Skip to main content

Game Industry

Library

Library

Search

Ask AI

News

Connect your AI

Browse

The Catch Up

Topics

Collections

Writers

Help

Subscribe

Game Industry

Library

Library

Search

Ask AI

Saved

Library

789 reports matching your filters

All Types

Reports

Articles

Presentations

Whitepapers

Financial

Legal

Other

Search

Global

Market Analysis

Mobile

Monetization

Marketing

User Acquisition

PC

Game Publishing

Investment

Game Development

Player Behavior

Console

Advertising

Steam

Game Design

AI

Mergers & Acquisitions

Streaming

Clear

Filters

1

Global

Recently added

Newest first

Oldest first

Title A–Z

Title Z–A

Report

4 pages

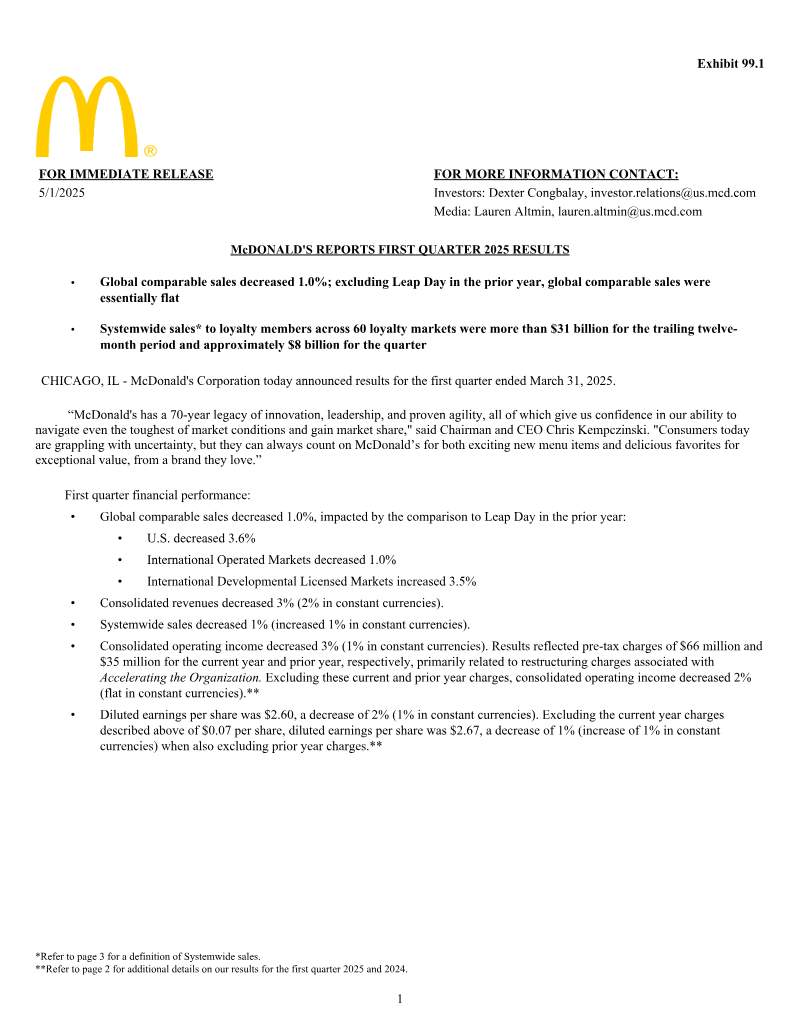

McDonald's Reports First Quarter 2025 Results

McDonald’s global comparable sales declined by 1.0% in Q1 2025, with consolidated revenues falling 3% year-over-year to $5.96 billion.

Diluted earnings per share dropped 2% to $2.60, though non-GAAP figures suggest underlying performance remained more stable when excluding restructuring charges.

The U.S. market faced a 3.6% decrease in comparable sales, primarily attributed to a reduction in total guest counts.

