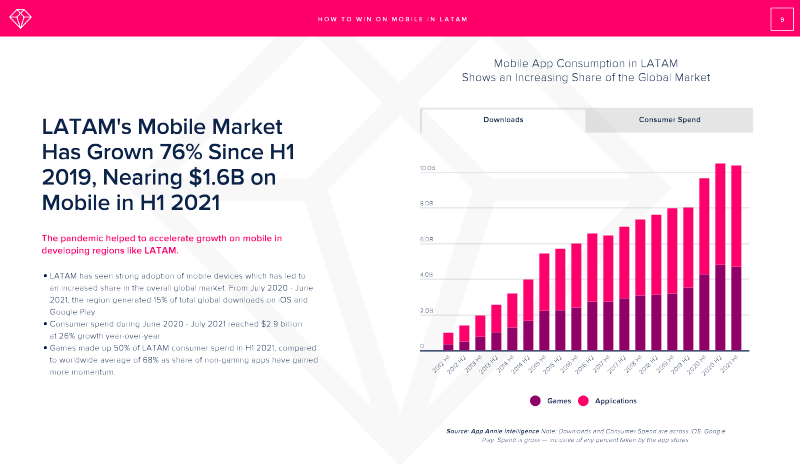

ReportHow to Win on Mobile in LATAM: 2021

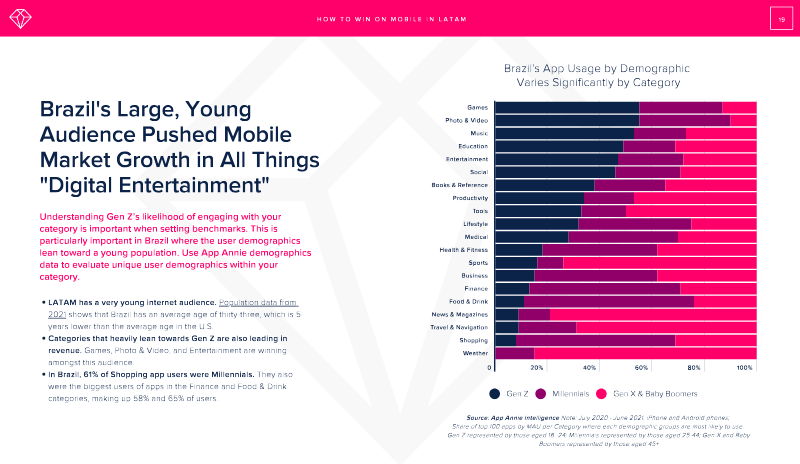

The analysis focuses on Latin America’s mobile ecosystem from July 2020 to June 2021, revealing a region that has accelerated digital adoption and monetization amid the pandemic. Mobile downloads surged 76 % year‑on‑year, reaching roughly 21 billion across iOS and Google Play, while consumer spend climbed 26 % to $2.9 billion. Android dominates downloads (≈89 %) yet iOS retains a higher spend share, commanding 56 % of total consumer expenditure. Brazil and Mexico together generate 73 % of regional downloads, with Brazil’s per‑capita income lower than Uruguay’s but still driving significant spend growth. Gaming remains a key driver, accounting for 50 % of LATAM consumer spend—below the global average of 68 %. Brazil leads in both downloads (4.6 billion) and revenue ($557 million), with Chile showing a strong spend‑to‑download ratio. Non‑gaming verticals such as Finance, Shopping, and Entertainment also expanded; finance apps grew 36 % YoY in Brazil, while shopping app downloads rose 30 %. Entertainment became the largest spend category in four of six major markets, reflecting limited Smart TV penetration and a shift to mobile streaming. User engagement metrics underscore high daily time spent, with Brazil averaging 5.4 hours per user and Mexico 4.8 hours—up 32 % and 36 % respectively from two years prior. Social, tools, and business categories saw the largest increases in sessions and minutes, indicating opportunities for productivity and contactless payment solutions. Demographic analysis shows a youthful audience: 61 % of shopping app users in Brazil are Millennials, and Gen Z dominates photo‑video and entertainment segments. Overall, the report highlights LATAM as a high‑growth mobile market with distinct platform dynamics, strong gaming and finance opportunities, and an emerging preference for mobile‑first entertainment and productivity apps.

Adaverse · 2024

ReportState of Web3 in Saudi Arabia

Saudi Arabia has emerged as the dominant hub for Web3 investment in the Middle East and North Africa, capturing 51 % of Q1 2024 venture‑capital funding with $429 million across 163 deals. This concentration reflects a supportive ecosystem that blends proactive government initiatives, a growing pool of local founders, and active participation from international investors. The market is presently skewed toward consumer‑facing applications such as DeFi, GameFi and SocialFi, while foundational protocol development remains limited, highlighting a clear opening for infrastructure builders. Founders of Saudi‑based Web3 ventures underscore the rapid maturation of the sector, citing high‑profile partnerships—including Animoca Brands with NEOM, collaborations with Hedera, and alignment with Vision 2030—as catalysts for growth. Yet they identify three persistent barriers: inadequate user‑friendly interfaces, insufficient public and investor education, and ambiguous regulatory frameworks that impede both builder activity and funding cycles. Sector‑specific use cases—blockchain‑enabled freelance payments, Sharia‑compliant insurance, and localized NFT platforms—are viewed as primary drivers of mass adoption. Government commitment reinforces this trajectory, with $37.7 billion earmarked for esports and $13.3 billion for gaming, complemented by sizable venture funds such as Wa’ed’s $500 million vehicle and 500 Global’s $2.4 billion under management. Notable projects illustrate tangible impact: Tharawat Green Exchange aims to plant ten million trees by 2030, while Ticket Souq has generated $3.3 million in gross merchandise value, serving 36 k users across 55 events in ten countries. Stakeholders agree that clear, supportive regulation, robust education, and targeted technology investment are essential to translate this momentum into sustainable, high‑pay‑off outcomes for the kingdom’s burgeoning gaming, fintech, e‑commerce and proptech sectors.

Investment

0 documentsReports in the Investment category.

No documents in this collection yet.

People Management

7 documentsReports in the People Management category.

