Report

Europe and Esports: High Engagement and Even Higher Potential

The study demonstrates that European esports audiences are expanding rapidly, with a projected 92 million viewers by the end of 2020 and a year‑over‑year growth of 7.4 %. Enthusiasts—those watching professional content more than once a month—total 33 million, while occasional viewers comprise the remaining 59 million. Revenue forecasts show a global market of nearly €974 million in 2020, rising to €1.6 billion by 2023, with Europe mirroring this trajectory. Survey data from 10,175 respondents aged 18‑45 across ten Western and Northern European countries reveal that esports engagement is not confined to the youngest cohort; only 33 % of 18‑20 year olds are regular enthusiasts, whereas the 21‑25 age group leads in engagement. Geographic variation is pronounced: Finland shows a 52 % enthusiast rate among 18‑20 year olds, compared to 21 % in the UK. COVID‑19 lockdowns increased viewership in markets with stricter restrictions, and 62 % of respondents in Spain and the UK expect continued higher viewership post‑lockdown. Gender analysis indicates that 32 % of the audience are women, primarily occasional viewers. Nonetheless, female participation in competitive play is rising, with 60 % of respondents acknowledging growth in women’s involvement. Women spend money on esports products at a comparable rate to men (46 % vs 38 %) and favor physical merchandise, whereas men lean toward digital items such as skins and premium passes. The research underscores strong cross‑sport interest, with 64 % of viewers also supporting a favorite sports team, and highlights the strategic opportunity for brands to engage this growing, diverse, and monetarily active audience.

PayPalJan 2020

Report

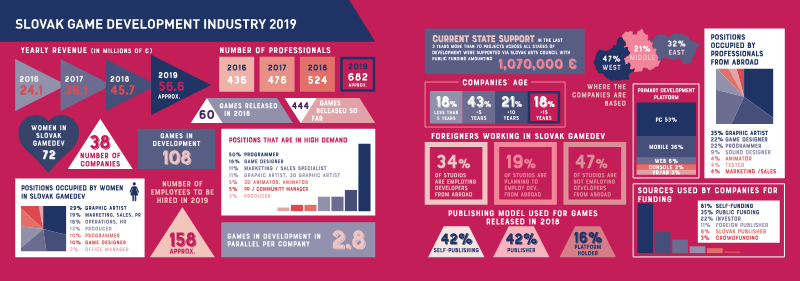

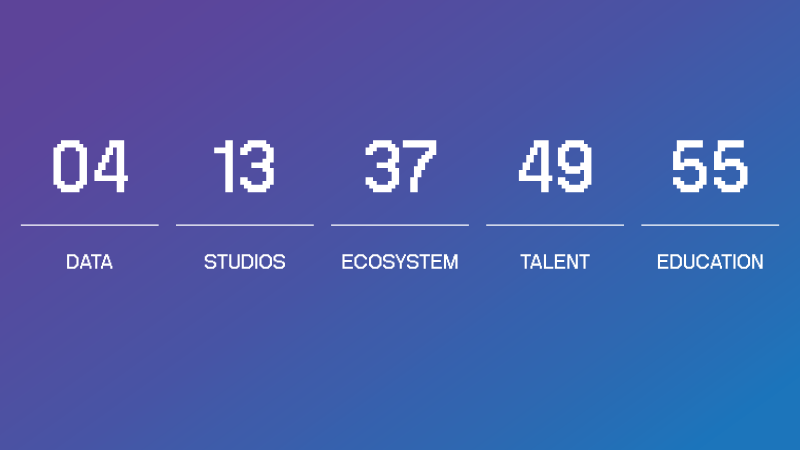

Gaming Industry Report: Serbia 2020

The 2020 assessment of Serbia’s video‑game sector presents a rapidly expanding ecosystem that has moved beyond a modest, paper‑based association to become a central hub for nearly one hundred companies. In a single year the industry surpassed €100 million in revenue, a 20 percent increase over the previous period, while supporting 120 development teams and roughly 2 100 employees, about one‑third of whom are women. The market delivered 41 new mobile titles, with most studios concentrated in Belgrade and financing split between angel investors and state‑funded programmes, which together account for 45 percent of capital. A clear majority of firms intend to grow their staff in 2021, despite citing regulatory red‑tape, limited legal incentives and insufficient console support as persistent obstacles. The sector is dominated by small‑to‑mid‑size studios, typically employing five to twenty‑five people, that provide full‑cycle development, consulting and backend‑as‑a‑service solutions. Companies such as Elbet and Tummy Games have already achieved notable market traction, with Elbet’s products operating on more than 130 operators across 30 countries. The pandemic forced a swift transition to remote work, exposing resource constraints and talent‑recruitment challenges, yet overall productivity remained stable and the community’s outlook stayed positive. Industry networking was sustained through a dedicated Discord community of over a thousand members and forty channels, while the Serbian Games Association launched talent‑development initiatives including a “Shift 2 Games” job‑role series and a mentorship pilot for fifteen participants. Parallel to these efforts, game‑related education expanded dramatically: the Master 4.0 Hub in Gaming at the University of Kragujevac and a new master’s programme at the University of Arts in Belgrade will together serve more than 1 500 students, supported by over thirty professors and a dozen new degree and certificate programmes across ten institutions. Backed by partners such as Epic Games, Crater Training Center and Nordeus, this coordinated educational push is poised to supply a robust pipeline of world‑class talent for Serbia’s indie and mid‑size studios.

SGAJan 2020