Skip to main content

Game Industry

Library

Library

Search

Ask AI

News

Connect your AI

Browse

The Catch Up

Topics

Collections

Writers

Help

Subscribe

Game Industry

Library

Library

Search

Ask AI

Saved

Library

1,733 game-industry reports — read the key insights or open the source.

All Types

Reports

Articles

Presentations

Whitepapers

Financial

Legal

Other

Search

Market Analysis

Global

Mobile

Game Development

Marketing

Monetization

Investment

PC

User Acquisition

Game Publishing

Europe

Player Behavior

Console

Advertising

Germany

Employment

Steam

Game Design

Filters

Recently added

Newest first

Oldest first

Title A–Z

Title Z–A

Report

3 pages

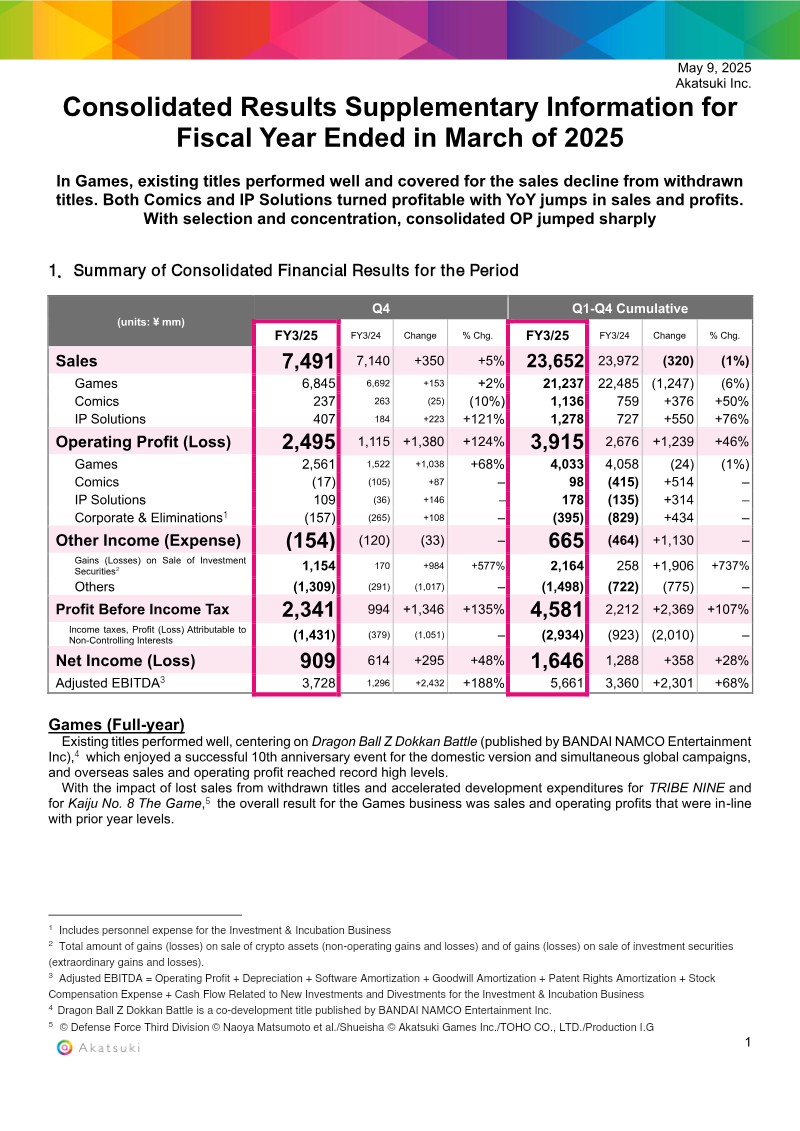

Consolidated Results Supplementary Information: Fiscal Year Ended March 2025

Akatsuki Inc. reported a 124% surge in operating profit to ¥3.915 billion for the fiscal year ended March 2025, driven by a 68% increase in gaming segment profit and ¥1.154 billion in gains from the sale of investment securities.

Total sales grew 5% year-over-year to ¥23.652 billion, supported by the continued strong performance of existing titles like Dragon Ball Z Dokkan Battle.

Net income rose 48% to ¥1.646 billion, while adjusted EBITDA increased 28% to ¥5.661 billion.