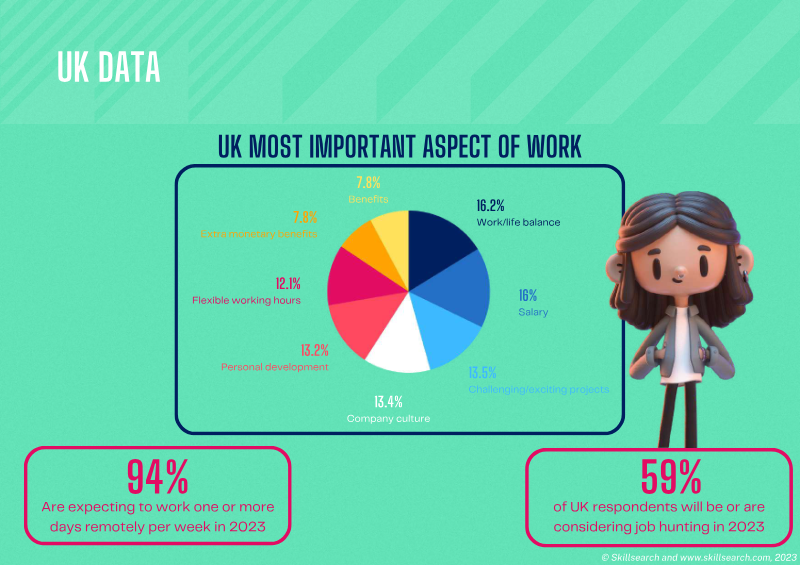

Skillsearch · 2023

ReportGames & Interactive Salary & Satisfaction Survey 2023

The 2023 Games & Interactive Salary & Satisfaction Survey establishes that financial compensation has emerged as the primary catalyst for professional mobility within the global gaming industry. Driven largely by the prevailing cost of living crisis, employees are increasingly prioritizing salary increases when evaluating career moves. While monetary remuneration remains the dominant factor, non-monetary benefits such as flexible working arrangements, private healthcare, and robust pension schemes are essential for talent retention. The data indicates a high degree of industry volatility, with a significant portion of the workforce—particularly among programmers and artists—actively considering new employment opportunities throughout the year. Geographically focused on the UK, Europe, and broader global markets, the findings underscore a fundamental shift in workplace expectations. Remote work has transitioned from a temporary accommodation to a standard requirement, with the vast majority of professionals now expecting at least one day of remote work per week. Despite this, a disconnect persists between employee needs and employer support. Many workers report inadequate institutional backing regarding mental health, neurodiversity accommodations, and financial pressures. Furthermore, project completion cycles serve as a major inflection point for retention, as employees frequently initiate job searches immediately following the conclusion of their current assignments. Ultimately, the industry faces a complex retention landscape where high mobility is tempered by a desire for stability and work-life balance. Although a large percentage of the workforce is open to changing employers, many candidates decline offers that fail to meet specific salary thresholds or project-based interests. To remain competitive, organizations must reconcile the demand for flexible, remote-first environments with the necessity of addressing the financial and psychological well-being of their staff, particularly as project-based turnover continues to threaten long-term team cohesion.