Market Analysis

Monetization

Global

+1

McDonald's Corporation

Report

14 pages

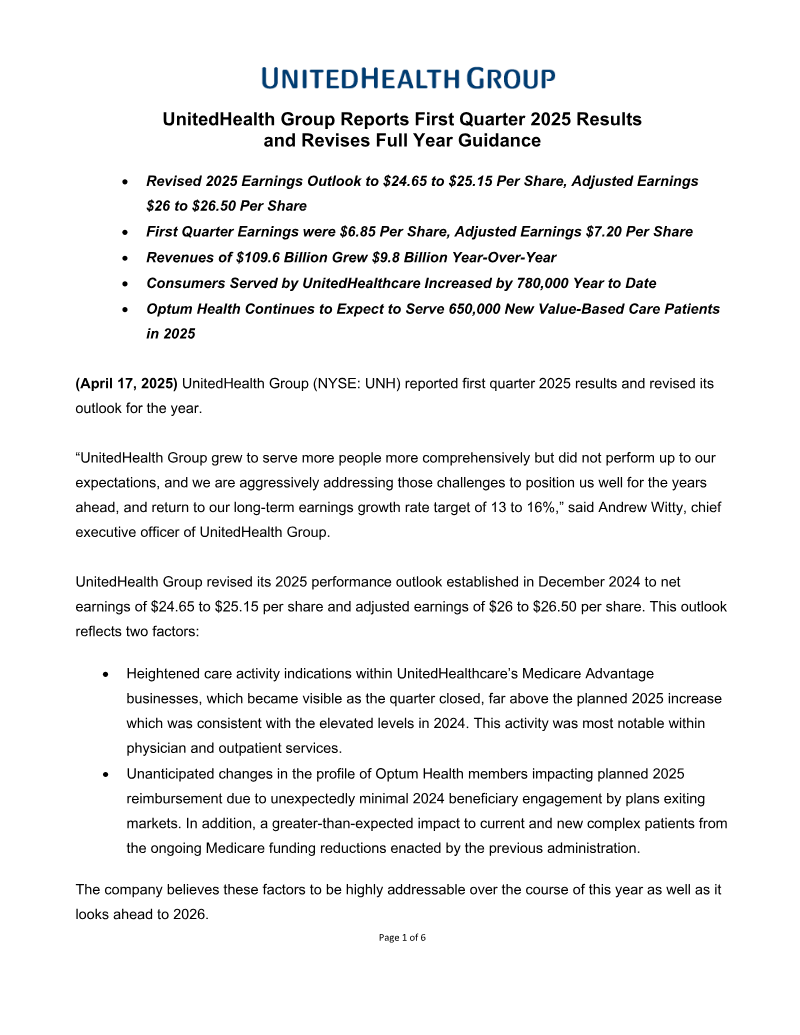

UnitedHealth Group: First Quarter 2025 Results and Revised Guidance

UnitedHealth Group has revised its 2025 full-year adjusted earnings outlook to a range of $24.65 to $25.15 per share.

First quarter 2025 revenues reached $109.6 billion, representing a year-over-year increase of $9.8 billion.

The company reported first quarter earnings of $6.85 per share, with adjusted earnings reaching $7.20 per share.

Market Analysis

Market Forecast

Investment

+2

UnitedHealth Group

Report

1 pages

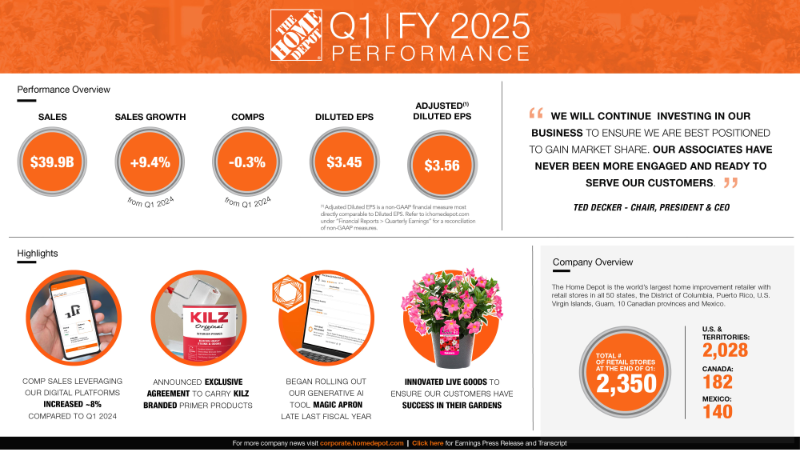

Performance Overview

The Home Depot generated $39.9 billion in total sales with a 9.4 percent increase in sales growth, despite a 0.3 percent contraction in comparable store sales.