Market Analysis

Investment

Mobile

+1

Akatsuki

Report

12 pages

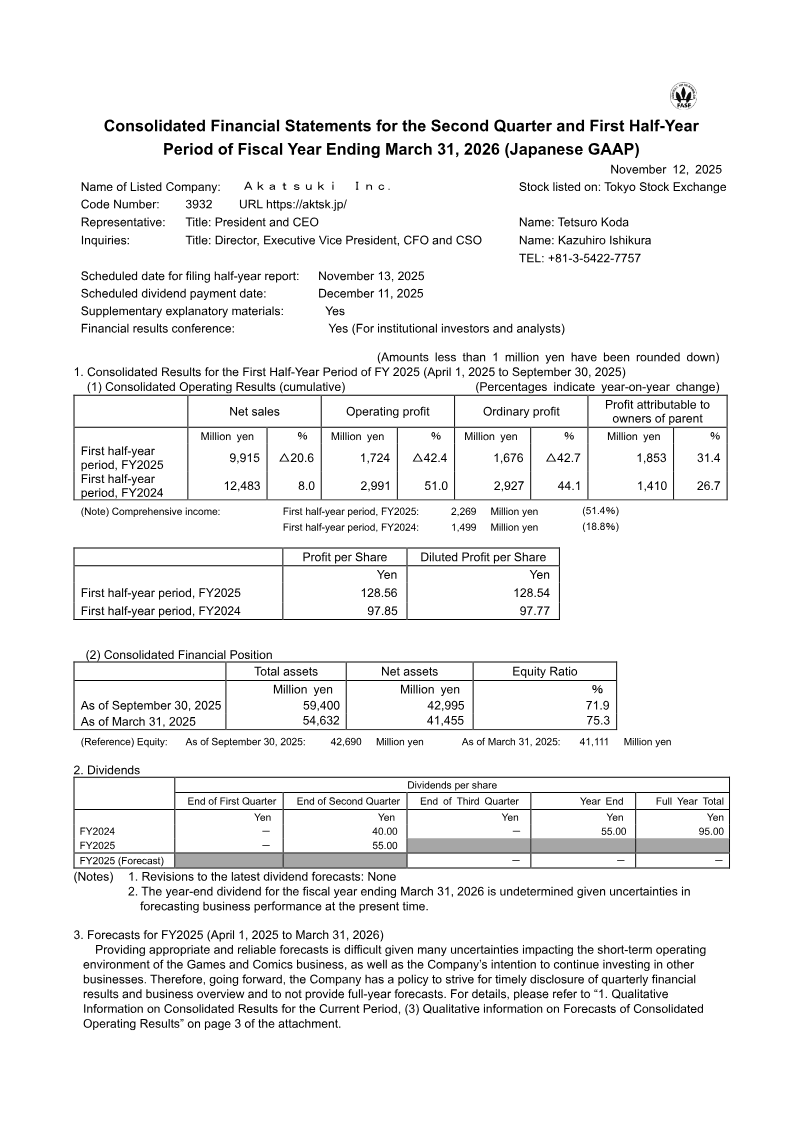

Consolidated Financial Statements: Second Quarter and First Half-Year Period of Fiscal Year Ending March 31, 2026

Akatsuki Inc. reported a 20.6% YoY decline in net sales to ¥9,915 million and a 42.4% drop in operating profit to ¥1,724 million for the first half of the fiscal year ending March 31, 2026.

Net income attributable to the parent rose 31.4% to ¥1,853 million, with diluted earnings per share increasing from ¥97.85 to ¥128.56.

The core Games and Comics segment, which accounts for the majority of revenue, saw a 23.2% sales decline and a 41.2% drop in profit.

Investment

Japan

Mobile

+1

Akatsuki

Report

4 pages

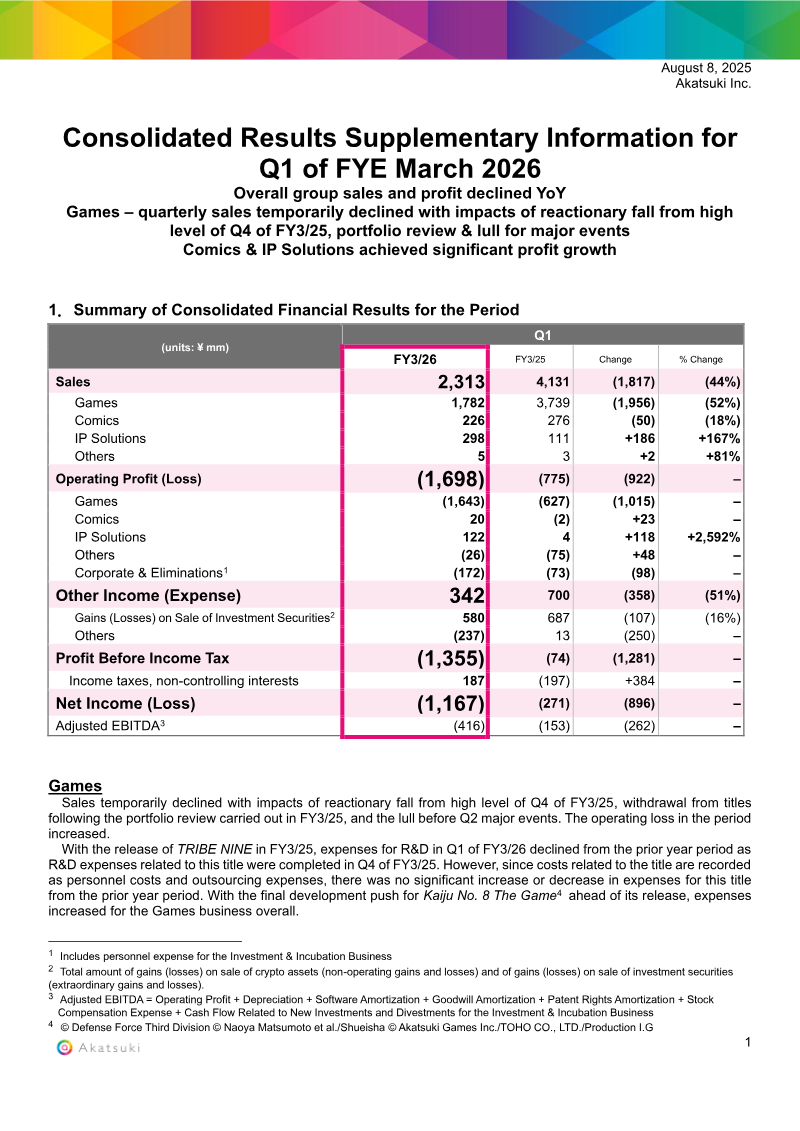

Consolidated Results Supplementary Information: Q1 FYE March 2026

Akatsuki Inc. reported a 44% year-over-year decline in total consolidated sales to ¥2,313 million for Q1 FYE March 2026, resulting in a net loss of ¥1,167 million.

The Games segment experienced a 52% sales drop to ¥1,782 million and an operating loss of ¥1,643 million, driven by a portfolio review withdrawal and a lack of major new releases.

The IP Solutions unit achieved significant growth, with sales increasing 167% to ¥298 million and operating profit rising 2,592% to ¥122 million, bolstered by the 'Slash Gift' online lottery and the consolidation of CRAYON, Inc.

