Skip to main content

Game Industry

Library

Library

Search

Ask AI

News

Connect your AI

Browse

The Catch Up

Topics

Collections

Writers

Help

Subscribe

Game Industry

Library

Library

Search

Ask AI

Saved

Library

58 reports matching your filters

All Types

Reports

Articles

Presentations

Whitepapers

Financial

Legal

Other

Search

AI

Global

Market Analysis

Marketing

Mobile

Game Development

User Acquisition

Advertising

Monetization

Creative Ads

Game Design

Investment

Employment

Player Behavior

Console

Market Forecast

PC

Mergers & Acquisitions

Clear

Filters

1

AI

Recently added

Newest first

Oldest first

Title A–Z

Title Z–A

Report

19 pages

How Developers Are Using Generative AI to Create a New Generation of Games

Generative AI adoption is near-universal, with 97% of 615 surveyed developers believing it is transforming the industry and 90% already integrating it into their workflows.

AI agents are becoming a core development pillar, with 44% of developers using them for content optimization and 38% each for dynamic gameplay tuning and in-game coaching.

Player expectations are shifting rapidly, as 89% of developers report that gamers now explicitly demand smarter, more adaptive, and personalized gaming experiences.

Market Analysis

Game Development

AI

+1

InvestGame

Report

90 pages

AI Eats the World

Hyperscaler capital expenditure is projected to reach $350 billion in 2025, nearly doubling 2024 levels as data-center investment outpaces office construction.

Silicon supply constraints at Nvidia and TSMC, combined with power and permitting limitations, represent the primary bottlenecks threatening to throttle AI growth.

Despite 800 million weekly active users, the paying-user base for AI models remains at approximately 5%, highlighting a significant gap in monetization.

Market Analysis

AI

Global

+1

Benedict Evans

Whitepaper

41 pages

What Good Are AI NPCs?: Lessons from a Large-scale Player Study

Generative AI NPCs drive high player engagement, with 97% of participants reporting high immersion and 96% rating their overall enjoyment as high.

The integration of AI NPCs maintains a balance between agency and guidance, as evidenced by 80% of players achieving top scores for play engrossment and 90% praising the creative freedom of the open-ended design.

Cognitive load remains manageable during AI-driven interactions, with participants reporting NASA-TLX mental demand scores of 64.7 and performance scores of 52.7.

AI

Game Design

Player Behavior

+2

University of Bristol

Presentation

16 pages

AI in MTG: Moving Beyond Theory

Adopting an 'AI-first' development approach enabled the launch of five new mobile games in 2026, facilitating rapid iteration and simultaneous production of specialized content.

AI integration has achieved significant operational efficiencies, including a 99% reduction in marketing asset costs and an 80% time saving on influencer spotlight production.

Data analysis turnaround times have been reduced by 75% by utilizing AI agents to query large-scale datasets, allowing analysts to focus on high-level strategy.

AI

Game Development

Midcore

+2

Modern Times Group

Whitepaper

10 pages

2026 Global Mobile App Marketing Trends White Paper

The mobile app market has shifted from volume-based growth to a quality-focused model, evidenced by a 16.7% YoY decline in active advertisers alongside a 73.3% surge in creatives per advertiser.

Global user acquisition spend grew 13% YoY to $78 billion, with the increase driven almost exclusively by iOS advertising.

Video remains the dominant advertising format, accounting for approximately 70% of social media inventory, while static and playable ads are relegated to testing and engagement signaling.

Market Analysis

Mobile

Marketing

+3

SocialPeta

Apr 2026

Report

97 pages

State of Mobile 2026

Non-game apps surpassed games in in-app purchase (IAP) revenue for the first time in 2025, contributing to a total global IAP market of $85.6 billion, a 21% year-over-year increase.

Generative AI and short-form drama are the fastest-growing subgenres, with AI assistants like ChatGPT generating $3.4 billion in 2025 and short-drama apps capturing over 10% of global video-entertainment time.

Roblox solidified its dominance in the gaming web arena, accounting for 74% of all game-publisher site visits in 2025.

Market Analysis

Monetization

AI

Sensor Tower

Apr 2026

Report

52 pages

State of the Game Industry 2026

Layoffs remain a critical industry issue, with two-thirds of AAA studio employees reporting company-wide cuts and nearly 20% of the total workforce having been personally let go.