The company reported a diluted earnings per share of $3.45, which increases to $3.56 on an adjusted basis.

Digital platforms achieved an 8 percent increase in comparable sales, supported by the deployment of generative AI tools like Magic Apron.

Market Analysis

Investment

USA

+1

The Home Depot

Report

23 pages

Ram HD 3500: FY 2025 Guidance

Stellantis has suspended its 2025 financial guidance due to heightened uncertainty surrounding evolving tariff policies and their potential impact on the competitive landscape.

Q1 2025 consolidated shipments fell 9% to 1.2 million units, while net revenues declined 14% to €35.8 billion, driven largely by production volume drops in North America.

North American net revenues plummeted 25% in Q1 2025, contrasting with South American performance, which saw a 6% revenue increase and a 23.8% market share.

Market Analysis

Market Forecast

Investment

+1

Stellantis

Report

1 pages

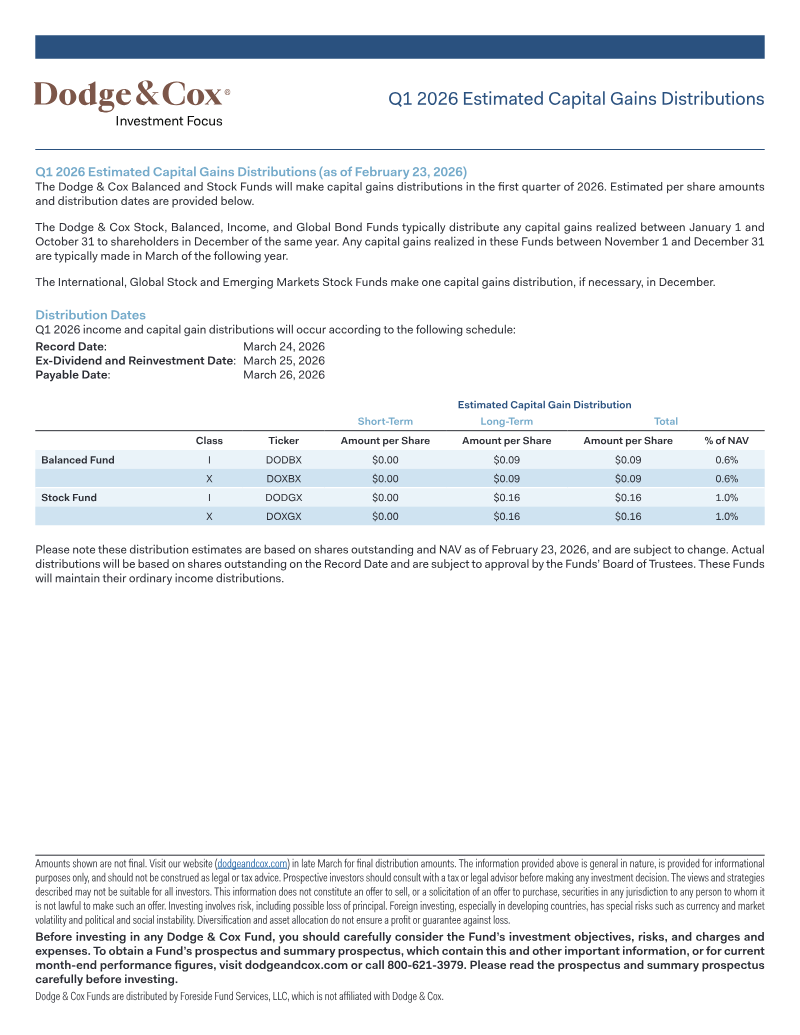

Q1 2026 Estimated Capital Gains Distributions

Dodge & Cox will issue Q1 2026 capital gains distributions on March 26, 2026, for the Balanced Fund and Stock Fund based on gains realized between November 1 and December 31, 2025.

The Balanced Fund (DODBX and DOXBX) estimates a distribution of $0.09 per share, equivalent to 0.6% of its net asset value.

The Stock Fund (DODGX and DOXGX) estimates a distribution of $0.16 per share, equivalent to 1.0% of its net asset value.

