Report

Global Games Market Report: August 2023

The global games market is entering a period of recovery in 2023, characterized by a projected revenue of $187.7 billion and a total player base of 3.38 billion. This 2.6% year-on-year growth signals a stabilization following the post-pandemic market correction of 2022. While mobile gaming remains the largest revenue segment, console gaming serves as the primary catalyst for this year’s expansion, rebounding significantly from previous development delays. Looking toward 2026, the industry is expected to maintain this upward trajectory, with total revenues forecasted to reach $212.4 billion. Regional performance remains uneven, as strong console demand in Western markets contrasts with slower growth in the Asia-Pacific region, where regulatory challenges in China continue to dampen momentum. To mitigate rising production costs and extended development cycles, studios are increasingly prioritizing live-service monetization models and integrating generative AI into their workflows. While these technologies offer potential for streamlined asset creation and prototyping, their long-term viability is complicated by unresolved legal and ethical concerns regarding copyright and intellectual property. The industry is undergoing a structural shift toward digital-first engagement, evidenced by the continued decline of physical media and the rise of transmedia strategies and influencer-led development. Hardware diversification is also accelerating, with the emergence of complementary handheld devices expanding the reach of traditional platforms. Despite these advancements, specific genres are experiencing shifting player preferences; while adventure and shooter titles remain dominant, the battle royale genre is losing traction. Furthermore, the mobile sector faces persistent headwinds in monetization and user acquisition, largely driven by evolving privacy policies that have impacted the performance of previously lucrative genres like RPGs.

NewzooJan 2023

Report

H1 2023 Gaming Deals Report: Navigating Turbulence

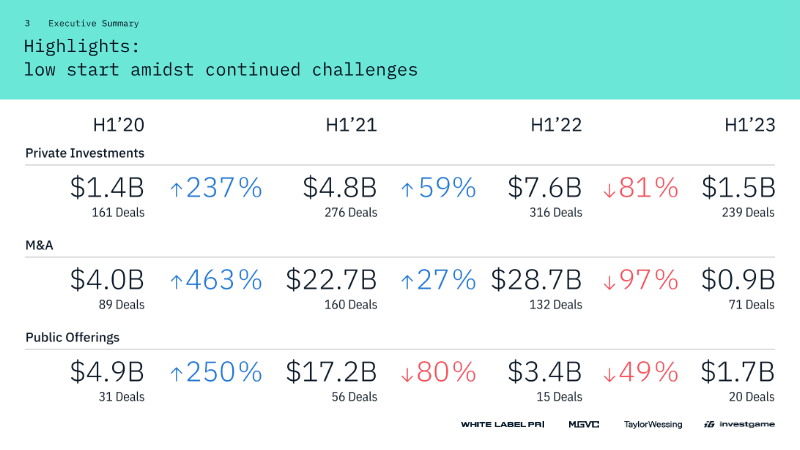

The gaming industry experienced a significant contraction in deal-making activity during the first half of 2023, characterized by a challenging macroeconomic environment and a cooling of investor sentiment. The primary thesis of this analysis is that the sector is navigating a period of turbulence where high-value exits and late-stage investments have stalled, forcing companies to prioritize profitability, cost optimization, and internal restructuring over aggressive growth. Key data points highlight a sharp decline across all major investment categories compared to the first half of 2022. Private investments fell to $1.5 billion across 239 deals, representing a substantial decrease in both volume and value. M&A activity saw an even more pronounced drop, with deal values plummeting as strategic investors shifted focus toward internal housekeeping and portfolio management. Public offerings remained largely muted, with companies increasingly opting to postpone listings due to unfavorable market conditions and valuation corrections. While early-stage venture capital remains the most resilient segment, it has also seen a shift in mindset, with startups moving away from "growth at all costs" toward sustainable business models. The scope of this analysis covers global gaming industry transactions, including private investments, M&A, and public offerings, throughout the first half of 2023. The methodology relies on tracking closed transactions involving companies with core operations in the video game sector, excluding pure gambling, betting, and non-gaming blockchain entities. Data is synthesized from public media, S&P Capital IQ, and market insights to provide a comprehensive view of the industry's financial health. Despite the current downturn, the report identifies emerging interest in artificial intelligence as a potential driver for future deal activity, even as the broader market continues to face headwinds.

InvestGameJan 2023