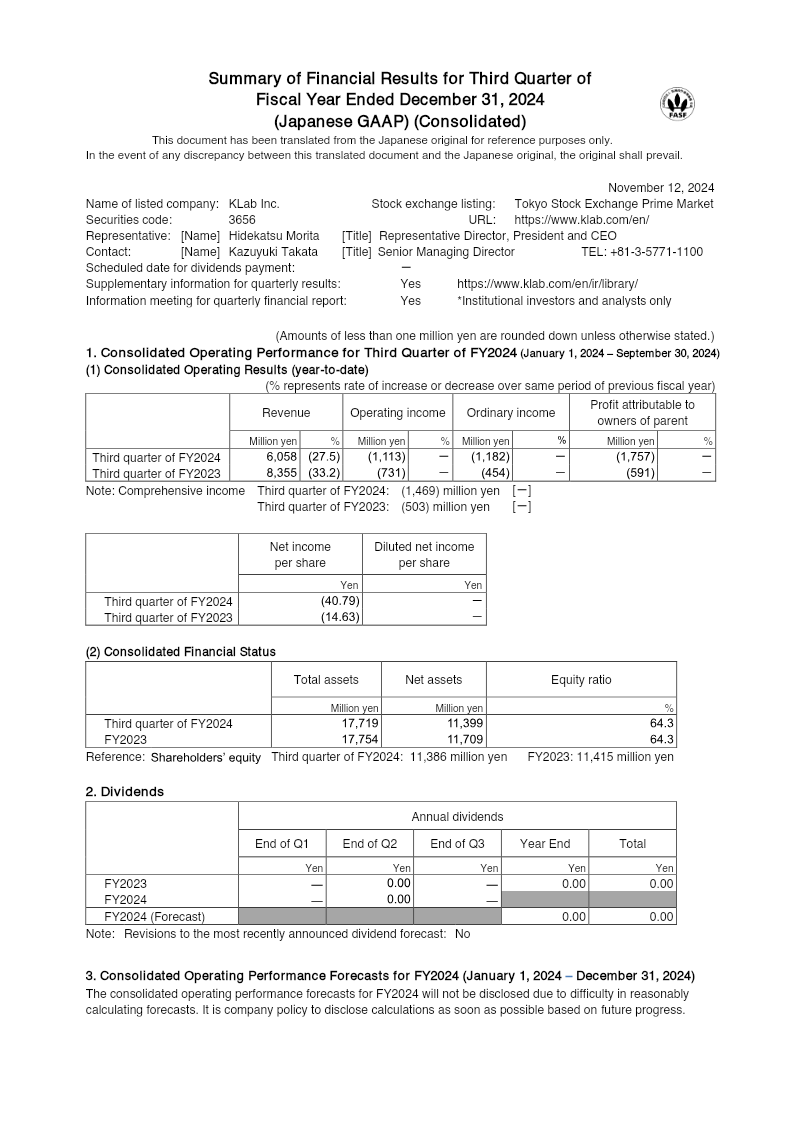

The company achieved a $15 million profit in Q3 2024, marking a significant recovery from the $3 million net loss recorded in Q1 2024.

Total revenue reached $111 million, representing a 5% increase over the previous quarter but an 8% decline compared to Q3 2023.

Monthly Paying Users (MPUs) grew 21% year-over-year to 381,000, though Average Bookings Per Paying User (ABPPU) dropped 11% to $92.

Operating costs were reduced to $94 million, a 13% year-over-year decrease driven primarily by lower selling and marketing expenses.

The Hero Wars franchise remains the primary revenue driver, with Hero Wars: Alliance and Hero Wars: Dominion Era accounting for 37% and 34% of total revenue, respectively.

Island Hoppers has become a growing contributor to the portfolio, increasing its revenue share from 4% in Q3 2023 to 7% in Q3 2024.

Revenue remains geographically concentrated in the United States (53%), followed by Europe (22%) and Asia (14%), with mobile platforms accounting for 62% of total revenue.

The financial results for the third quarter of 2024 reveal a period of stabilization and shifting cost structures within the gaming portfolio. Revenue for the quarter reached $111 million, reflecting a 5% increase from the previous quarter but an 8% decline compared to the same period in 2023. Profitability showed significant recovery from a net loss of $3 million in the first quarter of 2024 to a profit of $15 million in the third quarter, while Adjusted EBITDA remained steady at $16 million.

Operating metrics indicate a transition in user engagement and monetization. Monthly Paying Users (MPUs) grew to 381,000, a 21% increase year-over-year, though Average Bookings Per Paying User (ABPPU) declined by 11% to $92. Total bookings for the quarter stood at $108 million, showing a 6% year-over-year decrease but remaining relatively flat compared to the first half of 2024. The geographic distribution of revenue remains concentrated in the United States at 53%, followed by Europe at 22% and Asia at 14%.

The product portfolio is led by the Hero Wars franchise, with Hero Wars: Alliance and Hero Wars: Dominion Era accounting for 37% and 34% of revenue, respectively. Island Hoppers has emerged as a significant contributor, growing its revenue share from 4% in Q3 2023 to 7% in Q3 2024. Platform distribution remains dominated by mobile at 62%, with PC contributing 38%. Cost management efforts are evident in the reduction of total costs and expenses (excluding depreciation and amortization) to $94 million, down 13% from the prior year, driven largely by a decrease in selling and marketing expenses which now represent 25% of the cost base.