Market Analysis

Mobile

Japan

+1

Akatsuki

Report

3 pages

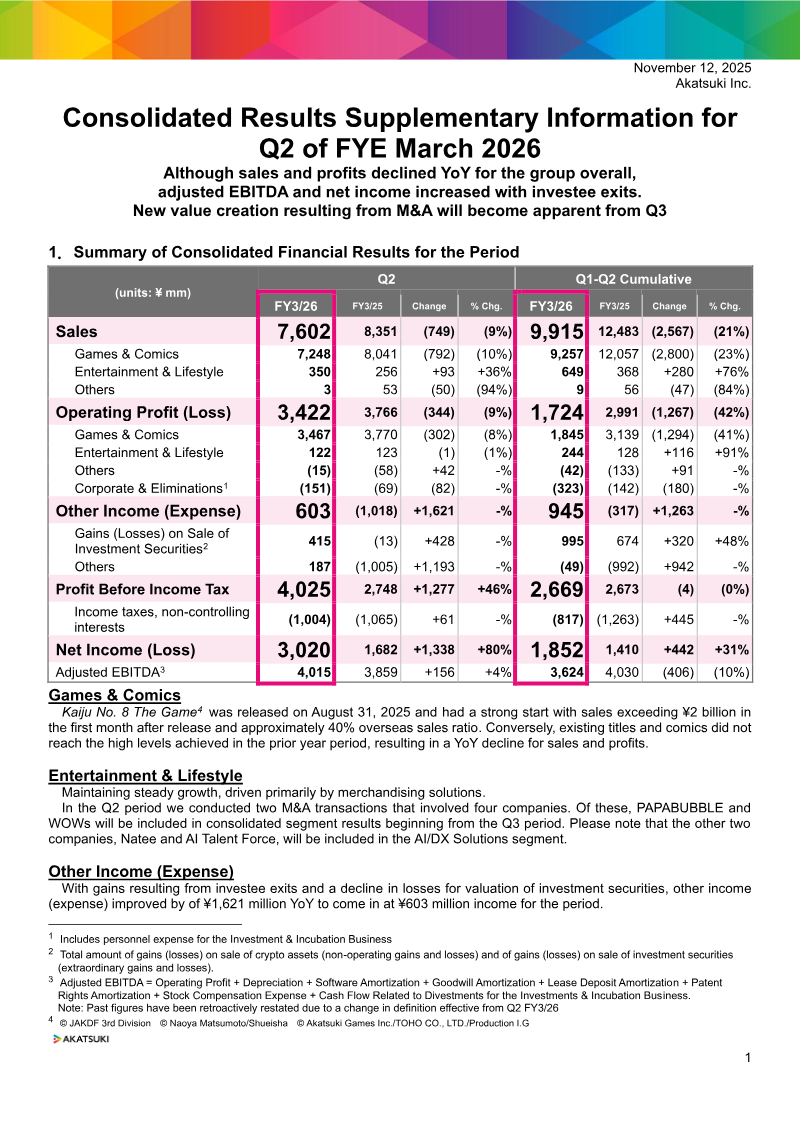

Consolidated Results Supplementary Information: Q2 of FYE March 2026

Akatsuki Inc. reported a 9% decline in quarterly sales to ¥7,602 million, primarily driven by a 10% YoY contraction in the core Games & Comics segment.

Net income surged 80% to ¥3,020 million, bolstered by gains from investee exits and a reduction in valuation losses on investment securities despite lower operating profit.

The launch of 'Kaiju No. 8 The Game' on 31 August 2025 generated over ¥2 billion in first-month sales, with 40% of revenue originating from overseas markets.

Market Analysis

Mergers & Acquisitions

Investment

+2

Akatsuki

Report

11 pages

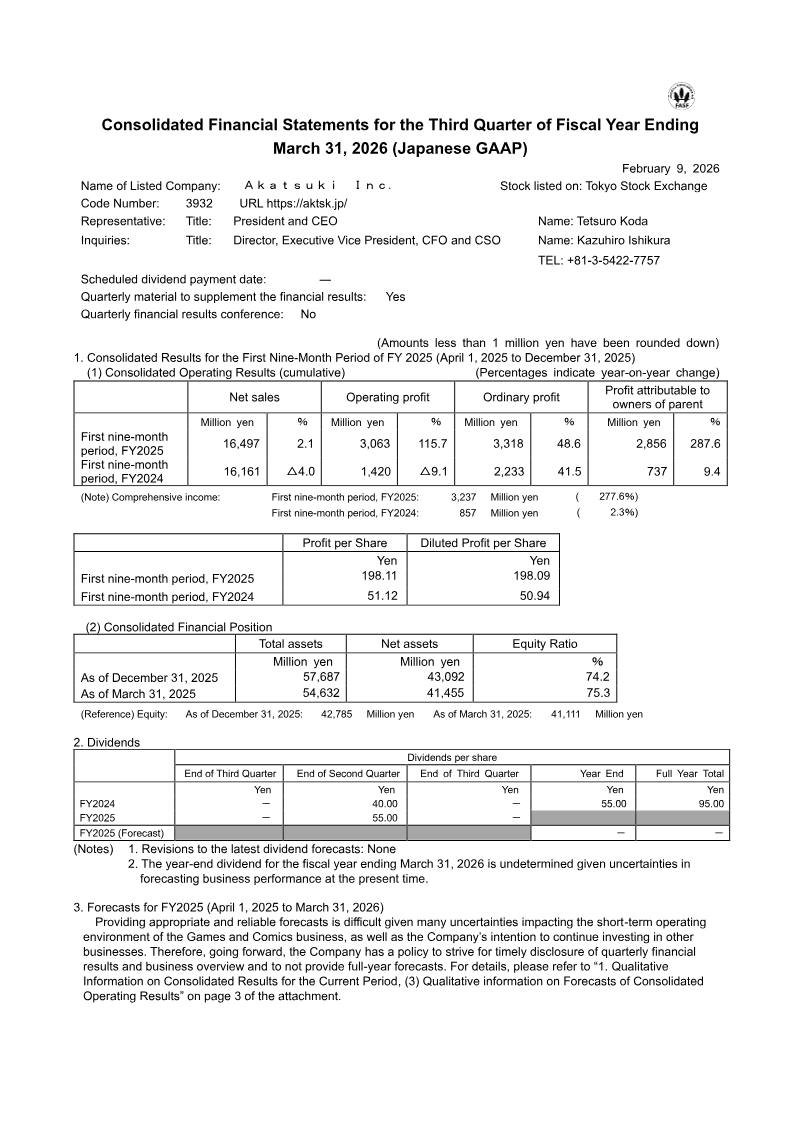

Consolidated Financial Statements for the Third Quarter of Fiscal Year Ending March 31, 2026

Akatsuki Inc. reported a significant surge in profitability for the first nine months of FY2025, with operating profit rising 115.7% to ¥3,063 million and net profit attributable to parent shareholders climbing 287.6% to ¥2,856 million.