Workplace culture remains characterized by persistent crunch, as 87% of employees clocked overtime in the past year, largely driven by perceived necessity or self-imposed pressure.

Generative AI adoption is deeply polarized, with 42% of professionals viewing it as a productivity tool while 38% fear it poses ethical risks and threats to job security.

Market Analysis

AI

Global

GDC

Apr 2026

Report

33 pages

The Future of Consumer Apps: How AI and Game Design Principles Are Reshaping Every Category

Non-gaming mobile app revenue is projected to reach $150 billion by 2030, with spending in this sector already surpassing traditional gaming apps as of 2025.

AI-driven gamification is the primary catalyst for revenue and engagement, with BITKRAFT forecasting at least five non-gaming consumer companies will exceed $10 billion valuations by 2035.

High-friction sectors are successfully using game mechanics to drive retention; for example, fintech platforms like StockGro use leaderboards and AI-personalized tutorials to convert financial discipline into instant gratification.

Market Analysis

AI

Game Design

+2

BITKRAFT Ventures

Mar 2026

Report

95 pages

2023 Integrated Report: Value Creation Story

The organization has defined its core strategic vision as becoming the world's premier provider of internet and AI technology.

The company's stated mission is to entertain and enrich lives while serving to improve the world.

The business model relies on leveraging individual employee strengths to drive the success of its unique business units.

AI

Japan

Mobile

+1

DeNA Co.

Report

11 pages

FOCUS: ACC South Florida 2026

The OBBBA has introduced new financial incentives relevant to the South Florida business landscape.

The integration of AI in the sports and entertainment industries presents evolving operational risks that require proactive management strategies.

Practical frameworks are available for mitigating legal risks associated with post-transaction M&A disputes.

AI

Mergers & Acquisitions

USA

ACC South Florida

Report

2 pages

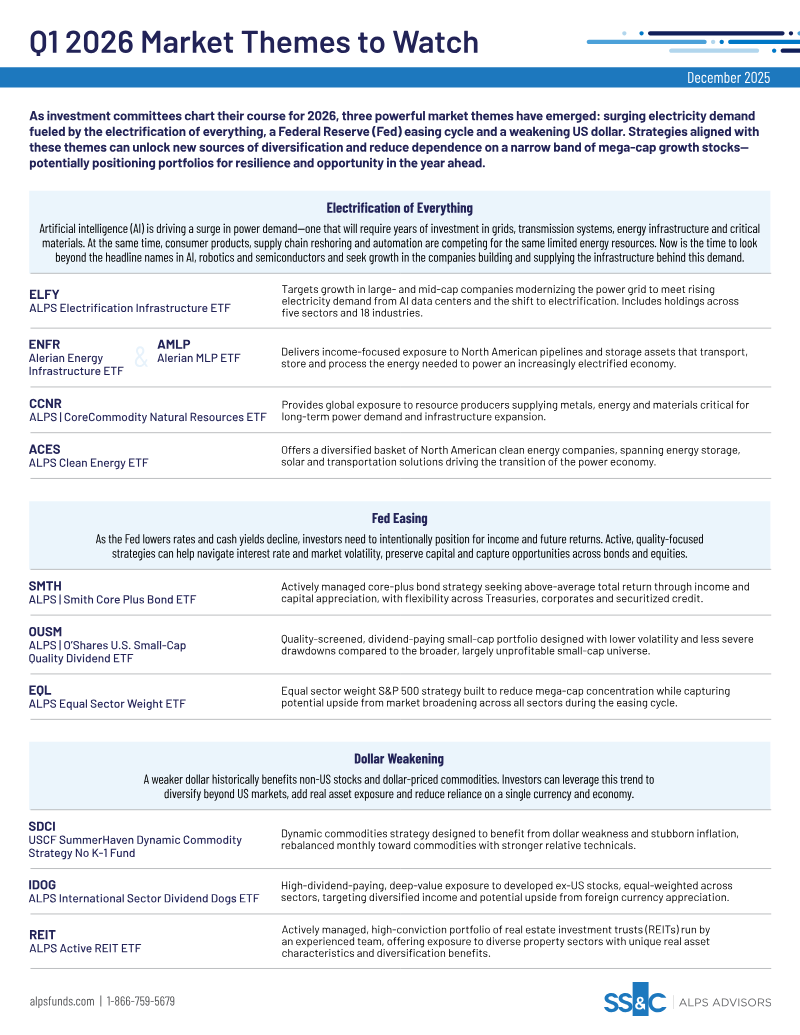

Q1 2026 Market Themes to Watch

Investors should pivot from mega-cap growth stocks toward infrastructure assets that support the electrification of the economy, including grid modernization, energy transmission, and critical material supply chains.

