Report4 pages

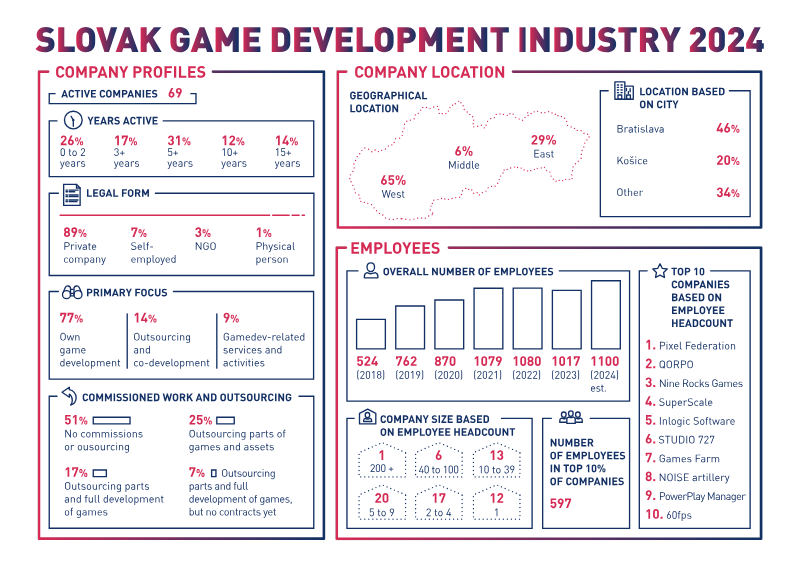

Company Profiles: Slovakia 2024

- The Slovak game industry is highly concentrated, with the top 10% of companies—including Pixel Federation and Nine Rocks Games—generating 83.5% of the sector's 70 million EUR annual turnover.

- The industry consists of 69 active companies, 77% of which focus on original game development rather than outsourcing services.

- After a slight contraction in 2023, the workforce is projected to reach approximately 1,100 employees by the end of 2024, with a median age of 31 and 21% female representation.

Swiss Game Developers AssociationJan 2024

Presentation5 pages

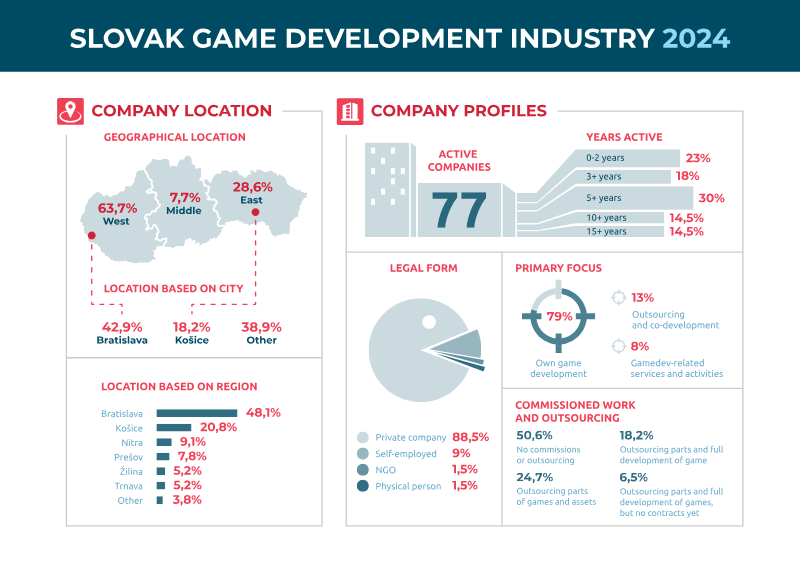

Slovak Game Industry Infographic 2024

- The Slovak game industry generated 67.8 million euros in total turnover in 2024, with high market concentration where the top 10% of companies account for over 83% of total revenue.

- The sector employs 982 professionals with a median age of 30–35, and while male-dominated, women comprise nearly 20% of the workforce, primarily in visual arts and marketing.