Net sales grew modestly by 2.1% to ¥16,497 million, while diluted earnings per share increased substantially to ¥198.11 compared to ¥51.12 in the prior year.

The core Games and Comics business experienced a 5.3% decline in sales but successfully doubled its operating profit through effective cost-reduction measures.

Market Analysis

Investment

Mobile

+1

Akatsuki

Report

4 pages

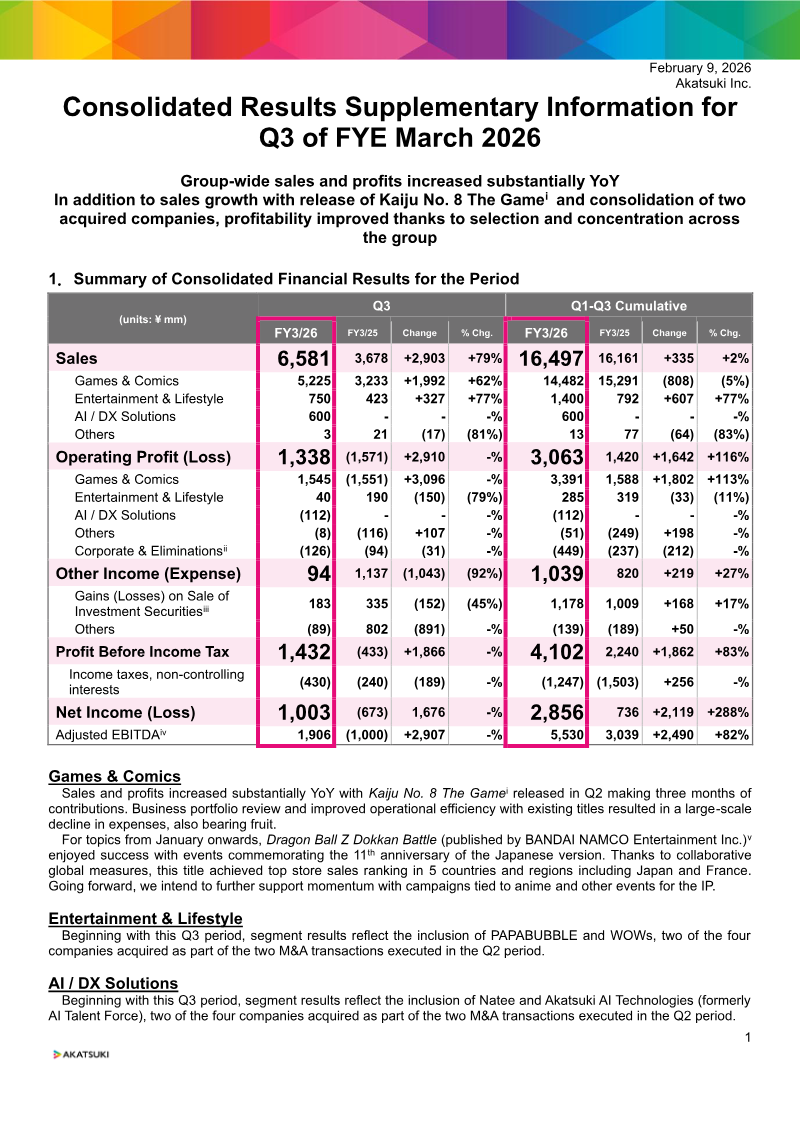

Consolidated Results Supplementary Information: Q3 FY3/26

Akatsuki Inc. achieved a significant financial turnaround in Q3 FY3/26, reporting ¥6,581 million in group-wide sales (up 79% YoY) and an operating profit of ¥1,338 million, reversing a prior-year loss of ¥1,571 million.

The primary growth driver was the Q2 release of 'Kaiju No. 8 The Game,' which contributed three months of revenue and helped boost Games & Comics segment sales by 62% to ¥5,225 million.

Net income reached ¥1,003 million, a 288% increase compared to the ¥673 million loss recorded in the same period last year.

