Skip to main content

Game Industry

Library

Library

Search

Ask AI

News

Connect your AI

Browse

The Catch Up

Topics

Collections

Writers

Help

Subscribe

Game Industry

Library

Library

Search

Ask AI

Saved

Library

1,251 reports matching your filters

All Types

Reports

Articles

Presentations

Whitepapers

Financial

Legal

Other

Search

Market Analysis

Global

Mobile

Monetization

Investment

PC

Game Publishing

Marketing

Player Behavior

Console

Steam

Game Development

User Acquisition

Player Demographics

Employment

Europe

Mergers & Acquisitions

Japan

Clear

Filters

1

Market Analysis

Recently added

Newest first

Oldest first

Title A–Z

Title Z–A

Report

9 pages

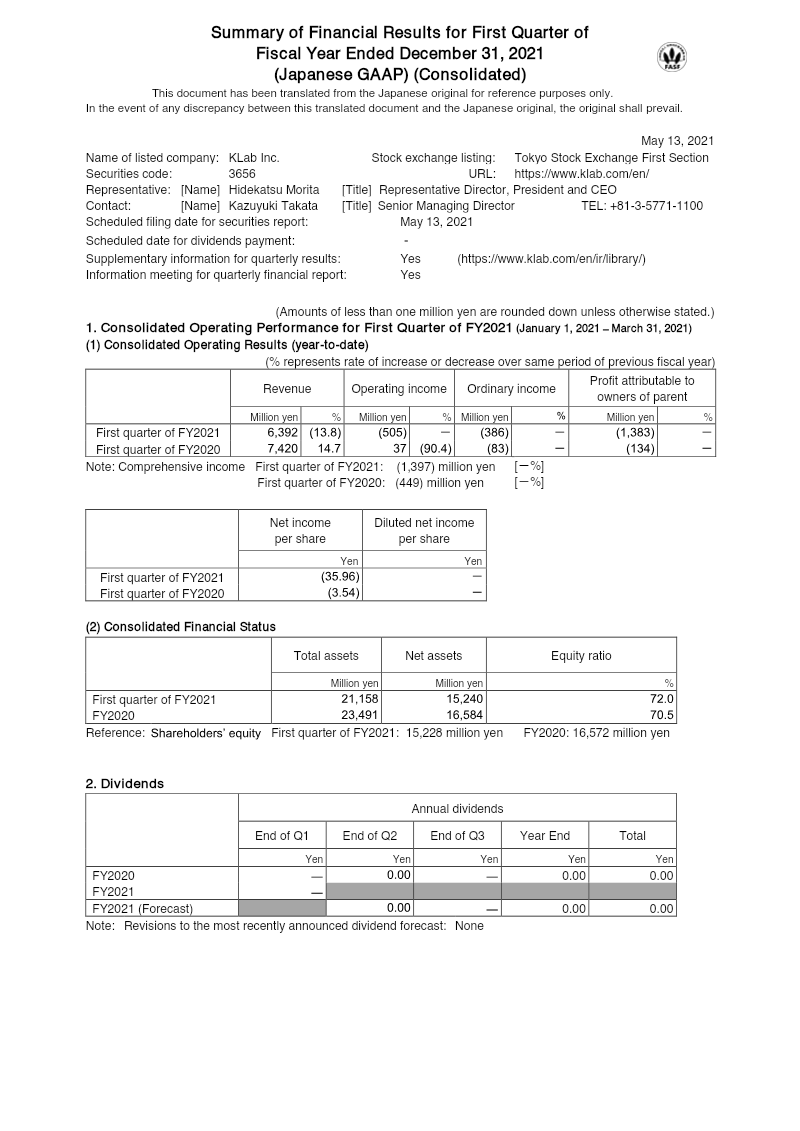

Q1 2021 Financial Statement

KLab Inc. reported a 13.8% year-over-year revenue decline in Q1 2021, falling to ¥6,392 million from ¥7,420 million.

Operating income swung to a ¥505 million loss compared to a ¥37 million profit in the same period of 2020.