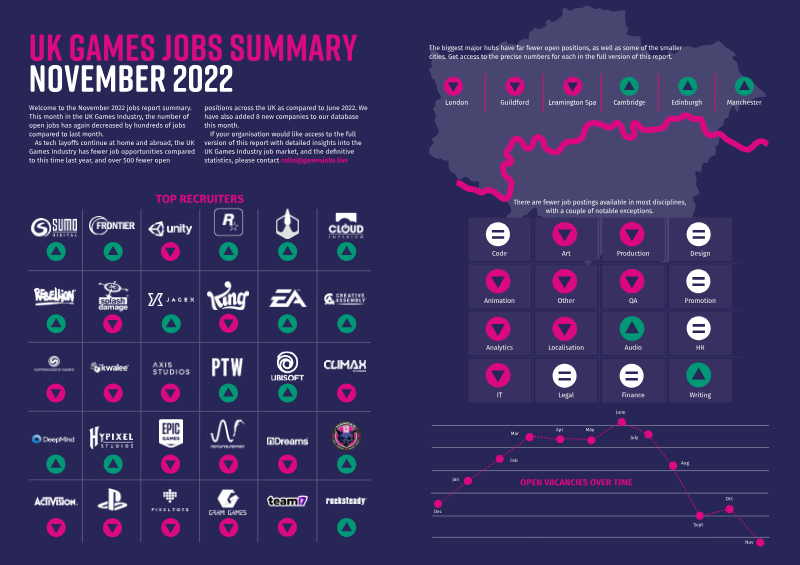

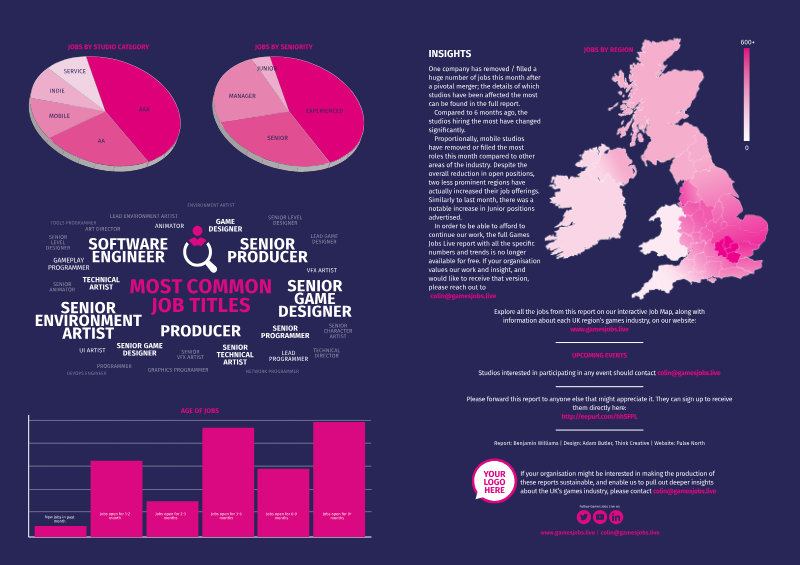

Games Jobs Live · 2022

ReportUK Games Jobs Summary: November 2022

The United Kingdom games industry experienced a notable contraction in recruitment activity during November 2022, continuing a downward trend observed throughout the second half of the year. Open vacancies decreased by several hundred positions compared to the previous month, leaving the market with over 500 fewer available roles than in June 2022. This decline aligns with broader global and domestic technology sector layoffs. While major development hubs such as London, Guildford, Leamington Spa, Cambridge, Edinburgh, and Manchester remain the primary centers for recruitment, these locations have seen a significant reduction in active job postings. The downturn has impacted various industry segments and disciplines unevenly. Mobile studios recorded the highest proportional reduction in open roles, often attributed to the fulfillment or removal of positions following major corporate mergers. Despite the general decline in volume, the market shows resilience in specific areas; two less prominent geographic regions bucked the national trend by increasing their job offerings. Furthermore, while senior and experienced roles remain prevalent, there was a recorded increase in advertised junior positions, suggesting a continued interest in developing entry-level talent despite broader economic headwinds. Data indicates that Software Engineers, Producers, and Senior Environment Artists are among the most sought-after titles. Programming, Art, and Design remain the dominant hiring categories, though most disciplines have seen a net loss in postings. The age of available jobs suggests a mix of immediate needs and long-term vacancies, with over 600 new jobs added in the month preceding the summary. This analysis is based on a comprehensive database of UK game studios, which expanded by eight new companies during this period, providing a representative snapshot of the hiring landscape across AAA, AA, mobile, indie, and service-based sectors.

Web3 & Blockchain

12 documentsReports in the Web3 & Blockchain category.

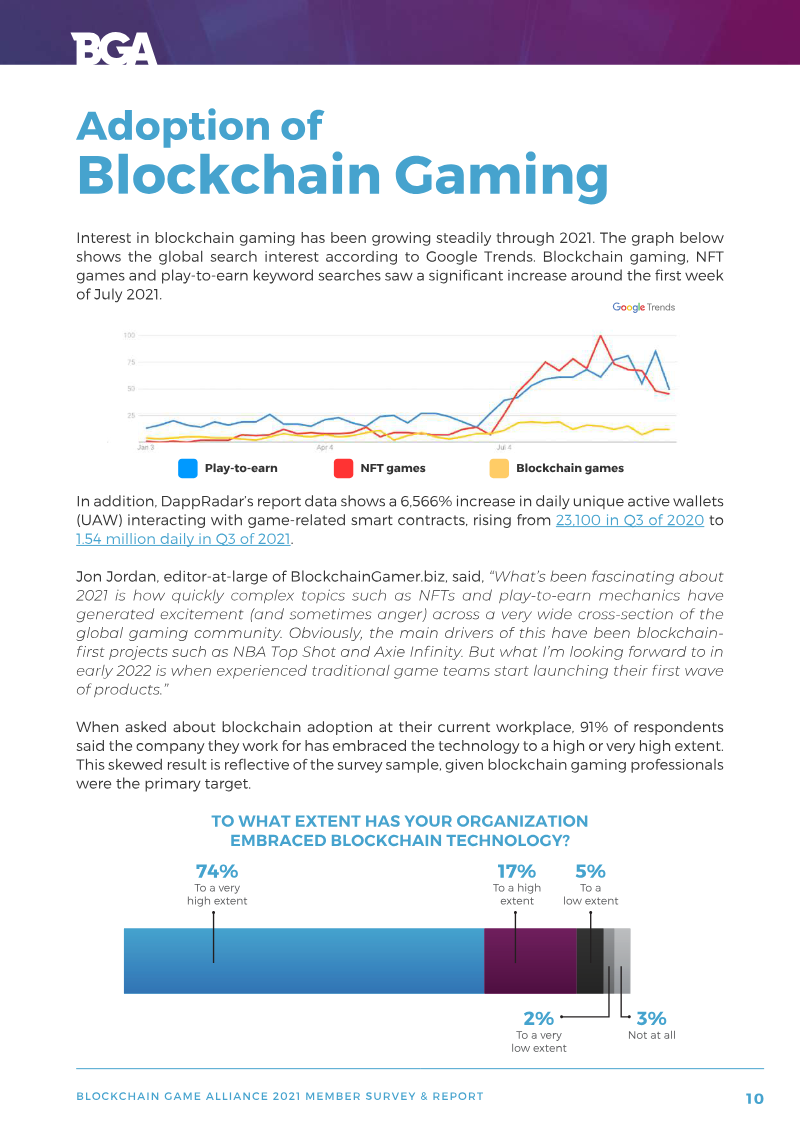

Blockchain Game Alliance · 2021

ReportMember Survey & Report 2021

The blockchain gaming industry experienced a transformative period of expansion in 2021, driven primarily by the emergence of play-to-earn mechanics and the implementation of true digital asset ownership. Industry professionals identify these features as the most significant catalysts for growth, with a vast majority anticipating that traditional gaming entities will integrate blockchain technology within the next two years. This momentum is further evidenced by approximately $4 billion in capital inflows from venture firms and decentralized autonomous organizations, signaling strong institutional confidence in the sector’s long-term viability. Despite this rapid financial and technological acceleration, the industry faces substantial structural headwinds. Regulatory uncertainty remains the most pressing concern for over half of the organizations operating in the space, followed closely by a general lack of public understanding regarding core blockchain concepts. Additionally, the sector must navigate technical challenges related to user-friendliness and a shortage of specialized engineering talent. While environmental sustainability has been a point of external criticism, the industry is actively transitioning toward carbon-neutral protocols and Proof of Stake networks to mitigate its ecological footprint. The ecosystem is characterized by a diverse and collaborative landscape that spans game studios, major traditional publishers like Ubisoft, and specialized firms in decentralized finance, legal, and infrastructure. While financial incentives have been the primary driver of initial adoption, long-term sustainability is widely believed to depend on the development of high-quality gameplay that can compete with traditional titles. This cross-sector synergy suggests that the future of the industry relies on balancing innovative monetization models with the fundamental entertainment value required for mainstream appeal.