Market Analysis

Mergers & Acquisitions

Mobile

+1

Akatsuki

Report

1 pages

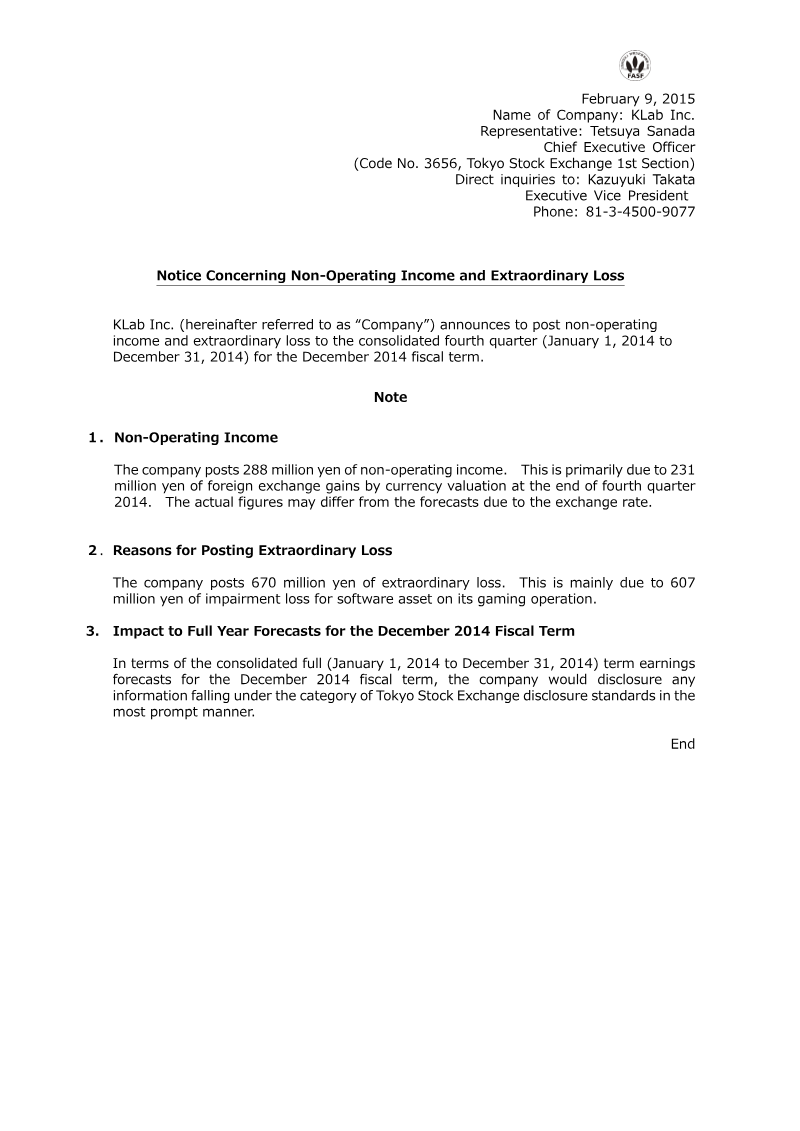

Notice Concerning Non-Operating Income and Extraordinary Loss: Japan

KLab Inc. recorded an extraordinary loss of 670 million yen for the fourth quarter of the 2014 fiscal year, primarily driven by a 607 million yen impairment charge on gaming software assets.

The company reported a net non-operating income of 288 million yen for the same period, bolstered by a 231 million yen foreign-exchange gain.

These financial adjustments represent the first quarterly disclosure of such items for KLab in 2014 and will impact the company's full-year earnings forecast.

Investment

Japan

KLab

Report

8 pages

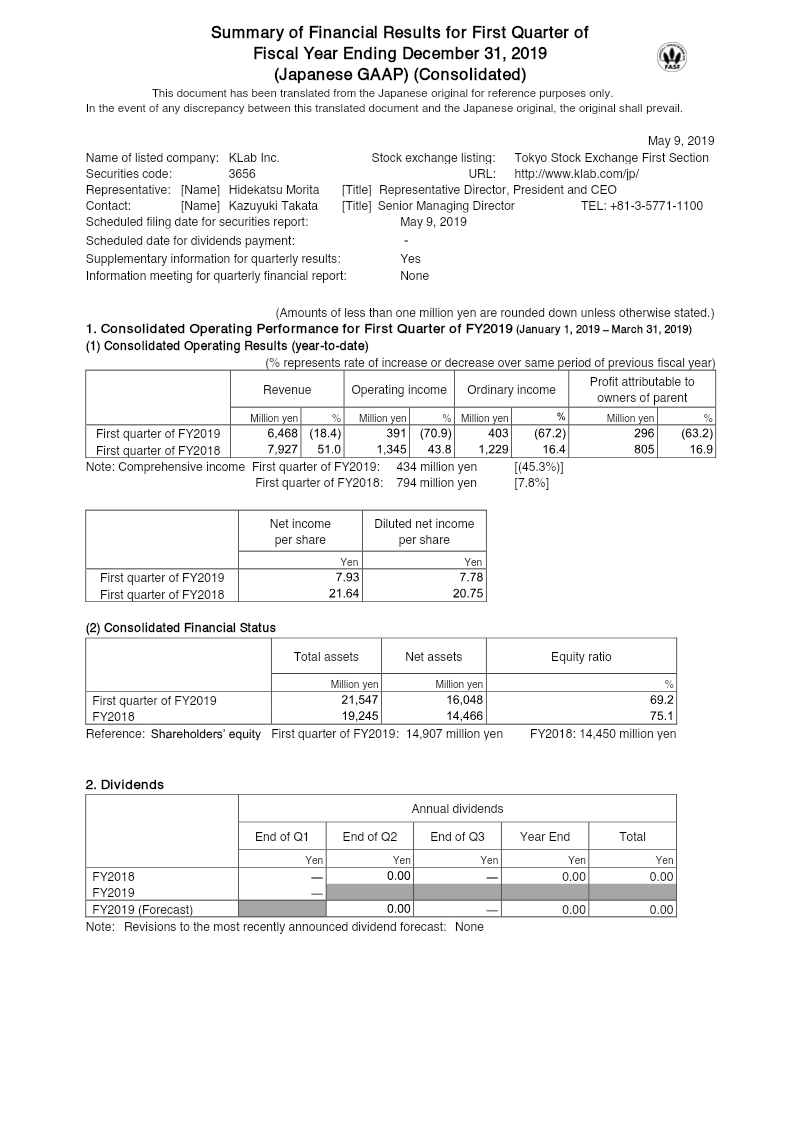

Consolidated Financial Statement: Q1 2019

KLab Inc. experienced a significant Q1 2019 downturn, with revenue falling 18.4% to ¥6,468 million and operating income dropping 70.9% to ¥391 million compared to the same period in 2018.

The primary driver for the revenue decline was a decrease in sales for the 'Love Live! School Idol Festival' title.

Profit attributable to owners of the parent contracted by 63.2% to ¥296 million, while net income fell 65% to ¥303 million.

