Skip to main content

Game Industry

Library

Library

Search

Ask AI

News

Connect your AI

Browse

The Catch Up

Topics

Collections

Writers

Help

Subscribe

Game Industry

Library

Library

Search

Ask AI

Saved

Library

13 reports matching your filters

All Types

Reports

Articles

Presentations

Whitepapers

Financial

Legal

Other

Search

MENA

Market Analysis

Esports

Investment

Africa

Saudi Arabia

Game Development

Mobile

Market Forecast

Asia

Global

Player Demographics

Marketing

Turkey

Player Behavior

Japan

Stealth Game

Sports Games

Clear

Filters

1

MENA

Recently added

Newest first

Oldest first

Title A–Z

Title Z–A

Report

52 pages

Middle East & Africa Gaming Review 2025

The Middle East and Africa gaming market is projected to grow from $7.4 billion in 2024 to over $19.4 billion by 2033, representing an 11% CAGR driven by mobile-first adoption.

Investment is highly concentrated, with Israel leading at nearly $1 billion raised across 146 startups, followed by Turkey at $961 million and Nigeria at $371 million.

Turkey has established itself as a 'unicorn factory' through major deals, including Peak Games’ $1.8 billion acquisition and Dream Games’ $2.6 billion capital raise.

Market Analysis

Market Forecast

Esports

+3

Lucidity Insights

Report

30 pages

Q4 2023 Gaming Industry Report: Global & MENAP Outlook

The global gaming market reached $212 billion in Q4 2023, with M&A activity surging to $68.7 billion, a 769% increase primarily driven by the Activision-Blizzard acquisition.

Mobile gaming remains the industry's primary platform, capturing 46% of the global player base, while indie PC titles have grown to represent approximately 30% of total revenue.

The MENAP region is a key growth area, contributing $2.8 billion to the market and recording a 30% quarter-over-quarter increase in both gamer population and venture capital investment.

Market Analysis

Investment

Global

+1

Shorooq Partners

Report

9 pages

Mobile App User Trends: MENA Ramadan 2026

Overall mobile app engagement in the MENA region during Ramadan 2026 increased by 111% compared to the same period in 2025.

In-app purchase volume saw a significant surge, rising by 91% during the 30-day Ramadan period.

Social media interaction, measured by likes, shares, and comments, grew by 63% compared to the previous year.

Market Analysis

Player Behavior

Mobile

+2

InvestGame

Jan 2026

Report

3 pages

Asian & MENA Markets: 2025 Half-Year Report

China remains the dominant regional market with projected 2025 revenues of $51.2 billion, supported by a 4.1% year-over-year increase and a 24% rise in government game approvals.

India is the fastest-growing market, projected to exceed $1 billion in 2025 with 16.2% year-over-year growth following the PROG Act's shift toward traditional gaming and esports.

The MENA-3 region (Saudi Arabia, UAE, and Egypt) has a revised growth forecast of 6.4%, as economic challenges in Egypt and slowing mobile growth in Saudi Arabia temper the impact of government-led localization efforts.

Market Analysis

Market Forecast

Asia

+1

Niko Partners

Jan 2025

Report

19 pages

What Does the Monetization Landscape Look Like for Video Games in MENA?

The MENA-3 gaming market (KSA, UAE, Egypt) generated $2 billion in player spending in 2024 and is projected to grow to over $2.7 billion by 2028.

Payment infrastructure is a major barrier, as 67% of the regional population lacks access to traditional credit or debit cards, necessitating the integration of local payment networks like Mada in Saudi Arabia and Fawry in Egypt.

Direct-to-consumer (D2C) web shops are essential for bypassing 30% app store fees, with 53% of paying gamers in the region already utilizing official game websites for purchases.