Roblox · 2023

ReportFashion & Beauty Trends: How Gen Z Express Themselves in Immersive Spaces

This analysis explores the evolving relationship between digital identity, fashion, and physical self-expression among Gen Z consumers. The primary thesis asserts that digital avatars have become a central medium for authentic self-expression, significantly influencing physical world style, brand affinity, and mental well-being. As immersive spaces transition from mere gaming environments to social hubs, the distinction between digital and physical identity continues to blur, with a majority of users now prioritizing their virtual appearance over their physical one. The findings are based on a dual methodology: behavioral data from the Roblox platform collected between January and September 2023, and a representative survey of 1,545 Gen Z users aged 14 to 26 in the United States and the United Kingdom. Key data points reveal a significant upward trend in engagement; total avatar updates grew 38% year-over-year to 165 billion, while purchases of digital fashion items rose 15% to 1.6 billion. Notably, 56% of Gen Z respondents stated that styling their avatar is more important than styling their physical selves, an increase from 42% in the previous year. The research highlights a symbiotic relationship between realms, with 84% of respondents noting that their physical style is inspired by their avatar’s look. This digital-to-physical pipeline extends to commerce, as 84% of users are likely to consider a brand in the physical world after trying its items virtually. The report also emphasizes the psychological benefits of these spaces, with 88% of users crediting immersive expression with helping them feel more comfortable in the physical world. Industry segments covered include digital fashion, beauty, and music, noting a growing demand for exclusivity through limited-edition digital goods and community-created content. Overall, the data suggests that the metaverse is functioning as a low-stakes laboratory for identity, driving broader trends in gender-fluid fashion and diverse representation.

Blockchain

0 documentsReports in the Blockchain category.

No documents in this collection yet.

Investments

58 documentsReports in the Investments category.

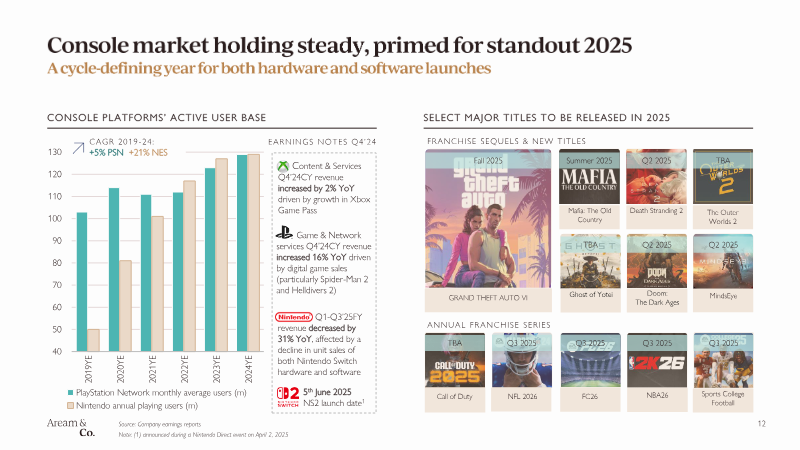

Aream & Co · 2025

FinancialVideo Game Market Update: Q1 2025

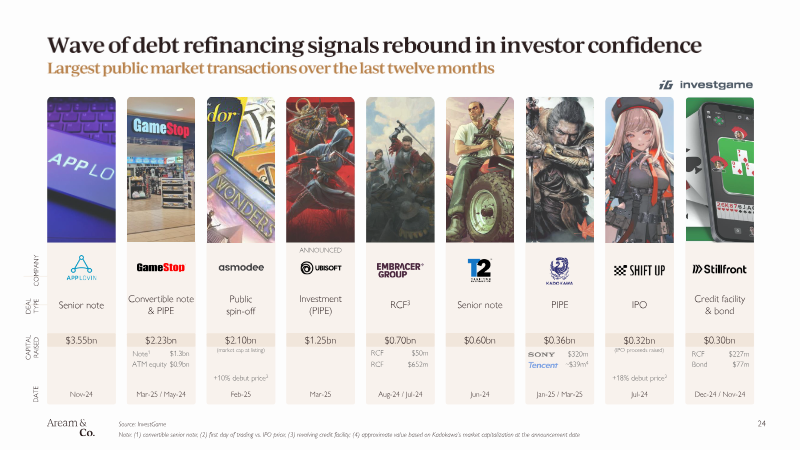

The quarterly briefing delivers a concise assessment of the global gaming ecosystem during the first quarter of 2025, emphasizing activity trends, revenue dynamics, and merger‑and‑acquisition (M&A) patterns across the principal platform segments. It argues that, despite lingering macro‑economic pressures, the industry remains resilient, with growth driven by new content releases and strategic consolidation. During the period, personal‑computer engagement surged, highlighted by Steam’s record‑high concurrent user count, while mobile spending rebounded by roughly three percent year‑on‑year, a recovery largely attributed to publishers operating in Asian markets. The console segment held steady, buoyed by anticipation of the Switch II launch and the forthcoming release of GTA VI, suggesting that flagship titles continue to anchor consumer demand across hardware categories. M&A activity reached a two‑year peak, generating approximately $6.6 billion across 42 transactions, with mobile‑focused deals accounting for about $4 billion of that total. Strategic consolidators and private‑equity firms intensified portfolio reshaping, even as later‑stage private financing grew more constrained. Although the number of deals contracted by roughly sixty percent over the preceding six months, the aggregate upfront value remained robust, indicating a shift toward fewer but larger transactions. Overall, the analysis concludes that the gaming market’s core segments are sustaining momentum amid tighter financing conditions, and that forthcoming hardware and software launches are likely to reinforce this stability. Stakeholders are advised to monitor the evolving deal landscape, where strategic scale