The surge in power demand driven by AI, data centers, and industrial automation necessitates capital allocation into North American energy pipelines, clean energy solutions, and global natural resource producers.

The Federal Reserve’s interest rate easing cycle requires a shift toward quality-oriented income strategies, such as active fixed-income management and dividend-paying small-cap equities, to replace declining cash yields.

Market Analysis

Market Forecast

Investment

+2

GameVault System

Report

17 pages

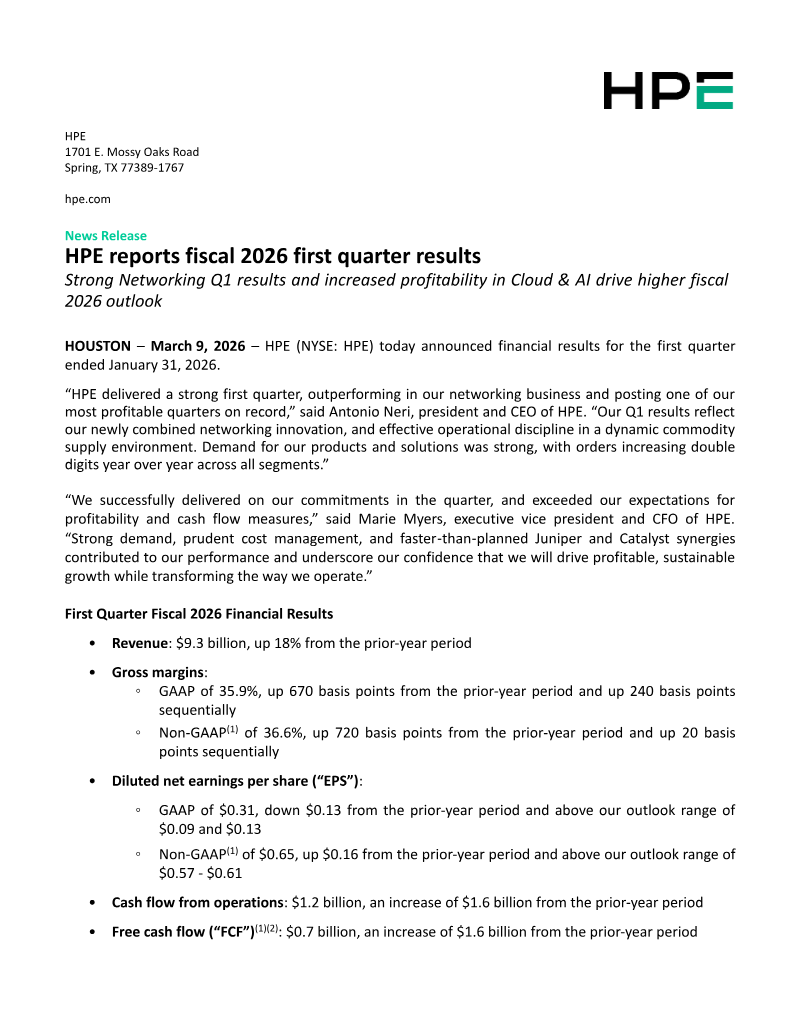

HPE Fiscal 2026 First Quarter Results

HPE reported strong financial results for the first quarter of fiscal 2026, ending March 9, 2026.

The company achieved one of its most profitable quarters on record during the first quarter of fiscal 2026.

Networking business performance exceeded expectations, serving as a primary driver for the quarter's strong results.

Market Analysis

AI

Investment

+1

Hewlett Packard Enterprise

Report

47 pages

IBM 2020 Corporate Responsibility Report

The year 2020 served as a catalyst for organizational and individual adaptation in response to global challenges.

The report emphasizes that periods of crisis drive human ingenuity and the reinvention of existing operational models.

Societal challenges faced during 2020 acted as a primary driver for testing the resolve and adaptability of global organizations.