The company recorded a significant ¥1.54 billion impairment charge on software assets, which was the primary driver of a ¥386 million loss attributable to the parent company.

Market Analysis

Mobile

Japan

+1

KLab

Report

8 pages

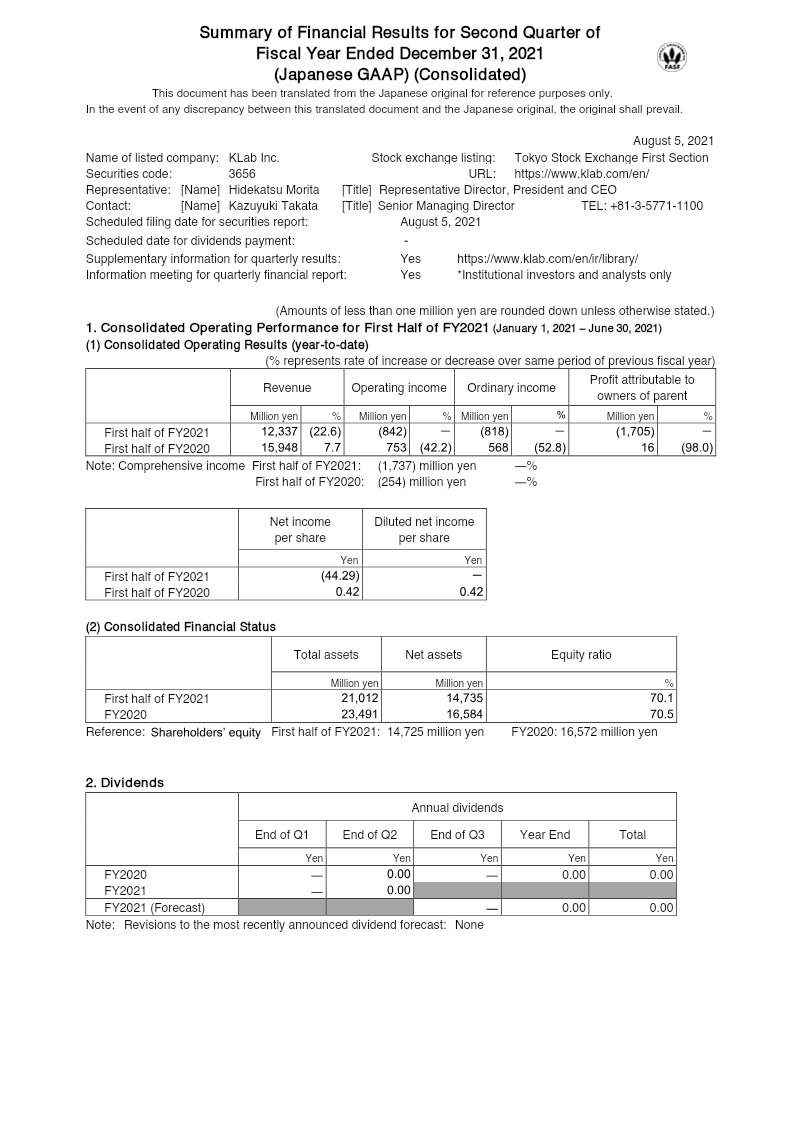

Financial Report: Q2 2021

KLab Inc. experienced a significant financial downturn in H1 2021, with total revenue falling 22.6% year-over-year to ¥12.34 billion.

Operating performance swung from a ¥753 million profit in H1 2020 to an operating loss of ¥842 million in H1 2021.

The company reported a net loss of ¥1.71 billion attributable to owners of the parent, resulting in a loss of ¥44.3 per share compared to a profit of ¥0.42 per share in the prior year.

Market Analysis

Investment

Mobile

+1

KLab

Report

50 pages

3Q FY2021 Presentation Material: Japan

The company has revised its FY2021 earnings forecast upward for the second time due to performance exceeding expectations.

Growth in both the games and internet advertisement business segments outperformed initial projections for the third quarter of FY2021.

The reported quarterly results cover the period from April 2021 through June 2021.

