Report

Omówienie Wyników Finansowych: Q2 2021

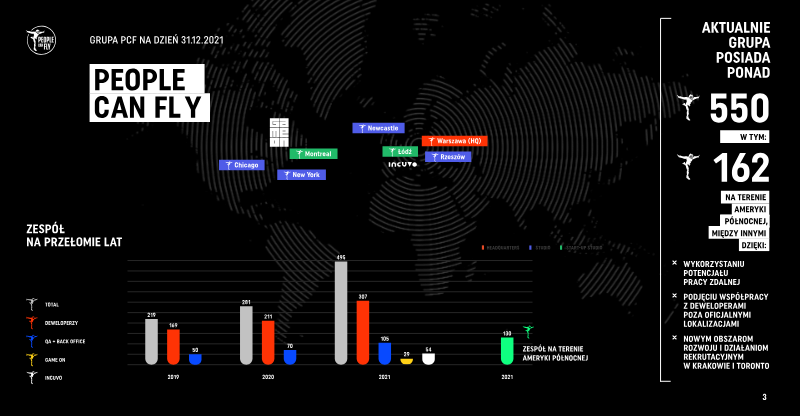

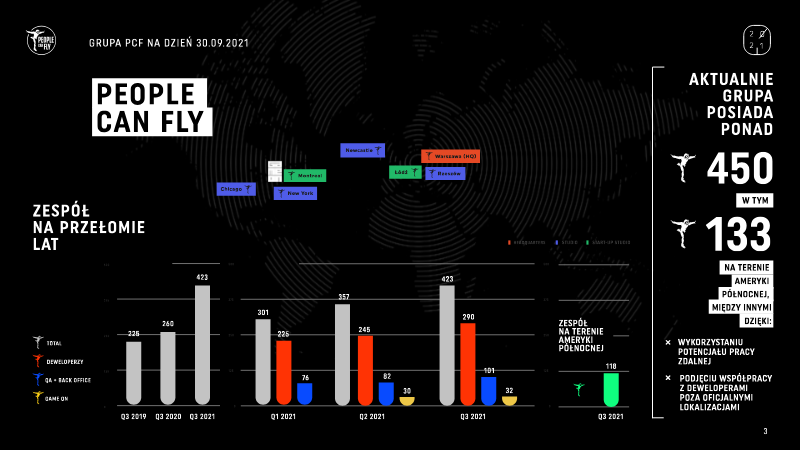

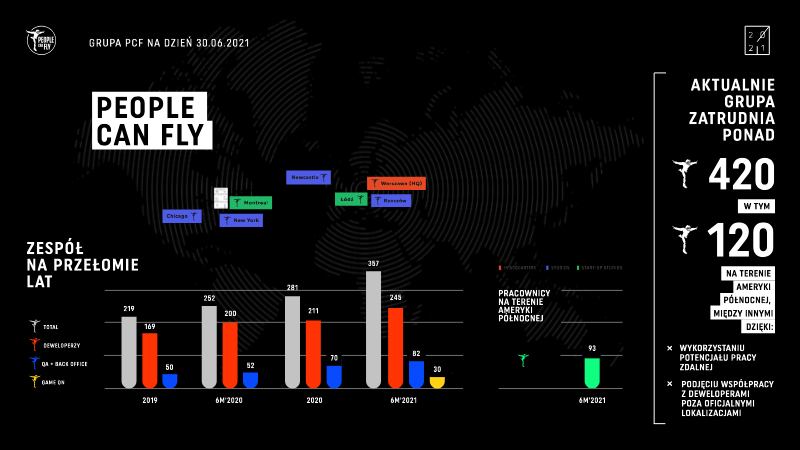

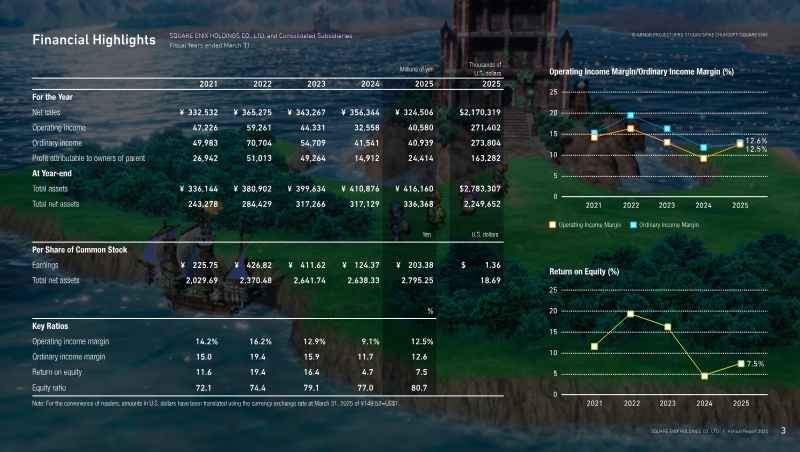

The presentation outlines PCF Group S.A.’s financial performance for the first half of 2021, emphasizing a significant growth trajectory across revenue, EBITDA, and workforce metrics. Total group revenues reached PLN 52.6 million in H1 2021, up 47 % from PLN 35.3 million in the same period of 2020, reflecting a compound annual growth rate of 34.4 % over 2017‑2020. EBITDA rose to PLN 28.8 million, a 36.5 % increase from PLN 21.1 million in H1 2020, and the adjusted EBITDA figure of PLN 27.6 million represents a 55.6 % jump from the prior year’s PLN 17.7 million, after accounting for IPO issuance costs and warrant amortisation. Personnel expansion is notable: the group’s headcount grew to 252 employees, a 41.7 % rise, with significant additions in North America and Europe, including new studios in Chicago, New York, and Montreal. The People Can Fly division contributed PLN 21.1 million in revenue, while the Can Fly studio reported an EBITDA of PLN 28.8 million, underscoring its profitability. Strategic initiatives highlighted include a partnership with Square Enix, confirming no royalty obligations for the Outriders title and progressing an investment agreement involving warrants. The group’s portfolio strategy aims to secure a leading position in new IP development, targeting annual releases of self‑published or publisher‑partnered titles by 2024. Financial statements show a robust asset base of PLN 95.7 million, with equity at PLN 190.1 million and liabilities of PLN 272.8 million, yielding an equity‑to‑asset ratio of 185 %. Cash reserves increased to PLN 150.3 million, supporting ongoing development and expansion plans.

PCF Group

Report

2025 Annual Report

Purpose C O N T E N T S Creating New Worlds With Boundless Imagination 03 Financial Highlights Creating New Worlds With Boundless Imagination 03 Financial Highlights 04 A Message to Our Stakeholders to Enhance People’s Lives.

Square Enix