Investment

Market Analysis

Global

Dodge & Cox

Report

70 pages

Visibility Should Mean "Risk On"

Macro investing success requires analyzing the interplay between government fiscal spending and monetary policy, specifically regarding its impact on inflation and interest rates.

Investment strategies should account for the fact that macroeconomic shifts can occur with rapid and dramatic speed, necessitating preparation for a broad range of potential outcomes.

High-conviction investment opportunities are best identified by focusing on long-term, multi-decade extremes rather than short-term market fluctuations.

Market Analysis

Market Forecast

Investment

+1

VanEck

Report

111 pages

Q1 2026 Chartbook: A Guide to Interpreting the Economy & Markets

The Wealth Management Chief Investment Office provides a strategic framework for Q1 2026 focused on disciplined portfolio management and diversified asset allocation.

The report outlines a comprehensive outlook for 2026, identifying key economic themes and market trends to guide investment decision-making.

Macroeconomic analysis serves as a foundational component of the Q1 2026 guidance to help clients navigate shifting market conditions.

Market Analysis

Market Forecast

Investment

+1

Wealth Management Chief Investment Office

Report

2 pages

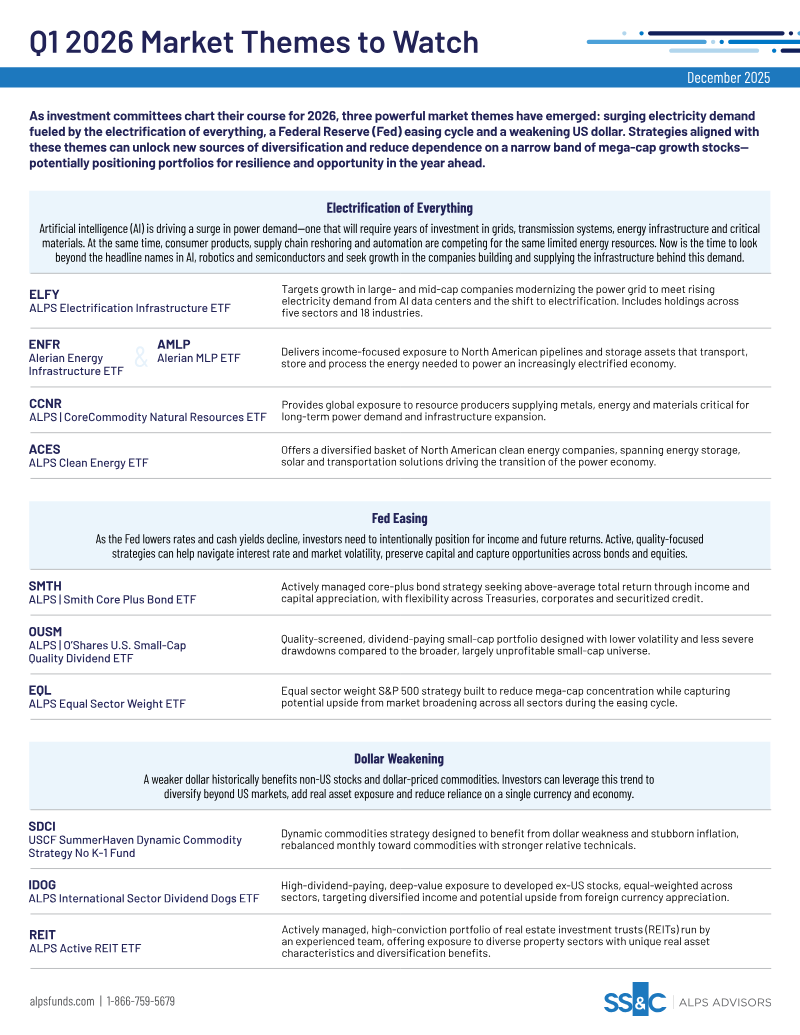

Q1 2026 Market Themes to Watch

Investors should pivot from mega-cap growth stocks toward infrastructure assets that support the electrification of the economy, including grid modernization, energy transmission, and critical material supply chains.

The surge in power demand driven by AI, data centers, and industrial automation necessitates capital allocation into North American energy pipelines, clean energy solutions, and global natural resource producers.