Market Analysis

Investment

Japan

+1

KLab

Report

8 pages

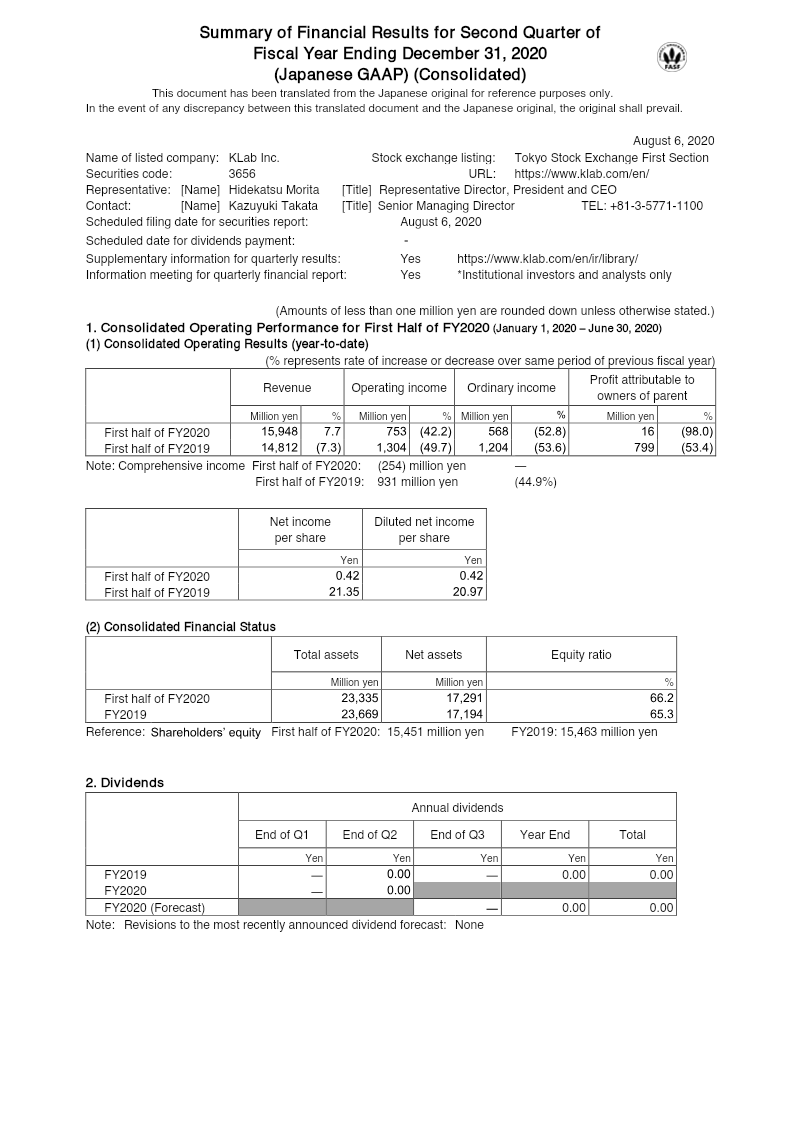

Consolidated Financial Report: Q2 2020

KLab Inc. reported a 98% decline in profit attributable to owners of the parent to ¥16 million for the first half of 2020, compared to the same period in 2019.

Operating income fell 42.2% to ¥753 million, driven by an increased cost of sales and a lower gross profit margin.

Revenue grew by 7.7% to ¥15.95 billion, supported by performance in the company's core game business and research and consulting services.

Market Analysis

Mobile

Japan

+1

KLab

Report

8 pages

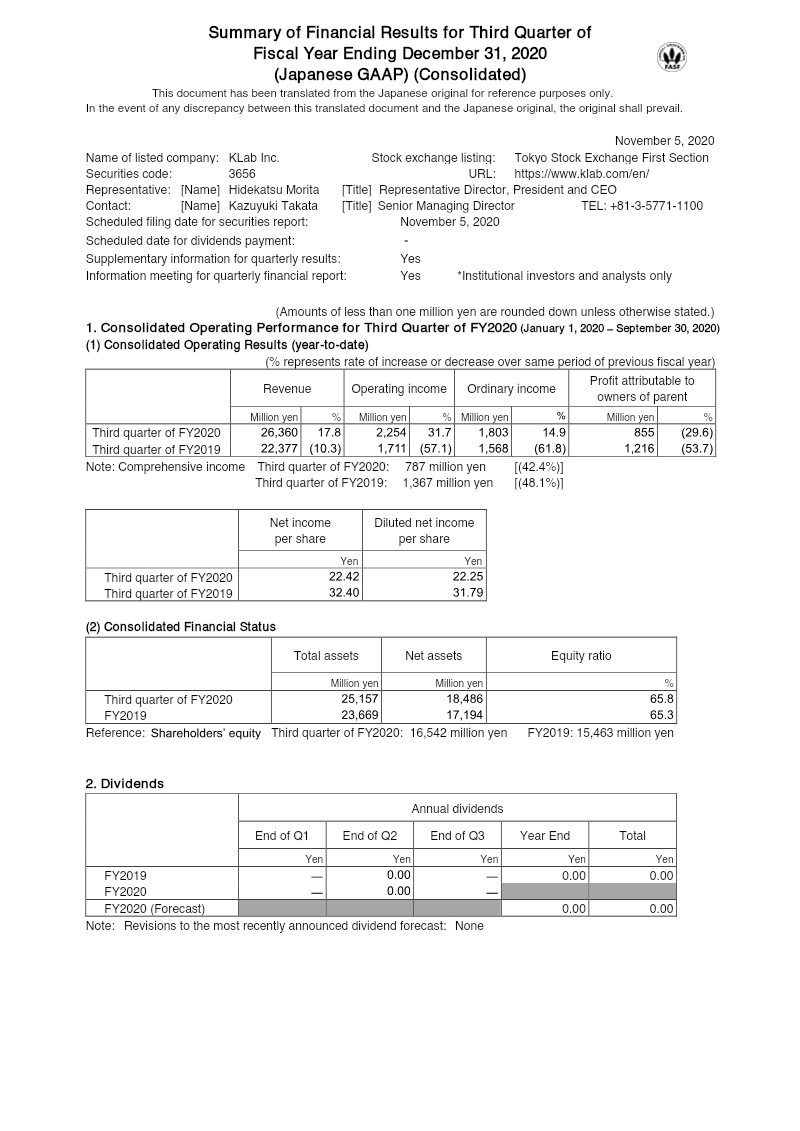

Quarterly Financial Report: Q3 2020

KLab Inc. reported a 17.8% year-over-year revenue increase to ¥26.36 billion for the first nine months of FY2020, driven by strong performance in its game business segment.