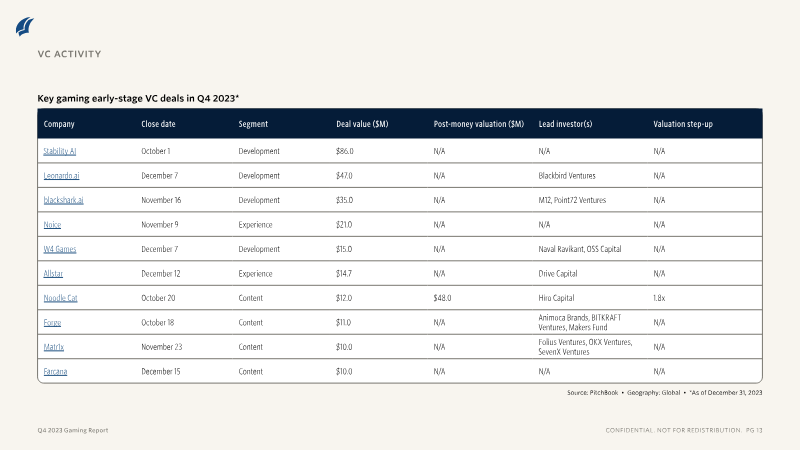

PitchBook · 2023

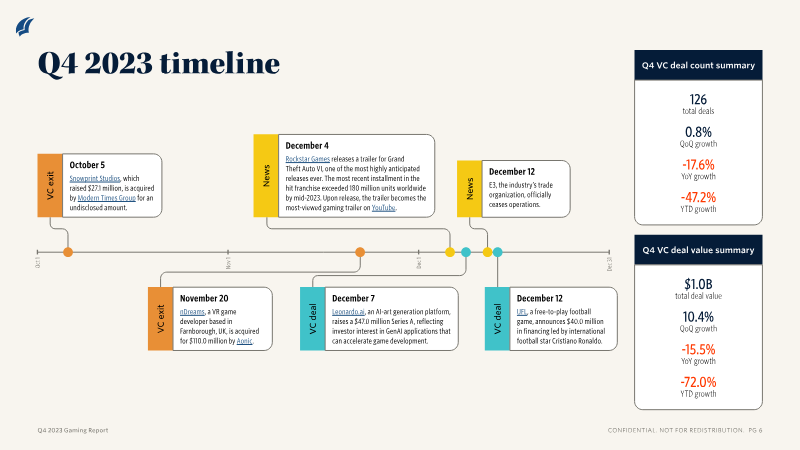

FinancialGaming Report: VC Trends and Emerging Opportunities 2023

The report examines global gaming venture capital activity in 2023, focusing on Q4 performance and broader industry trends. In the fourth quarter, 126 deals raised $1.0 billion, a modest 0.8 % increase in deal count and 10.4 % rise in value versus the prior quarter, yet both metrics fell sharply year‑over‑year by 17.6 % and 15.5 %. Cumulative 2023 activity reached $4.1 billion, the second‑lowest annual figure since 2017 and only slightly above 2019 levels. The data, sourced from PitchBook, cover all geographic regions and include studios, publishers, developer tools, SaaS platforms, and content segments. Key findings reveal that content‑related startups attracted the largest share of capital in Q4 ($438.4 million across 71 deals), followed by development firms ($288.7 million, 29 deals). Other segments—access, monetization, and gambling—experienced subdued activity. The report notes a shift in investor focus toward more mature business models such as SaaS and developer tools, reflecting the high capital intensity of game development. Methodologically, the analysis aggregates PitchBook’s deal database, reporting both quarterly and cumulative figures. It also highlights notable early‑stage deals (e.g., Stability AI, Leonardo.ai) and strategic acquirers (Unity, Sony Interactive Entertainment). The document concludes that while overall VC enthusiasm has cooled from the Web3 and metaverse peaks of 2020‑22, investment remains concentrated in content creation and developer tooling, suggesting a more realistic, sustainable growth trajectory for the gaming ecosystem.

Advertising & Monetization

6 documentsReports in the Advertising & Monetization category.

Epic Games · 2025

ReportGlobal State of Game Publishing & Marketing 2025 Industry Report

The global game publishing market is entering a period of significant expansion, projected to grow from $117.4 billion in 2025 to $150.7 billion by 2030. This growth is underpinned by a fundamental shift toward cross-platform development and the democratization of publishing tools, which has enabled independent titles to achieve massive commercial success alongside traditional publishers. A 40% increase in multi-platform launches reflects a strategic move to maximize player engagement, while the rise of "publishing as a service" models allows smaller studios to access professional marketing and analytical scale without traditional gatekeeping. The industry has almost entirely transitioned to a digital-first model, with digital sales accounting for 95% of total revenue. Marketing strategies now prioritize influencer partnerships and transmedia collaborations over traditional retail channels, as 40% of enthusiasts now make purchasing decisions based on creator recommendations. This digital dominance is further reinforced by the rise of Live Service Gaming, which is expected to reach $18.7 billion by 2030. Publishers are increasingly leveraging real-time AI data analytics and community-building initiatives to sustain long-term monetization and player retention in this competitive landscape. Revenue streams are diversifying rapidly as the market moves away from one-time purchases toward recurring models. While the premium purchase market shows only marginal growth, subscription models are forecasted to surge at a 12.2% CAGR, reaching $21.6 billion by 2030. Additionally, the esports sector remains a high-growth area, driven by sponsorships and media rights. Ultimately, sustainable growth in the modern era requires a player-centric approach that balances technological innovation with community engagement, ensuring that cross-platform strategies and AI-driven monetization can effectively offset rising development costs.