The Federal Reserve’s interest rate easing cycle requires a shift toward quality-oriented income strategies, such as active fixed-income management and dividend-paying small-cap equities, to replace declining cash yields.

Market Analysis

Market Forecast

Investment

+2

GameVault System

Report

17 pages

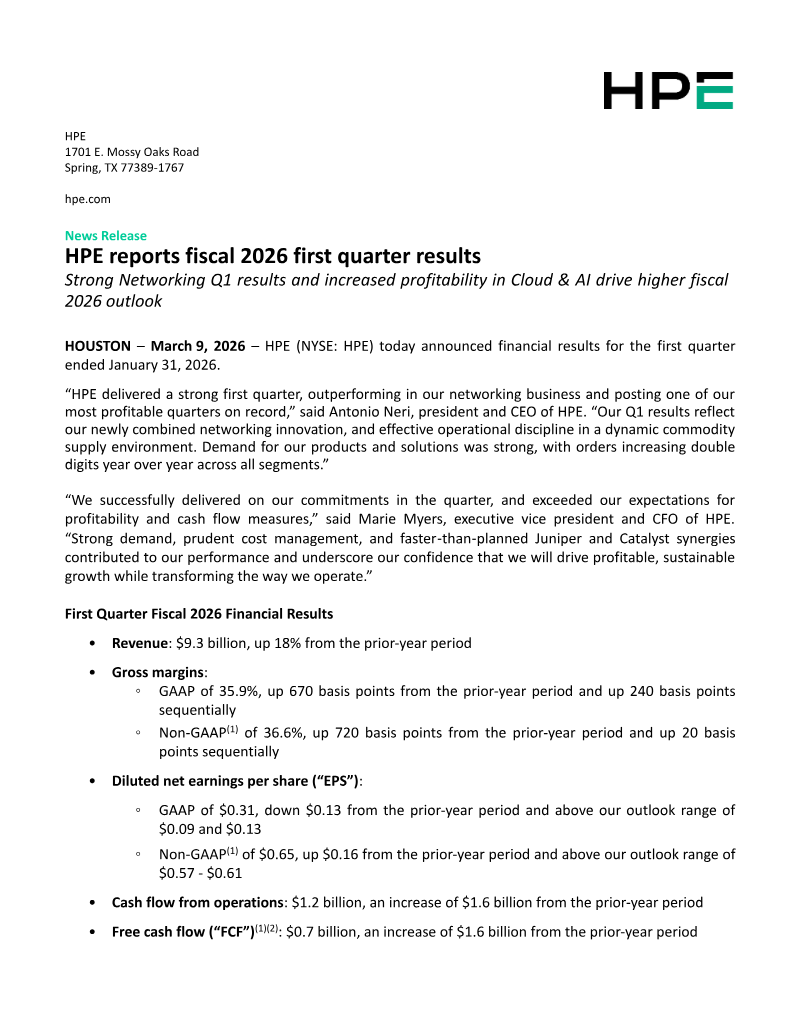

HPE Fiscal 2026 First Quarter Results

HPE reported strong financial results for the first quarter of fiscal 2026, ending March 9, 2026.

The company achieved one of its most profitable quarters on record during the first quarter of fiscal 2026.

Networking business performance exceeded expectations, serving as a primary driver for the quarter's strong results.

Market Analysis

AI

Investment

+1

Hewlett Packard Enterprise

Report

20 pages

Q1 2026 Trader Client Sentiment Report

Bullish sentiment among active traders declined by 5 percentage points in Q1 2026 compared to the end of 2025, though over 50% of respondents maintain a positive outlook.

Despite macroeconomic concerns, 47% of traders identify as risk-seeking, and 83% express a high likelihood of buying into market dips over the next three months.

Information Technology saw the most significant decline in sector sentiment, while Energy, Utilities, and Materials remain the most favored sectors for investors.

Market Analysis

Market Forecast

Investment

+1

Charles Schwab

Report

20 pages

Quarterly Outlook: Q1 2026

Q1 2026 is characterized by a significant divergence between ongoing geopolitical volatility and a period of relative stability in global rulemaking.

Companies are currently prioritizing the monitoring of geopolitical developments to assess their potential operational and strategic implications.

