Report

The Most Exciting Time in the Gaming Industry: 2020–2022

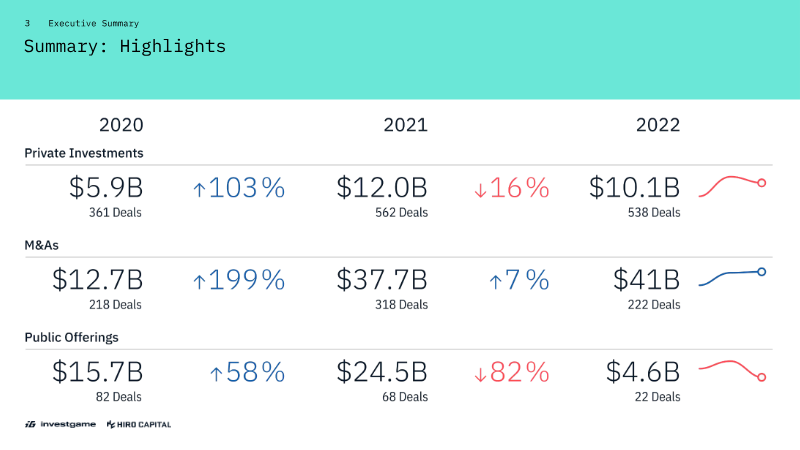

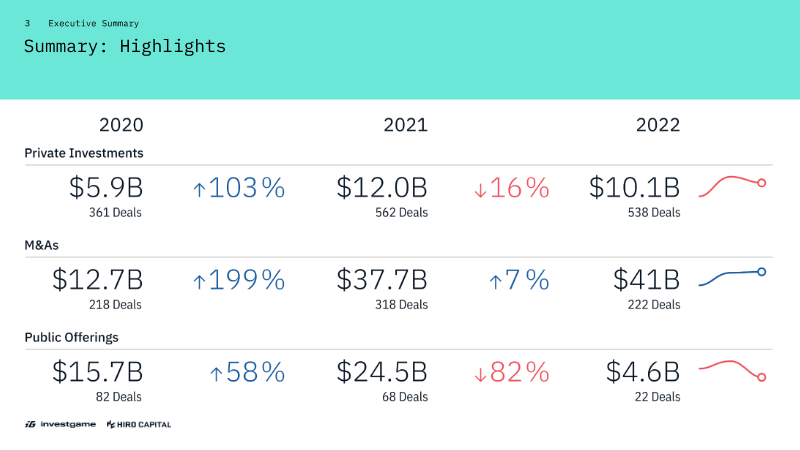

The analysis demonstrates that the gaming sector experienced a pronounced surge in deal activity between 2020 and 2022, with private equity investments peaking at $12 billion in 2021 before receding to $10.1 billion the following year. Mergers and acquisitions reached a high of $41 billion in 2021, cooling to $27.3 billion in 2022, while public offerings peaked at $24.5 billion and collapsed to $4.6 billion amid a macro‑economic slowdown projected to continue into 2023. Despite this contraction, strategic investors such as Microsoft, Sony, and Netflix maintained studio acquisitions, and early‑stage venture capital remained resilient with substantial dry powder poised for future rounds. Late‑stage transactions contracted sharply in early 2023, with only sixteen deals versus thirty‑one in 2022 and a four‑and‑a‑half‑fold decline in disclosed value from $4.2 billion to $0.9 billion. The top fifteen M&A deals over the period accounted for roughly eighty percent of announced value, dominated by public takeovers—including Microsoft’s purchases of Activision Blizzard and ZeniMax—and characterized by high EV/EBITDA multiples, reaching up to 55×. Venture capital activity stayed robust, led by Makers Fund and BITKRAFT Ventures in both deal count and value. Corporate investments slowed in 2022 but are expected to rebound as regulatory scrutiny eases and large cash reserves, such as Epic’s $2 billion, become available. The report is framed within a global context, covering all major gaming markets from 2020 through 2022, with particular emphasis on the United States, Europe, and Asia. It focuses on public, private, and venture capital transactions across the industry’s core segments—game development studios, publishing platforms, and emerging technology providers. The findings underscore a transition from high‑volume, high‑valuation deals toward a more cautious investment climate, while highlighting the enduring appeal of strategic acquisitions and venture funding as engines for future growth.

InvestGameJan 2020

Report

2020–2022: The Most Exciting Time in the Gaming Industry

This analysis examines global investment and merger and acquisition (M&A) activity within the video game industry from 2020 through 2022. The primary thesis posits that the industry has passed a historic peak of deal-making and is now entering a "Great Reset" characterized by market cooling, lower valuations, and a shift in investor priorities. While the era of massive public offerings and late-stage venture capital (VC) surges has slowed due to macroeconomic headwinds like inflation and rising interest rates, the industry remains fundamentally strong with significant "dry powder" available for early-stage startups and strategic consolidations. The data reveals a volatile three-year cycle. M&A activity reached a zenith in 2022 with $37.7 billion in closed deals—a 199% increase in value from 2021—driven by massive consolidations such as Take-Two’s acquisition of Zynga. Conversely, public offerings plummeted by 82% in 2022 as the IPO and SPAC windows effectively closed. Private investments also saw a 16% decline in value in 2022 after doubling the previous year. Despite these drops, early-stage VC remained resilient, with over $6.2 billion raised by gaming-focused funds ready for deployment. Geographically and segmentally, the scope is global, with specific attention paid to the decline of mobile gaming hype post-IDFA and the rising interest in PC, console, and AI-driven startups. The report highlights a stark cooling in Web3 gaming, where investor "FOMO" has been replaced by a focus on fundamental gameplay and infrastructure. Gender diversity remains a challenge in the sector; 89% of funded or acquired companies were led by men in 2022, a negligible change from 90% in 2021. Methodologically, the findings are based on tracked closed transactions across video game publishers, developers, and hardware providers. Data was aggregated from public media, S&P Capital IQ, and partner insights, utilizing a weighted ranking system to identify the most active investors. The analysis concludes that while the "peak wave" has passed, the industry is transitioning into a more disciplined phase of the investment cycle.

InvestGameJan 2020