Monetization

Market Analysis

Player Demographics

+1

Xsolla & Niko Partners

Jan 2025

Report

7 pages

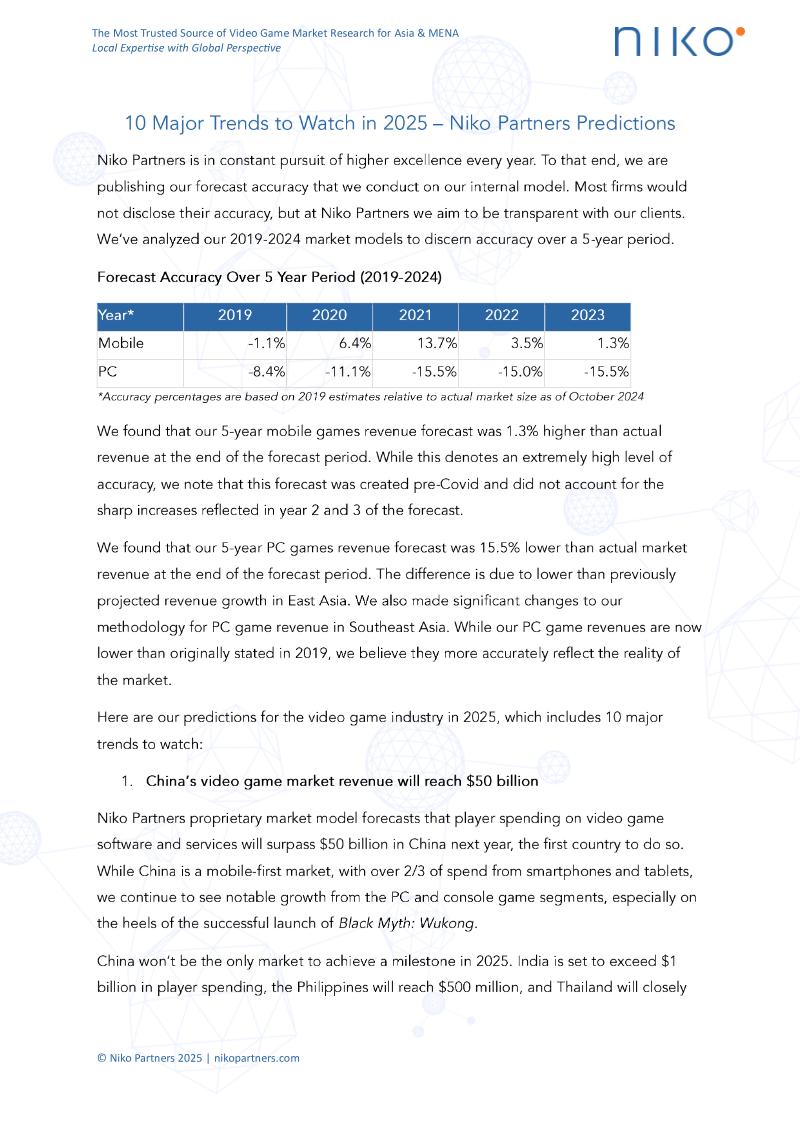

10 Major Trends to Watch in Asia & MENA

Asia and MENA are the primary engines of global gaming growth, driven by a mobile-first audience and a rising middle class with increased discretionary income.

Government-backed investments in Saudi Arabia and the UAE are rapidly establishing these nations as central hubs for international esports and game development infrastructure.

Market success in these regions now requires hyper-localization and the adoption of innovative payment ecosystems that bypass traditional storefront limitations.

Market Analysis

Player Demographics

Asia

+2

Niko Partners

Jan 2025

Report

145 pages

State of Web3 in Saudi Arabia: 2024 KSA Report

Saudi Arabia captured over 50 percent of all regional venture capital funding in the MENA region during early 2024.

Vision 2030 and a young, digitally native population are the primary drivers establishing the Kingdom as a premier regional hub for Web3 innovation.

The Saudi Web3 sector is currently focused on applying blockchain technology to fintech, environmental sustainability, and secure ticketing, alongside significant investments in gaming and esports.

Web3

Blockchain

Market Analysis

+3

Adaverse

Jan 2024

Report

36 pages

Localization in the MENA Region

The MENA gaming market is a high-growth frontier projected to reach $3.24 billion in player spending and 38.9 million gamers by 2028.

There is a significant supply gap in the region, as only 3.5% of Steam titles are currently localized despite 41% of regional gamers prioritizing localized content.

Deep culturalization can drive exponential growth, with some titles increasing their MENA-based revenue and daily active users from 3% to 80% of their global total.

Market Analysis

Player Demographics

Esports

+1

Saudi Esports Federation

Jan 2024

Report

30 pages

Gaming Industry Report: Global & MENAP Outlook Q4 2023

Investment activity in the gaming sector is currently targeting early-stage ventures from pre-seed to Series A, with typical ticket sizes ranging from $1 million to $8 million.

Strategic investment is focused on three core pillars: high-value intellectual property, software solutions that reduce development costs, and ecosystems centered on user-generated content.

The industry is experiencing a rapid convergence of emerging technologies, including AI, VR, cloud gaming, quantum computing, and GPU-as-a-Service, to accelerate content creation and distribution.

Market Analysis

Investment

Global

+1

Shorooq Partners

Dec 2023

Report

36 pages

Gametech Report: Global & MENAP Outlook Q3 2023

The global gaming market reached a valuation exceeding $250 billion with a 9.9% CAGR, even as the industry underwent a period of operational recalibration resulting in over 2,000 layoffs in Q3 2023.

The MENA region remains a growth outlier, expanding 6.9% year-over-year to reach a $5 billion market size, supported by a demographic where 70% of the population is under 30.

Global venture capital investment returned to pre-pandemic levels with $454 million secured in Q3 2023, with Jordan emerging as a regional hub by capturing 30% of all MENA-based deals.

Market Analysis

Investment

MENA

Shorooq Partners

Sept 2023

Report

25 pages

The MENA Games Market: From Sand to Stardom

The MENA-3 region (Saudi Arabia, UAE, and Egypt) generated $1.8 billion in revenue from 67.4 million gamers as of 2022, driven by a mobile-first ecosystem.

Cultural localization is a critical success factor, with 86.6% of regional gamers prioritizing language support and successful titles integrating Arabic themes and local celebrities.

Esports is a primary engagement driver, with 73% of regional gamers participating in competitive gaming supported by massive prize pools and dedicated infrastructure.

Market Analysis

MENA

Saudi Arabia

+3

Niko Partners

Jan 2023

Report

15 pages

Five Key Mobile Game Genres in Asia and MENA

RPG titles are the dominant market force, generating 50% more revenue than the other four top genres combined and achieving the highest monetization score of 7.7.

Puzzle games command the largest download volume and highest engagement score of 6.0, though they suffer from low monetization and minimal esports relevance.

Battle Royale games lead the market in esports influence with a score of 9.5, despite generating the lowest total revenue among the five genres.

Market Analysis

Mobile

Asia

+1

Niko Partners

Jan 2023

Report

98 pages

Gametech Report Q1 2023: Global & MENAP Outlook

The MENAP gaming market is projected to reach $2.8 billion by 2026, growing at a 10% CAGR driven by mobile adoption and esports.

Generative AI in gaming is forecast to reach a $7.1 billion valuation by 2032, expanding at a 23.3% CAGR.

Global cloud-gaming infrastructure is projected to grow 250% by 2030, supported by the fact that 68% of studios already utilize AWS for Games.

Market Analysis

Esports

MENA

+1

Shorooq Partners

Jan 2023