- Self-funding is the primary financial model for 80.5% of companies, indicating a reliance on internal capital over public funding or international publishing deals.

Slovak Game Developers AssociationJan 2024

Report4 pages

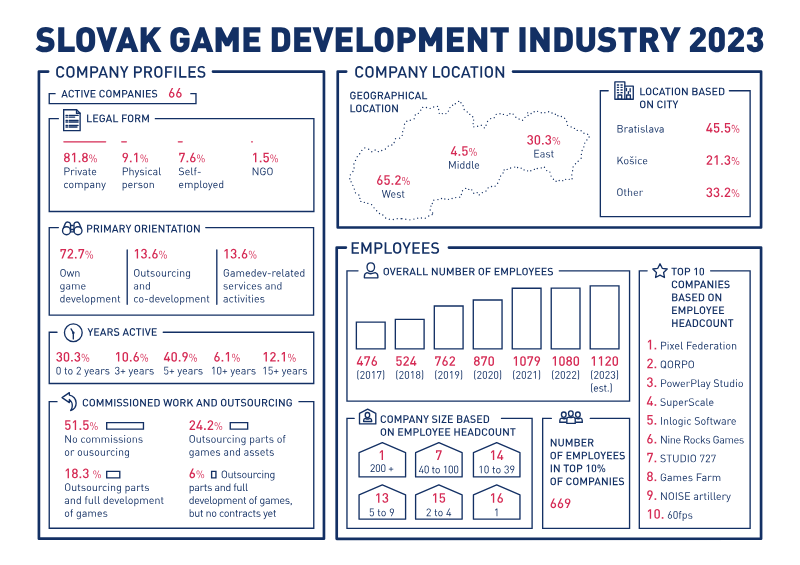

Slovak Game Development Industry 2023

- The Slovak game industry is highly centralized, with the top 10% of companies accounting for 60% of the 1,120-person workforce and 84.6% of the total annual turnover.

- Industry revenue has plateaued, with turnover reaching €77.1 million in 2022 and an estimated €76.9 million in 2023.

- Pixel Federation, SuperScale, and Inlogic Software are the dominant market leaders in both headcount and revenue.

Slovak Game Developers AssociationJan 2023

Report65 pages

Slovak Game Industry Report 2022

- The Slovak game industry faces significant financial headwinds due to spiraling inflation and a reduced availability of free capital.

- Post-IDFA (Identifier for Advertisers) changes have made game marketing increasingly challenging for developers.

- Current economic conditions, characterized by inflation and capital scarcity, are creating a high-difficulty environment for industry growth and sustainability.

Slovak Game Developers AssociationJan 2022

Presentation1 pages

Slovak Game Industry Infographic

- The Slovak game industry experienced significant workforce expansion between 2016 and 2019, growing from 436 to 762 employees.

- The top ten companies in the sector generated over 48 million euros in annual turnover as of 2019.

- The industry is geographically concentrated, with 52 percent of the 55 active companies based in Bratislava and 24 percent in Košice.

Slovak Game Developers AssociationJan 2020

Report63 pages

Slovak Game Industry Annual Report 2020/2021

- The Slovak game development industry maintained operational continuity and development output throughout the 2020 period despite the challenges of the global pandemic.

- Slovak game studios demonstrated resilience by continuing to support the industry association while simultaneously managing their internal development pipelines during 2020.

- The 2020/2021 report highlights the critical role of individual dedication and studio-level commitment in sustaining the national game development sector during unprecedented times.

Slovak Arts CouncilJan 2020

Report45 pages

Slovak Game Industry 2019

- The 2019 report serves as the inaugural comprehensive census of the Slovak game development industry.

- The monitoring project was established to provide guidance and orientation for stakeholders within the Slovak digital games sector.

- The initial census results confirmed that the industry monitoring framework is effectively tracking the development of the local market.

Slovak Game Developers AssociationJan 2019