Market Analysis

Advertising

Streaming

+2

CyberAgent

Report

26 pages

1Q FY2020 Presentation Material

The company reported 115.6 billion yen in revenue for 1Q FY2020, maintaining a consistent quarterly growth rate between 24% and 28%.

Operating income reached 7.7 billion yen, reflecting a 24–28% year-over-year increase and an operating margin of approximately 32%.

Net profit for the quarter rose 15–18% to 1.4 billion yen, resulting in a net margin of nearly 10%.

Market Analysis

Mobile

Japan

+1

CyberAgent

Report

40 pages

3Q FY2020 Presentation Material: Japan

Financial results for the third quarter of fiscal year 2020, covering the period from April to June 2020, aligned with initial forecasts.

The company successfully met its performance targets for the third quarter despite the operational challenges posed by the COVID-19 pandemic.

The Internet Advertisement Business segment maintained performance levels consistent with expectations throughout the April–June 2020 period.

Market Analysis

Game Publishing

Advertising

+3

CyberAgent

Report

54 pages

FY2020 Presentation Material: October 2019 to September 2020

The fiscal year 2020 reporting period covers the twelve-month duration from October 2019 through September 2020.

The document outlines performance results for the fiscal year 2020 and provides a forward-looking forecast for the fiscal year 2021, spanning October 2020 to September 2021.

The report includes a specific focus on the performance and strategic outlook of the company's internet advertisement business segment.

Market Analysis

In-Game Advertising

Mobile

+1

CyberAgent

Report

44 pages

1Q FY2021 Presentation Material

The internet advertisement and media business achieved record-high sales during the first quarter of fiscal year 2021.

The reported financial results cover the period from October 2020 through December 2020.

Performance in the ads and media sector served as a primary driver for the company's quarterly results.

Market Analysis

Advertising

Game Publishing

+2

CyberAgent

Report

52 pages

2Q FY2021 Presentation Material

The company reported positive performance across both its game and internet advertisement business segments during the second quarter of fiscal year 2021.

The quarterly results period covered in the report spans from January 2021 through March 2021.

The report explicitly identifies the internet advertisement business as a key operational focus for the 2021 fiscal year.

Market Analysis

Advertising

Streaming

+2

CyberAgent

Report

43 pages

1Q FY2022 Presentation Material

The company reported a strong start for both sales and operating profit in the first quarter of fiscal year 2022.

The financial results cover the period from October to December 2021.

The report outlines the performance and strategic outlook for the company's Internet Advertisement Business.

Market Analysis

Investment

Advertising

+2

CyberAgent

Report

41 pages

FY2022 Presentation Material: Japan

CyberAgent’s ABEMA streaming platform achieved a 7.8% quarterly growth in user engagement, driven by high-profile sports broadcasts like the 2022 FIFA World Cup and Premier League.

Original programming on ABEMA contributed to a 4.69 billion-yen increase in operating income during FY 2022.

The company is executing a long-term growth strategy centered on monetizing digital media and gaming through a combination of advertising, subscription models, and cross-business synergies.

Market Analysis

Japan

Mobile

CyberAgent

Report

43 pages

3Q FY2022 Presentation Material: Japan

Game sales for the period of April to June 2022 declined compared to the peak performance of titles released in the previous year.

The company's financial results for 3Q FY2022 are subject to potential material differences from initial forecasts due to various underlying assumptions.

The report outlines performance metrics across three primary segments: quarterly results, the internet advertisement business, and medium to long-term strategy for FY2022.

Market Analysis

Advertising

Game Publishing

+2

CyberAgent

Report

30 pages

1Q FY2023 Presentation Material

CyberAgent achieved an 8.3% year-over-year revenue increase and an operating profit of ¥6.4 billion in 1Q FY2023.

Operating profit margins improved to 6.7% from 5.9% the previous year, supported by a gross margin increase from 55% to 57%.

Overseas subscriber acquisition grew by 12%, with the United States and Southeast Asia identified as the primary growth markets.