King · 2021

ReportGames Marketing Insights for 2021

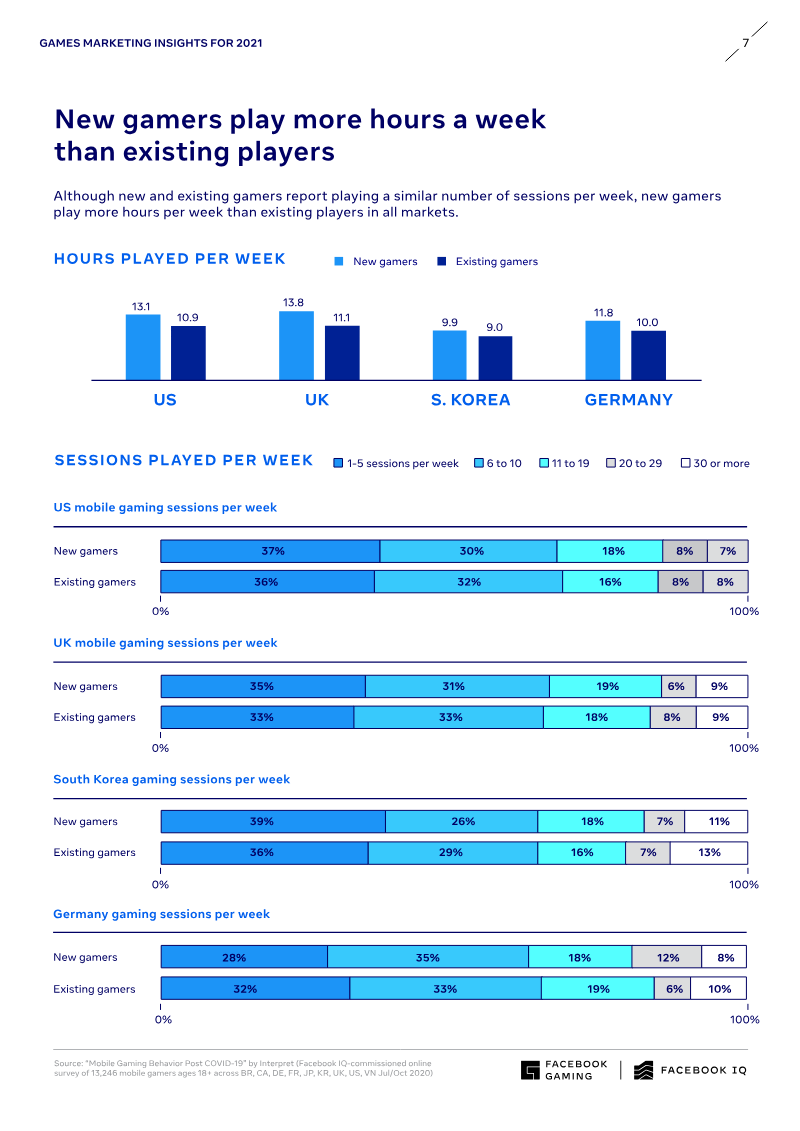

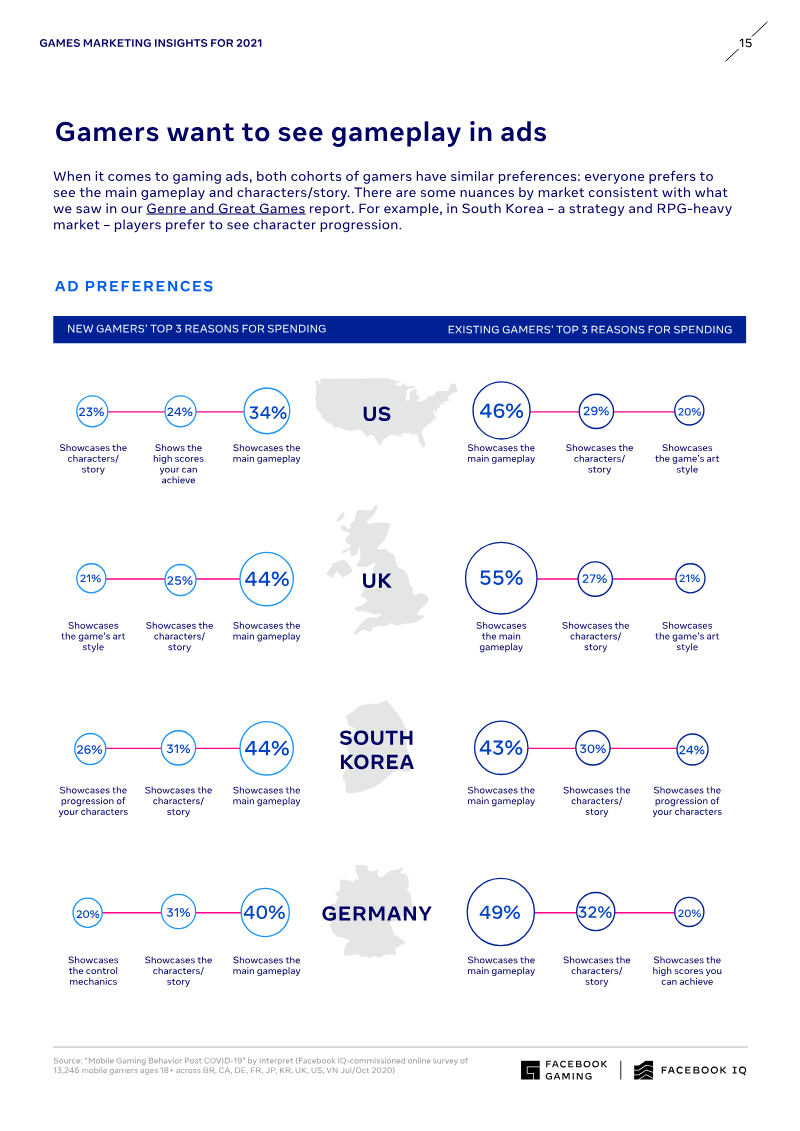

This analysis examines the shifting landscape of the global gaming industry following the COVID-19 pandemic, focusing on player motivations, monetization, and community engagement. The primary thesis asserts that the pandemic catalyzed a permanent expansion of the gaming audience, introducing a "new gamer" cohort that differs significantly from existing players in demographics and behavior. While existing players increased their time spent gaming, they became less likely to spend money, whereas new players emerged as a high-value segment with a greater propensity for in-game purchases. The findings are based on a July 2020 survey of 13,246 mobile gamers across nine markets, including the United States, United Kingdom, Germany, and South Korea. Data indicates that the mobile gaming audience grew by 28 million in the US and 8.6 million in the UK. In Western markets, these new players are significantly younger than existing ones and gravitate toward "core" genres like shooters and strategy rather than casual puzzles. Conversely, South Korea proved an anomaly, where new gamers are older and prefer casual titles. Across all regions, new gamers play more hours per week than veterans and are more open to social features, such as multiplayer modes and in-game chatting. The industry saw a massive shift toward digital discovery and community. Live-streaming platforms experienced record growth, with Facebook Gaming surpassing one billion hours watched in Q3 2020. Furthermore, 70% of consumers reported increased mobile device usage, making mobile-first discovery essential. A critical finding for marketers is the rising importance of brand familiarity; less than a quarter of players in the US, UK, and Germany tried games they had never heard of, suggesting that title recognition and IP strength are now as vital for mobile games as they are for the console market. To navigate these shifts, the analysis recommends a mixed monetization model that balances ad-supported content with in-app purchases to capture diverse spending habits. It concludes that developers must embrace "always-on" marketing and community management, as players are increasingly seeking engagement through social media groups and streaming partnerships outside of the game client itself.