Market Analysis

Investment

Global

+1

KPMG

Report

1 pages

Harmonogram publikacji raportów okresowych: GreenX

GreenX Metals Limited has scheduled its 2026 fiscal year financial reporting across the London, Australian, and Warsaw stock exchanges.

The company will release quarterly reports on October 31, 2025, January 30, 2026, April 30, 2026, and July 31, 2026.

The half-year report for the period ending December 31, 2025, is set for publication on March 12, 2026.

Investment

Funding

Global

GreenX Metals Limited

Report

162 pages

Corporate Responsibility Report 2020: Germany

Deutsche Telekom published its 2020 Corporate Responsibility Report for Germany, detailing accountability metrics and management strategies.

The report organizes sustainability and operational data into four core thematic pillars: Green future, Digital life, New ways of working, and Good stewardship.

The document serves as a comprehensive record of the company's accountability standards and management practices for the 2020 fiscal year.

Global

Germany

Investment

+1

Deutsche Telekom

Report

93 pages

Responsibility Report 2020: Partners for Greater Purpose

Ecolab prioritized the global response to the Covid-19 pandemic as a central operational focus throughout 2020.

The company maintains a structured environmental management framework that specifically targets energy consumption and emissions reduction.

Water stewardship and conservation represent a core pillar of the organization's sustainability strategy.

Diversity & Inclusion

Global

Employment

Ecolab

Report

98 pages

Corporate Responsibility Report 2020

RELX operates as a global provider of information-based analytics and decision tools for professional and business markets.

In 2020, the company supported World Alzheimer's Day by promoting Elsevier content aimed at challenging the stigma and fear surrounding dementia.

The organization aligns its corporate responsibility initiatives with specific United Nations Sustainable Development Goals, including Zero Hunger, Good Health and Well-being, and Quality Education.

Diversity & Inclusion

Global

Marketing

RELX

Report

86 pages

2020 Report on Corporate Responsibility

The 2020 corporate responsibility report adheres to the Global Reporting Initiative (GRI) Core Standards.

Environmental impact disclosures are prepared in alignment with the Greenhouse Gas Protocol (GHG Protocol).

The company provides reporting indices specifically for the Task Force on Climate-related Financial Disclosures (TCFD).

Global

Employment

Diversity & Inclusion

Baker Hughes

Report

47 pages

IBM 2020 Corporate Responsibility Report

The year 2020 served as a catalyst for organizational and individual adaptation in response to global challenges.

The report emphasizes that periods of crisis drive human ingenuity and the reinvention of existing operational models.

Societal challenges faced during 2020 acted as a primary driver for testing the resolve and adaptability of global organizations.

AI

Diversity & Inclusion

Employment

+1

IBM

Report

64 pages

Corporate Responsibility Report: 2024 Fiscal Year

The 2024 Fiscal Year Corporate Responsibility Report outlines Metro's strategic framework across business fundamentals, products, services, and employee engagement.

The report establishes a materiality assessment to prioritize key corporate responsibility issues impacting the company's operations.

Leadership perspectives from the President and CEO, alongside the Vice President of Public Affairs and Communications, define the company's governance and public-facing priorities.

Diversity & Inclusion

Global

4A Games

Report

79 pages

2020 Corporate Responsibility Report

Keurig Dr Pepper (KDP) published its 2020 Corporate Responsibility Report, outlining the company's strategic approach to social and environmental governance.

The report details the company's organizational structure and operational scope, covering its diverse portfolio of beverage brands.

A primary focus area for the company is the health and safety of its workforce, which serves as a foundational pillar of its corporate responsibility strategy.

Diversity & Inclusion

Employment

Global

+1

Keurig Dr Pepper

Report

99 pages

Corporate Responsibility Report 2020: Driving Fashion Forward for Good

PVH Corp. established the 'Forward Fashion' strategy as the core framework for its 2020 corporate responsibility initiatives.

The report outlines the operational and sustainability commitments for PVH's primary brands, specifically highlighting Calvin Klein and Tommy Hilfiger.

The document serves as a formal 2020 disclosure regarding the company's environmental, social, and governance (ESG) performance.

Diversity & Inclusion

Employment

Global

PVH

Previous

1

…

11

12

13

…

40

Next