ReportRGDA – Romanian Game Developers Association

The Romanian Video Games Development Industry

1 Jan 20252 pages~1 min full read

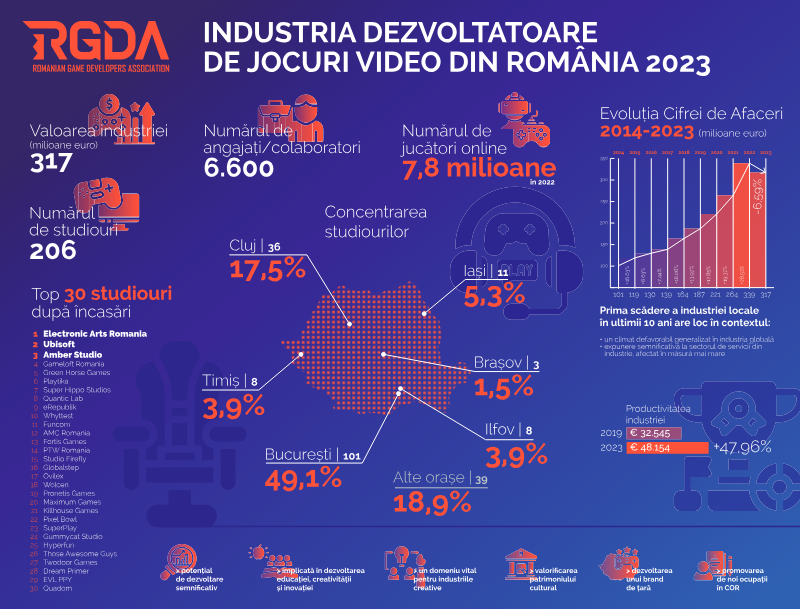

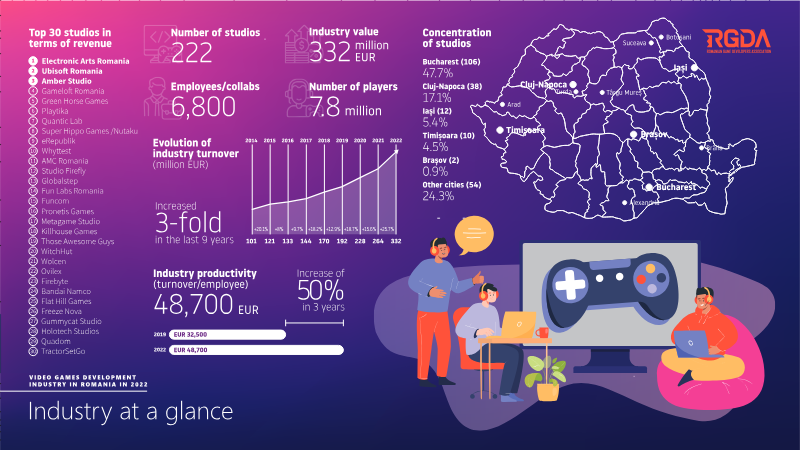

The Romanian video game industry has nearly tripled its turnover in the last decade, growing from approximately €119 million in 2015 to over €340 million in 2024.

The sector’s workforce has expanded at an annual rate of 12%, with total headcount projected to reach 343,160 employees by 2024.

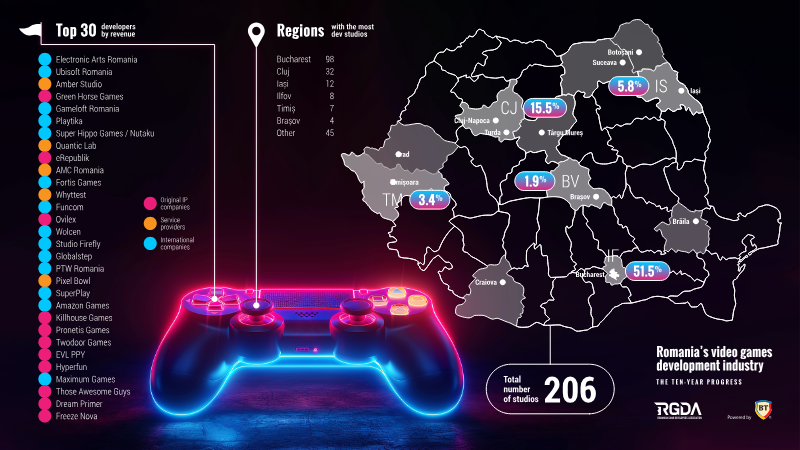

Market dominance is held by major multinational publishers like Electronic Arts in Bucharest and Ubisoft in Cluj-Napoca, while mid-size studios such as Amber, Green Horse Games, and Playtika contribute between 5% and 15% of total earnings.

Industry efficiency has improved alongside growth, with productivity—measured as turnover per employee—increasing by 7.4% over the ten-year period.

The number of active development studios in Romania has increased by 70% since 2015, with operations clustering in major hubs like Bucharest, Cluj-Napoca, Iași, and Brașov.

Service-oriented companies and international providers account for 51.5% of the market, highlighting the country's deep integration into the global video game supply chain through outsourcing and collaboration.

The analysis presents a comprehensive overview of Romania’s video‑game development sector, focusing on revenue performance, geographic concentration, and workforce trends over the past decade. Its central thesis is that the industry has experienced rapid expansion, with total turnover rising from roughly €119 million in 2015 to more than €340 million in 2024, while the number of active studios grew by 70 % within the same period.

Revenue concentration is illustrated by a ranking of the top thirty developers, highlighting that multinational publishers such as Electronic Arts Romania (Bucharest) and Ubisoft Romania (Cluj‑Napoca) dominate the market, together accounting for a substantial share of the €340 million total. Mid‑size studios—including Amber Studio (Iași), Green Horse Games (Ilfov), and Playtika (Brașov)—contribute notable percentages, ranging from 5 % to 15 % of overall earnings. The data also maps studio locations, revealing a strong clustering in Bucharest, Cluj‑Napoca, Iași, and Brașov, with emerging hubs in Timișoara, Turda, and Arad.

Workforce figures show headcount increasing from 279,986 employees in 2015 to a projected 343,160 in 2024, reflecting a 12 % annual growth rate in personnel. Productivity, measured as turnover per employee, rose by 7.4 % over the ten‑year span, indicating that revenue gains are not solely driven by hiring but also by higher efficiency. Service‑oriented companies and international providers together represent 51.5 % of the sector, underscoring the importance of outsourcing and cross‑border collaborations.

The scope encompasses the entire Romanian market, covering all development, publishing, and service activities from 2015 through 2024. Figures appear to be compiled from company‑reported revenues, employee registers, and regional studio counts, suggesting a mixed methodology of financial reporting and industry surveys. Overall, the evidence points to a robust, diversifying ecosystem that is increasingly integrated with the global video‑game supply chain.