Operating income rose 31.7% to ¥2.25 billion, while ordinary income grew 14.9% to ¥1.80 billion compared to the same period in FY2019.

Net profit attributable to the parent fell 29.6% to ¥855 million, primarily due to foreign-exchange losses and a ¥498.9 million impairment charge on investments.

Market Analysis

Investment

Mobile

+1

KLab

Report

9 pages

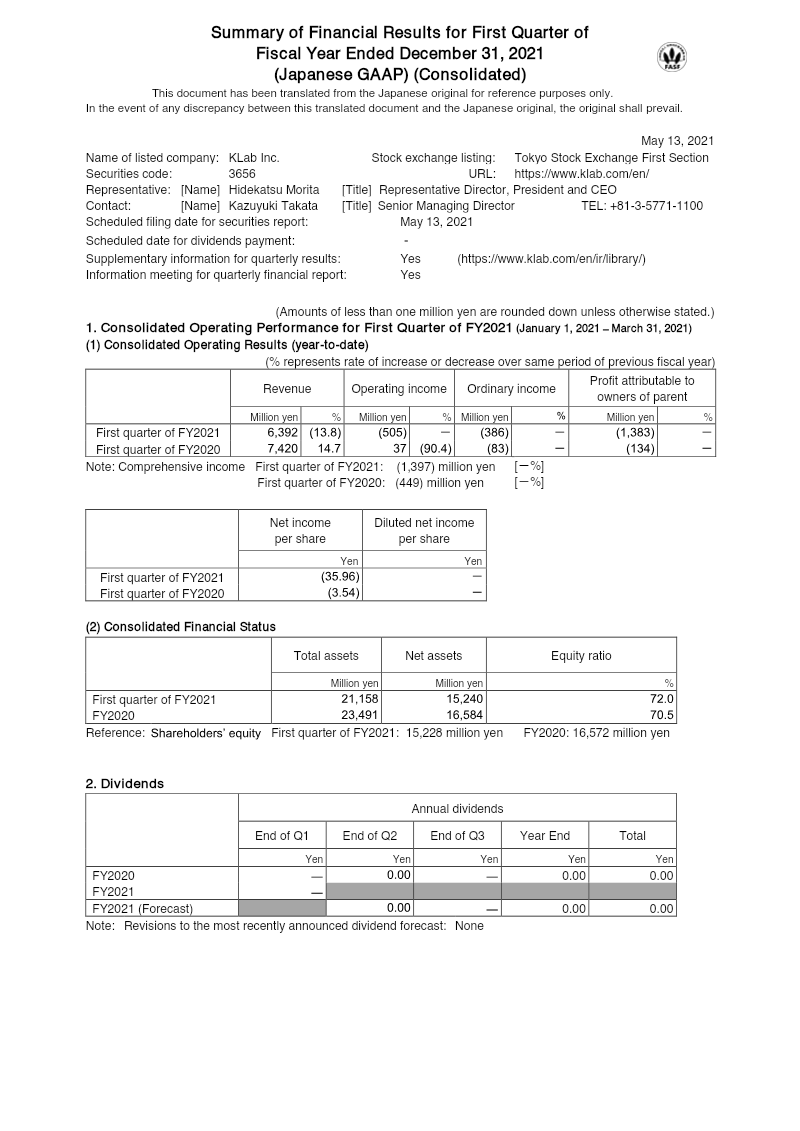

Q1 2021 Financial Statement

KLab Inc. reported a 13.8% year-over-year revenue decline in Q1 2021, falling to ¥6,392 million from ¥7,420 million.

Operating income swung to a ¥505 million loss compared to a ¥37 million profit in the same period of 2020.

The company recorded a significant ¥1.54 billion impairment charge on software assets, which was the primary driver of a ¥386 million loss attributable to the parent company.

