ReportGDACZ – Czech Game Developers Association

Czech Video Game PC, Console and Mobile Game Developers in Czech Republic 2020

1 Jan 202045 pages~96 min full read

The Czech video game industry experienced rapid growth between 2017 and 2020, with annual turnover rising from CZK 2.26 billion to over CZK 5 billion, representing a 29% average annual growth rate.

See it on page 23The sector is highly export-oriented, with approximately 95% of revenue generated from international markets, primarily the United States, Germany, and the United Kingdom.

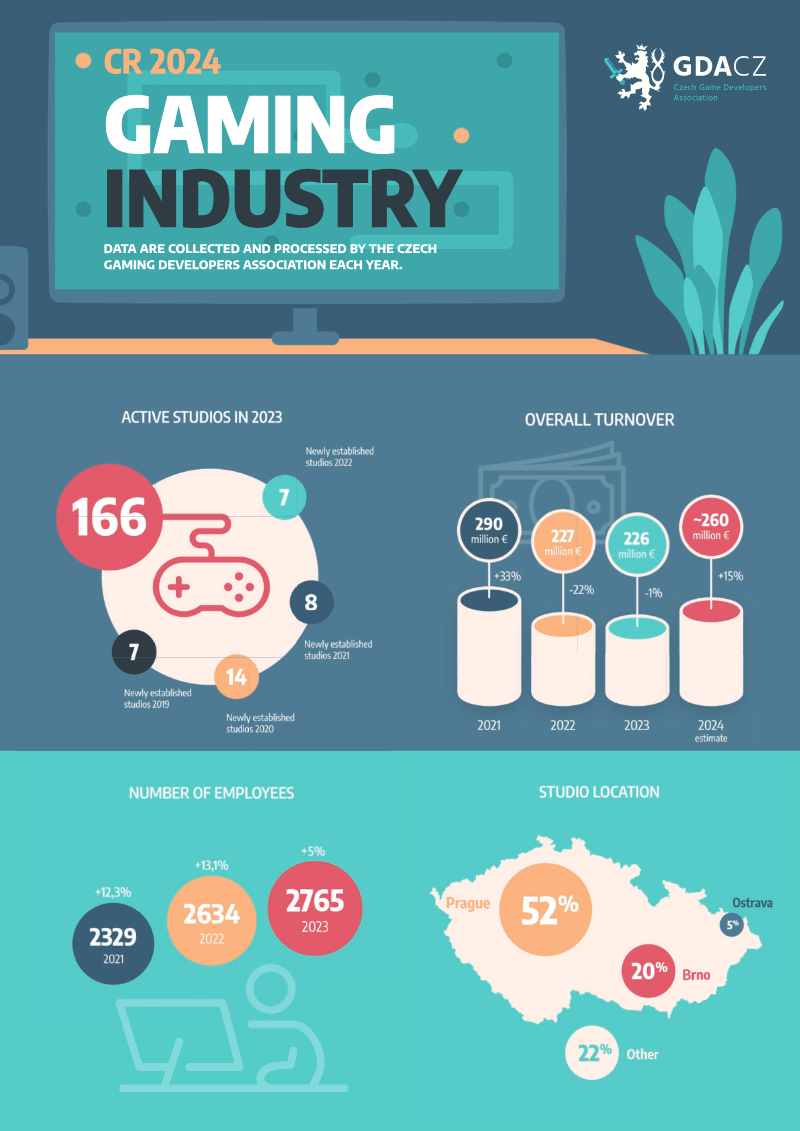

See it on page 27As of 2020, the industry comprised roughly 110 domestic studios employing 1,750 specialists, with revenue already tripling that of the national film industry by 2019.

See it on page 7The publishing landscape has shifted away from traditional full-development financing toward a model where publishers primarily handle marketing and launch, while online platforms have marginalized physical distribution.

See it on page 12Human capital remains a critical bottleneck due to a fragmented education pipeline and intense competition for skilled talent, compounded by a lack of dedicated public subsidies for research and development compared to neighboring countries.

See it on page 36Domestic consumer behavior is characterized by an average gamer age of 33, a 33% female player base, and annual domestic spending of approximately CZK 4 billion, with a strong preference for story-driven titles.

See it on page 31The study maps the structure and dynamics of the Czech video‑game industry as of 2020, highlighting its rapid export‑driven expansion and the strategic challenges it faces in talent development and public support. The sector comprises roughly 110 domestic development studios, of which only a small fraction are foreign branches, employing about 1,750 specialists. Turnover rose from CZK 2.26 billion in 2017 to over CZK 5 billion in 2020, equivalent to more than €190 million, reflecting an average annual growth rate of 29 % over the previous five years and an export share near 95 % to markets such as the United States, Germany and the United Kingdom. Revenue in 2019 already surpassed €169 million, outpacing the national film industry by a factor of three, and the market is projected to exceed €190 million in 2020.

The analysis of the publishing and distribution landscape shows a shift away from traditional full‑development financing toward a model where publishers act mainly as marketing and launch partners, while online platforms now dominate the transaction chain, reducing costs and marginalising physical distributors, of which only ten remain active in the country. Consumer data reveal an average gamer age of 33, a gender split of one‑third women, and annual spending of roughly CZK 4 billion, with a strong preference for story‑driven titles.

Human‑capital constraints emerge as a critical bottleneck: the industry confronts intense competition for skilled staff, a fragmented education pipeline, and limited visibility of creative industries within public policy. Unlike neighboring Poland and Germany, which allocate substantial public funds to game‑industry support, the Czech Republic offers virtually no dedicated subsidies for research, development or innovation, despite the sector’s outsized contribution to national exports. The findings suggest that sustained growth will depend on coordinated investment in education, clearer industry‑government linkages, and targeted public financing to bolster the sector’s competitive edge.