ReportSyndicat National du Jeu Vidéo

Baromètre Annuel du Jeu Vidéo en France: 2020

1 Jan 202019 pages~28 min full read

France ranks as the second-largest global hub for video game development, trailing only the United States.

See it on page 15The industry is primarily composed of independent development studios, with 93% identifying as independent and 74% focused on creating original intellectual properties.

See it on page 7International markets are a primary revenue driver, accounting for 44% of total studio income.

See it on page 4The sector relies heavily on self-financing and public support mechanisms like the Video Game Tax Credit (CIJV), as traditional bank credit remains difficult to access.

See it on page 13The workforce is characterized by stability and growth, with a trend toward permanent, qualified positions and high hiring intentions.

See it on page 11A robust educational pipeline supports the industry, with 40 institutions currently training talent in design, technology, and management roles.

See it on page 17While PC remains the dominant platform, studios are navigating industrial shifts toward cloud gaming, immersive technologies, and evolving distribution models.

See it on page 3The 2020 Annual Barometer of the Video Game Industry in France provides a comprehensive analysis of the sector’s economic health, production landscape, and educational ecosystem. Based on a survey of 1,131 industry structures conducted between June and September 2019, the report highlights a robust industry characterized by steady growth, strong entrepreneurial spirit, and significant international reach. The findings underscore France's position as a highly attractive hub for video game development, ranking second globally behind the United States.

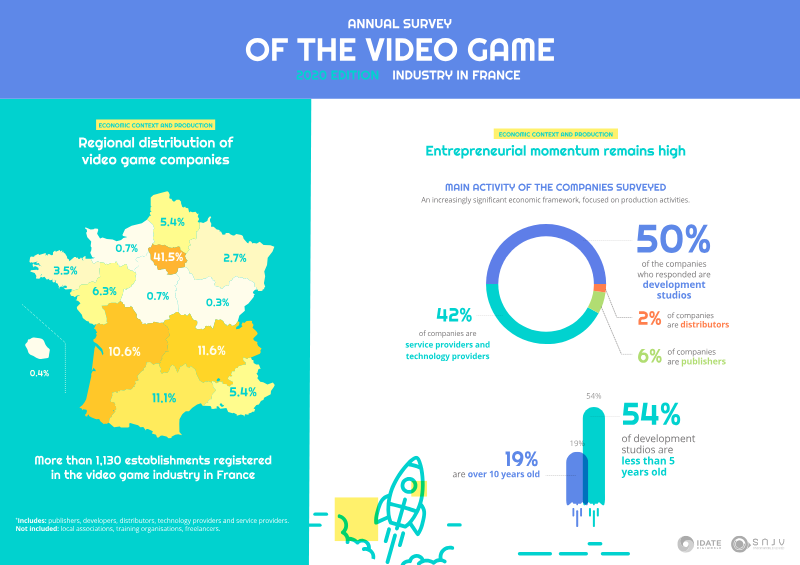

Key findings reveal that the industry is heavily focused on production, with half of all sector entities operating as development studios. These studios demonstrate a strong commitment to independence, with 93% identifying as independent and 74% actively creating original intellectual properties. Production remains largely centered on PC platforms, though mobile and console markets remain vital. Financially, the sector relies heavily on self-financing, supplemented by public support mechanisms such as the Video Game Tax Credit (CIJV) and regional aids. Despite this, access to traditional bank credit remains a challenge for many studios.

The report also details a positive outlook for employment, noting a trend toward stable, qualified, and permanent positions, with significant hiring intentions for the coming year. The educational sector is identified as a critical pillar of this growth, with 40 surveyed institutions training a growing pipeline of talent across design, technology, and management roles. While the industry shows resilience and optimism, it faces ongoing industrial transitions, including the rise of cloud gaming, immersive technologies, and new distribution models. Overall, the sector maintains a strong export orientation, with 44% of studio revenue generated internationally, reinforcing the strategic importance of the French video game industry within the global market.