Marketing (Mobile)

1 documentReports in the Marketing (Mobile) category.

Web3 & Metaverse

4 documentsReports in the Web3 & Metaverse category.

Adaverse · 2024

ReportState of Web3 in Saudi Arabia

Saudi Arabia has emerged as the dominant hub for Web3 investment in the Middle East and North Africa, capturing 51 % of Q1 2024 venture‑capital funding with $429 million across 163 deals. This concentration reflects a supportive ecosystem that blends proactive government initiatives, a growing pool of local founders, and active participation from international investors. The market is presently skewed toward consumer‑facing applications such as DeFi, GameFi and SocialFi, while foundational protocol development remains limited, highlighting a clear opening for infrastructure builders. Founders of Saudi‑based Web3 ventures underscore the rapid maturation of the sector, citing high‑profile partnerships—including Animoca Brands with NEOM, collaborations with Hedera, and alignment with Vision 2030—as catalysts for growth. Yet they identify three persistent barriers: inadequate user‑friendly interfaces, insufficient public and investor education, and ambiguous regulatory frameworks that impede both builder activity and funding cycles. Sector‑specific use cases—blockchain‑enabled freelance payments, Sharia‑compliant insurance, and localized NFT platforms—are viewed as primary drivers of mass adoption. Government commitment reinforces this trajectory, with $37.7 billion earmarked for esports and $13.3 billion for gaming, complemented by sizable venture funds such as Wa’ed’s $500 million vehicle and 500 Global’s $2.4 billion under management. Notable projects illustrate tangible impact: Tharawat Green Exchange aims to plant ten million trees by 2030, while Ticket Souq has generated $3.3 million in gross merchandise value, serving 36 k users across 55 events in ten countries. Stakeholders agree that clear, supportive regulation, robust education, and targeted technology investment are essential to translate this momentum into sustainable, high‑pay‑off outcomes for the kingdom’s burgeoning gaming, fintech, e‑commerce and proptech sectors.

Adaverse · 2024

ReportState of Web3 in Saudi Arabia: 2024 KSA Report

Saudi Arabia is rapidly establishing itself as a premier regional hub for Web3 innovation, propelled by the strategic objectives of Vision 2030 and a demographic profile characterized by a young, digitally native population. The Kingdom has secured a dominant position in the MENA venture capital landscape, capturing over 50 percent of regional funding in early 2024. This financial momentum is bolstered by robust government support, significant investments in gaming and esports, and a burgeoning startup ecosystem that is increasingly applying blockchain technology to sectors such as fintech, environmental sustainability, and secure ticketing. Despite this rapid expansion, the ecosystem faces structural challenges that must be addressed to achieve mass-market adoption. Industry stakeholders identify regulatory uncertainty, market volatility, and a persistent shortage of specialized talent as primary barriers to sustainable growth. Furthermore, the current technical complexity of decentralized applications remains a significant hurdle for the average user. Experts emphasize that for Web3 to integrate successfully into the broader economy, developers must prioritize the creation of intuitive, value-driven user interfaces that abstract away technical complexities, shifting the focus from decentralization for its own sake to practical, real-world utility. The long-term success of the Saudi Web3 sector depends on the continued alignment of technological development with national economic diversification goals. By fostering deeper collaboration between government regulators, academic institutions, and private industry, the Kingdom aims to create a stable and business-friendly environment. As the ecosystem matures, the transition from foundational infrastructure to sophisticated, user-centric applications will be critical in cementing Saudi Arabia’s status as a global leader in blockchain innovation and digital transformation.

Non-Gaming (Mobile)

1 documentReports in the Non-Gaming (Mobile) category.

Blockchain & Metaverse

2 documentsReports in the Blockchain & Metaverse category.

