LOS ANGELES | SAN FRANCISCO | NEW YORK | LONDON | PARIS | MUNICH | BERLIN | DUBAI PROVEN TRACK RECORD IN GAMING M&A AND GROWTH FINANCING ADVISORY PROVEN TRACK RECORD IN GAMING M&A AND GROWTH FINANCING ADVISORY MICHAEL METZGER JULIAN RIEDLBAUER Linkedin - Free social media icons MOHIT PAREEK Linkedin - Free social media icons MICHAEL METZGER JULIAN RIEDLBAUER ...

Drake Star Partners · 2025

Drake Star Partners · 2025

Drake Star Partners · 2025

Drake Star · 2025

Drake Star Partners · 2025

Drake Star Partners · 2025

Drake Star Partners · 2025

Drake Star Partners · 2024

Drake Star Partners · 2024

Drake Star Partners · 2024

Drake Star Partners · 2024

Drake Star Partners · 2024

Aream & Co · 2026

Modern Times Group · 2026

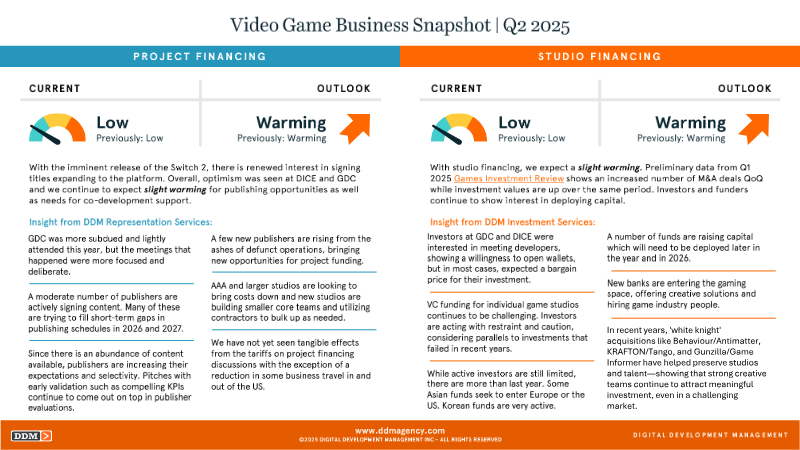

DDM · 2025

Digital Development Management · 2025

DDM · 2025

Thunderful · 2025

DDM · 2025

Aream & Co · 2025

Drake Star · 2025