Market Analysis

Mobile

Japan

+1

KLab

Report

8 pages

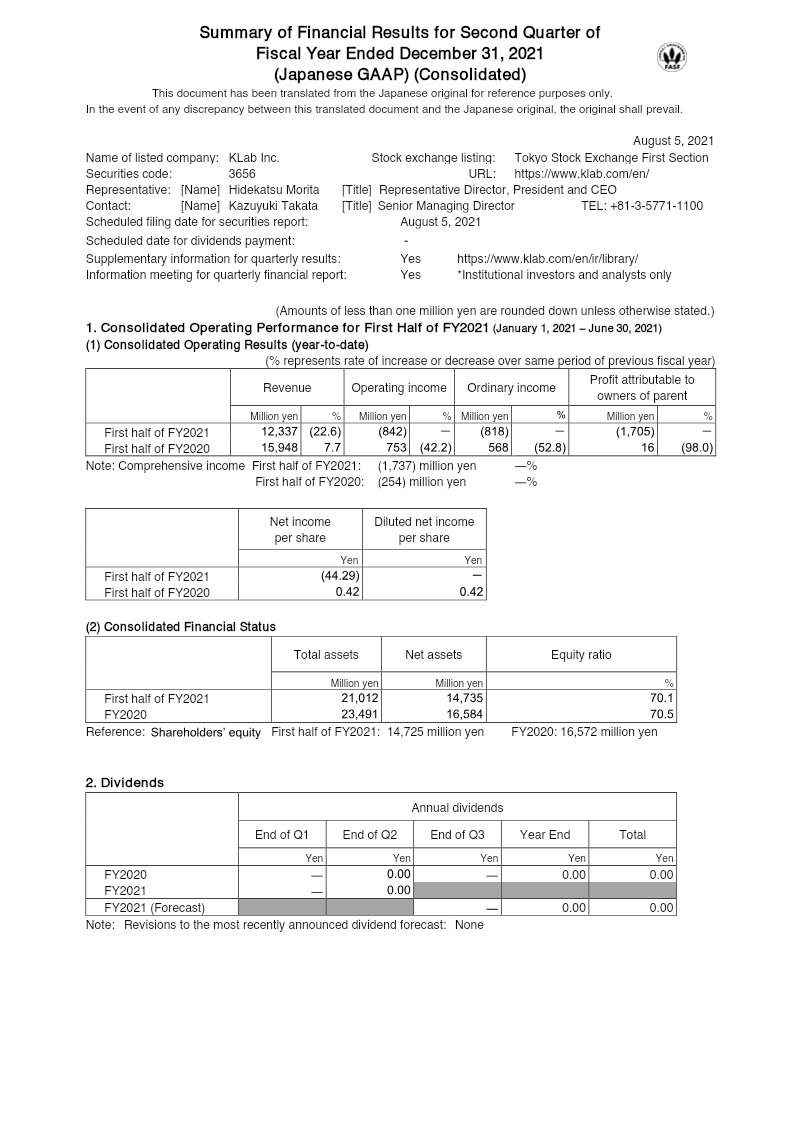

Financial Report: Q2 2021

KLab Inc. experienced a significant financial downturn in H1 2021, with total revenue falling 22.6% year-over-year to ¥12.34 billion.

Operating performance swung from a ¥753 million profit in H1 2020 to an operating loss of ¥842 million in H1 2021.

The company reported a net loss of ¥1.71 billion attributable to owners of the parent, resulting in a loss of ¥44.3 per share compared to a profit of ¥0.42 per share in the prior year.

Market Analysis

Investment

Mobile

+1

KLab

Report

6 pages

GungHo Business Report Vol. 42

GungHo’s overseas sales ratio grew from 39.3% in 2022 to 47.7% in 2024, signaling a successful shift toward international market penetration.

Consolidated net sales decreased from ¥125.3 billion in 2022 to ¥103.6 billion in 2024, with operating profit declining from ¥27.9 billion to ¥17.5 billion over the same period.

The flagship title Puzzle & Dragons has surpassed 63 million global downloads since its 2012 launch and is preparing for a 13th-anniversary release in May 2025.

Game Publishing

Mobile

Console

+4

GungHo Online Entertainment

Report

9 pages

Supplementary Explanatory Materials Regarding the Opinion of the Company’s Board of Directors on Shareholder Proposals: GungHo Online Entertainment

GungHo Online Entertainment’s board has unanimously rejected all shareholder proposals from Strategic Capital and LIM Japan Event Master Fund for the 2026 Annual General Meeting.

The board rejected shareholder-return proposals that would have distributed approximately 57% of the company's cash and deposits, labeling the demand as excessive.

GungHo maintains a capital return policy targeting a 4% dividend-on-equity (DOE) and a minimum 50% consolidated payout ratio, including a ¥90.00 per share dividend for FY 2025.

Investment

Japan

GungHo Online Entertainment

Report

2 pages

Ragnarok Online 3: Service to Begin in Japan

Gravity Co., Ltd. and studio DTDS will launch Ragnarok Online 3 in Japan on February 13, 2026, as a free-to-play MMORPG.

The title will be available across iOS, Android, and PC platforms, featuring in-game purchases and a business model focused on seasonal content updates.

GungHo Online Entertainment will publish the game, which retains core series elements like the job system and atmospheric design while introducing a modernized art style.

Game Publishing

Mobile

PC

+2

GungHo Online Entertainment

Report

50 pages

3Q FY2021 Presentation Material: Japan

The company has revised its FY2021 earnings forecast upward for the second time due to performance exceeding expectations.

Growth in both the games and internet advertisement business segments outperformed initial projections for the third quarter of FY2021.

The reported quarterly results cover the period from April 2021 through June 2021.

Market Analysis

Advertising

Streaming

+2

CyberAgent

Report

26 pages

1Q FY2020 Presentation Material

The company reported 115.6 billion yen in revenue for 1Q FY2020, maintaining a consistent quarterly growth rate between 24% and 28%.

Operating income reached 7.7 billion yen, reflecting a 24–28% year-over-year increase and an operating margin of approximately 32%.

Net profit for the quarter rose 15–18% to 1.4 billion yen, resulting in a net margin of nearly 10%.

Market Analysis

Mobile

Japan

+1

CyberAgent

Report

40 pages

3Q FY2020 Presentation Material: Japan

Financial results for the third quarter of fiscal year 2020, covering the period from April to June 2020, aligned with initial forecasts.

The company successfully met its performance targets for the third quarter despite the operational challenges posed by the COVID-19 pandemic.

The Internet Advertisement Business segment maintained performance levels consistent with expectations throughout the April–June 2020 period.

Market Analysis

Game Publishing

Advertising

+3

CyberAgent

Report

54 pages

FY2020 Presentation Material: October 2019 to September 2020

The fiscal year 2020 reporting period covers the twelve-month duration from October 2019 through September 2020.

The document outlines performance results for the fiscal year 2020 and provides a forward-looking forecast for the fiscal year 2021, spanning October 2020 to September 2021.

The report includes a specific focus on the performance and strategic outlook of the company's internet advertisement business segment.

Market Analysis

In-Game Advertising

Mobile

+1

CyberAgent

Report

44 pages

1Q FY2021 Presentation Material

The internet advertisement and media business achieved record-high sales during the first quarter of fiscal year 2021.

The reported financial results cover the period from October 2020 through December 2020.

Performance in the ads and media sector served as a primary driver for the company's quarterly results.

Market Analysis

Advertising

Game Publishing

+2

CyberAgent

Previous

1

…

5

6

7

…

87

Next