AI

Diversity & Inclusion

Employment

+1

IBM

Report

10 pages

Winning on Google Discover: A Data-Driven Guide for Gaming Media

Google Discover now accounts for roughly 50% of Google traffic for gaming sites within the Raptive network, following a February 5, 2026 core update that shifted traffic away from traditional search.

Sites that prioritize high U.S. traffic concentration, deep session depth, and structured editorial content like guides and databases experience superior Discover performance and revenue stability.

Following the February 2026 update, 20% more gaming sites began receiving Discover feed impressions, with smaller publishers seeing notable traffic growth.

Market Analysis

Marketing

Advertising

+2

Raptive

Mar 2026

Report

31 pages

The Dual Frontier: A Retailer’s Framework for Agentic Commerce

Retailers must prioritize high-quality, structured catalog data, as insufficient data in an agentic environment causes total exclusion from a shopper's consideration set rather than just lower conversion rates.

A 32-point readiness diagnostic across four pillars—catalog, infrastructure, organizational capacity, and strategic urgency—determines the viability of agentic commerce, with scores of 26–32 indicating immediate readiness and 0–9 requiring foundational work.

Retailers should adopt a calibrated data-sharing strategy, categorizing signals into 'share freely,' 'share selectively,' and 'protect' to balance recommendation accuracy with the need to safeguard proprietary competitive advantages.

Market Analysis

AI

Monetization

+2

InvestGame

Feb 2026

Report

38 pages

The AI Disruption Index: How AI Is Reshaping Consumer Discovery

One-third of U.S. adults now use personal AI agents for product discovery, while nearly 50% utilize AI for purchase research.

AI-driven 'zero-click' discovery is actively eroding traditional paid search and organic search channels, threatening sectors like retail, education, and health & fitness.

Sectors with strong regulatory or content moats, specifically financial services, media rights holders, and auto OEMs, currently maintain a defensive advantage against AI disintermediation.

Market Analysis

Marketing

AI

+2

InvestGame

Jan 2026

Report

36 pages

Winning with Creative: Building, Testing, and Scaling High-Performance Ads

High-performance ads achieve a 350% lift in ad spend when winning templates are paired with top-performing assets.

TikTok-first video structures—comprising a hook, body, and close—can increase purchase intent by up to 77% when using 30-second, sound-on formats.

AI-driven content creation tools, such as TikTok Symphony, provide a 57% efficiency gain in the production process.

Marketing

Advertising

Creative Ads

+3

Moloco

Jan 2026

Report

41 pages

Mobile App Trends: 2026 Edition

The mobile app economy reached $167 billion in consumer spending in 2025, supported by a 10% year-over-year increase in global installs and a 7% rise in sessions.

Gaming installs remained flat while costs per install surged 30% to $0.56, though casual games bucked the trend with a 19% increase in installs and a 37% rise in sessions.

The industry is shifting from mobile-first to multi-platform strategies to address fragmented consumer journeys, supported by AI-driven predictive segmentation and cross-device measurement.

Market Analysis

User Acquisition

AI

+2

Adjust

Jan 2026

Whitepaper

90 pages

2026 Global Mobile Apps Marketing Trends

The mobile marketing landscape has shifted from media-centric targeting to creative-driven acquisition, evidenced by a 73.3% surge in creative output per advertiser alongside a 16.7% decline in the total number of active advertisers.

Playable ads are currently the top-performing format, consistently delivering the highest conversion metrics, scroll-stop rates, and attention duration.

The AI application sector underwent a significant contraction in 2025, with the number of active advertisers dropping by 48%.

Market Analysis

Mobile

Marketing

+4

SocialPeta

Jan 2026

Report

26 pages

2026 Predictions: Trends in Gen AI, Gaming & Digital Ad Spend

Generative AI apps will become a top-five category by 2026, generating over $10 billion in IAP revenue, 7.2 billion downloads, and 43 billion hours of usage, representing an 82% year-over-year growth.

By the end of 2026, generative AI traffic will surpass paid sources on more than 50% of the top 1,000 U.S. websites, up from 37% in late 2025.

Short-drama vertical video is projected to overtake traditional OTT streaming in download volume, capturing roughly 80% of total downloads with rapid adoption in India, Indonesia, and Brazil.

Market Forecast

AI

Advertising

+1

Sensor Tower

Jan 2026

Previous

1

2

3

Next