Market Analysis

Monetization

Japan

+1

CyberAgent

Report

40 pages

2Q FY2023 Presentation Material: Japan

The company achieved a new record high for quarterly sales during the second quarter of fiscal year 2023.

The financial reporting period for the second quarter of fiscal year 2023 covers the months of January through March 2023.

The report outlines performance and strategic outlooks across three primary areas: financial summaries, the internet advertisement business, and medium to long-term corporate strategy.

Market Analysis

Monetization

Advertising

+2

CyberAgent

Report

54 pages

FY2023 Presentation Material

The company's fiscal year covers the period from October 2022 through September 2023.

Management has established a forward-looking forecast for the fiscal year spanning October 2023 to September 2024.

The report outlines performance and strategic outlooks for the company's Internet Advertisement Business.

Market Analysis

Market Forecast

Advertising

+1

CyberAgent

Report

45 pages

3Q FY2023 Presentation Material: Japan

The company reported financial results for the third quarter of fiscal year 2023, covering the period from April to June 2023.

The Media and Ads segment achieved a year-over-year increase in sales during the third quarter of fiscal year 2023.

The report outlines a medium to long-term strategy for the remainder of fiscal year 2023.

Market Analysis

Investment

Advertising

+2

CyberAgent

Report

34 pages

1Q FY2024 Presentation Material

CyberAgent returned to profitability in 1Q FY2024 with ¥6.28 billion in operating profit, a significant recovery from the prior year's loss, on consolidated sales of ¥193 billion.

The company projects full-year FY2024 performance to reach ¥750 billion in sales and ¥30 billion in operating profit.

The game development segment saw sales rise 10.1% YoY to ¥45.0 billion, with operating losses narrowing by 32.9% YoY to ¥3.4 billion, largely driven by the success of the new title 'Jujutsu Kaisen Phantom Parade.'

Market Analysis

Advertising

Mobile

+2

CyberAgent

Report

37 pages

FY2024 Presentation Material: January to March 2024

CyberAgent achieved consolidated Q2 FY2024 sales of ¥215.1 billion (up 10.0% YoY) and an operating profit of ¥21.0 billion, marking the first time profit has exceeded ¥20 billion in eight quarters.

The Game segment grew 8.1% YoY to ¥67.1 billion in sales, bolstered by the launch of 'Granblue Fantasy: Relink'—which reached one million units sold in eleven days—and various anniversary events.

The Media segment (ABEMA) reached a record ¥42.0 billion in sales, a 25.8% YoY increase, and achieved profitability for the first time since Q2 2023 with an operating profit of ¥0.7 billion.

Market Analysis

In-Game Advertising

Streaming

+2

CyberAgent

Report

54 pages

FY2024 Presentation Material: October 2023 to September 2024

The company's fiscal year 2024 results cover the period from October 2023 through September 2024.

The fiscal year 2025 forecast covers the period from October 2024 through September 2025.

The report outlines performance and projections for the company's internet advertisement business.

Market Analysis

Advertising

Investment

+1

CyberAgent

Report

43 pages

2Q FY2025 Financial Presentation Material

The company identified inappropriate accounting practices occurring at a consolidated subsidiary.

Financial statements for past fiscal years have been amended to address these accounting irregularities.

Correction reports for past annual securities reports were formally submitted on May 15, 2025.

Market Analysis

Advertising

Investment

+2

CyberAgent

Report

37 pages

1Q FY2025 Presentation Material

CyberAgent reported a 5.6% YoY revenue increase to ¥203.8 billion and a 32.1% rise in operating profit to ¥8.3 billion for 1Q FY2025.

The Game segment underperformed, recording a 15.1% YoY revenue decline to ¥38.2 billion and a 4.1% drop in operating profit due to a slower release cadence.

Growth was primarily driven by the Media & IP segment, which saw a 10.5% sales increase to ¥55.6 billion, and the Internet Advertising segment, which grew 11.8% to ¥117.7 billion.

Market Analysis

Advertising

Investment

+1

CyberAgent

Previous

1

…

4

5

6

…

63

Next