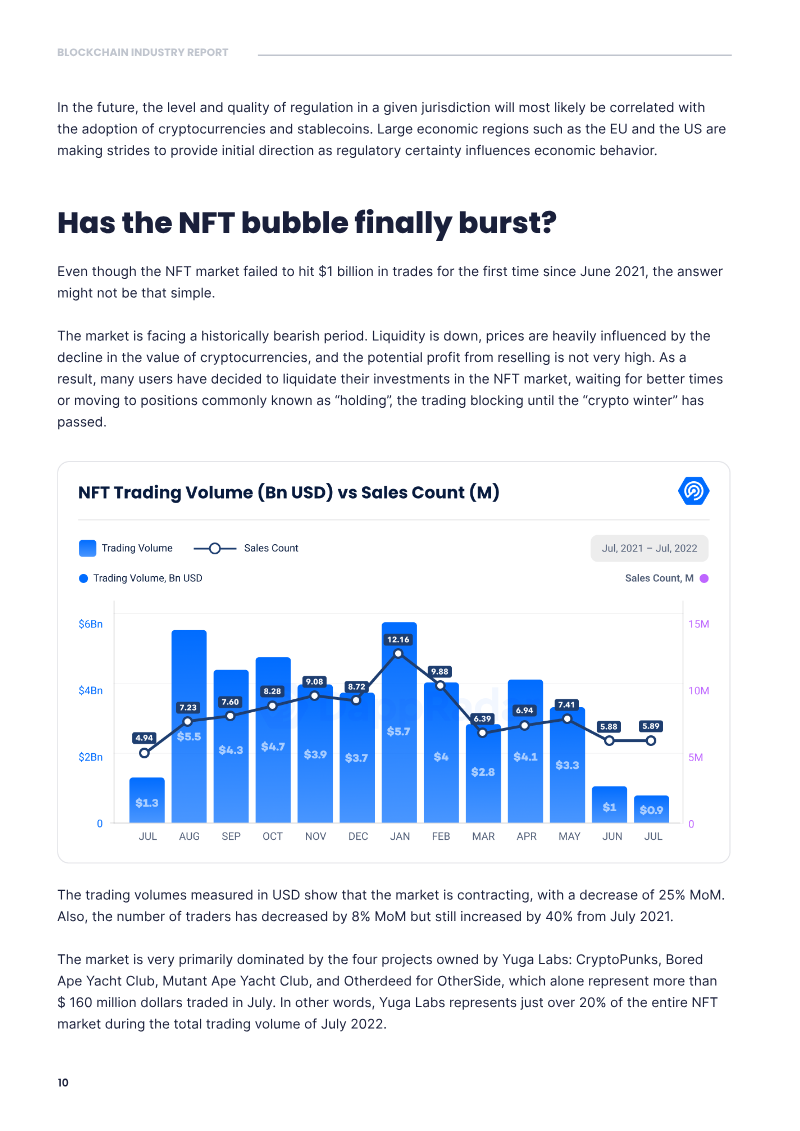

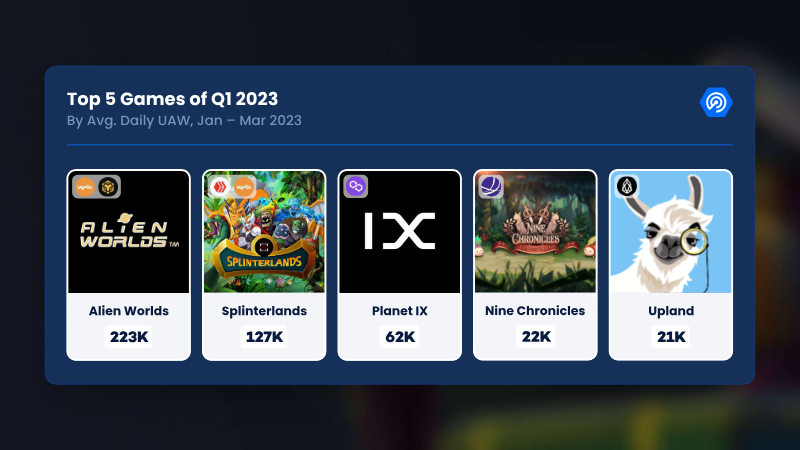

DappRadar · 2023

ReportState of Blockchain Gaming Q1 2023 Report

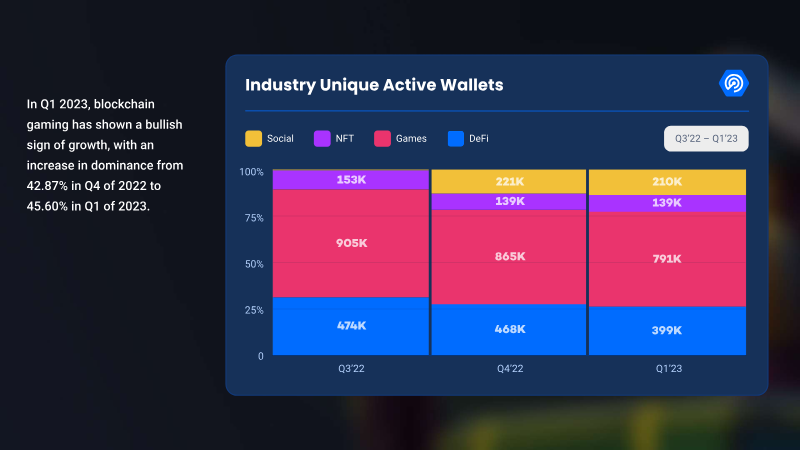

**Investment in Blockchain Games (Q4 2022 → Q1 2023)** | Quarter | Investment (USD) | Investment (Bn USD) | % Quarter‑over‑Quarter Change | |---------|------------------|----------------------|--------------------------------| | Q4 2022 | **≈ $654.5 million** | **≈ 0.655 Bn** | – | | Q1 2023 | **$739 million** | **0.739 Bn** | **+12.95 %** | **How the numbers were derived** - The report states that Q1 2023 saw a **12.95 % increase** over the previous quarter and that the Q1 2023 total was **$739 M**. - To back‑calculate the Q4 2022 figure: \[ \text{Q4 2022 Investment} = \frac{\text{Q1 2023 Investment}}{1 + 0.1295} = \frac{739\text{ M}}{1.1295} \approx 654.5\text{ M} \] - Converting to billions (1 Bn = 1,000 M): \[ 654.5\text{ M} \approx 0.655\text{ Bn} \qquad 739\text{ M} = 0.739\text{ Bn} \] **Key take‑away** - **Q1 2023** investment in blockchain gaming and metaverse projects reached **$739 M (0.739 Bn)**, marking a **robust 12.95 % quarter‑over‑quarter growth** from the **≈ $654.5 M (0.655 Bn)** invested in **Q4 2022**. This upward trajectory underscores the accelerating capital interest in the blockchain gaming sector.

Newzoo · 2022

ReportGames, Esports, Live Streaming, Cloud and the Metaverse: 2022

The global gaming industry is undergoing a fundamental transformation characterized by the convergence of traditional media, high-fidelity content, and emerging Web3 technologies. The primary thesis posits that the sector is shifting toward an interconnected, cross-platform ecosystem where revenue diversification and creator-driven engagement models are essential for growth. While consumer skepticism persists regarding blockchain-based assets and NFTs, publishers are successfully navigating this transition by prioritizing mobile esports, co-streaming strategies, and efforts to circumvent restrictive app store ecosystems to foster deeper fan loyalty. Technological infrastructure is evolving to support this expansion, with cloud-based solutions and Platform-as-a-Service models playing a critical role in mitigating hardware limitations. By integrating gaming experiences into smart TVs and leveraging cloud technology, companies are effectively broadening their reach to new demographics. Simultaneously, the metaverse has emerged as a significant focal point for venture capital and brand investment, as corporations increasingly utilize digital fashion and virtual real estate to capture the attention of younger, digitally native audiences. Geographically, the market remains dominated by the Asia-Pacific region, which generates $88.2 billion in annual revenue, representing over half of the global total. North America follows with $42.6 billion, maintaining a strong position in the industry landscape. However, the long-term trajectory of the market is increasingly influenced by emerging territories in Latin America, the Middle East, and Africa. These regions are currently expanding at rates exceeding the global average, signaling a gradual decentralization of revenue and a more diverse, globalized future for the interactive entertainment sector.

VR & AR

0 documentsReports in the VR & AR category.

No documents in this collection yet.