Report

Casual Games Report H1 2025

The casual mobile gaming landscape in the first half of 2025 exhibits a high degree of market concentration, with three specific genres—Puzzle, Simulation, and Lifestyle—accounting for 80% of total industry revenue. This dominance underscores a significant narrowing of consumer spending patterns, where established mechanics and high-engagement loops drive the vast majority of monetization. While the broader casual market continues to see a high volume of new releases, financial success is increasingly gated behind these top-performing categories, leaving a fragmented 20% of the market to be contested by all other sub-genres. Geographically, the data reflects a global trend toward consolidated spending, though Tier-1 markets in North America and Western Europe remain the primary engines for this revenue density. The findings suggest that the barrier to entry for sustainable profitability has risen, as the top three genres benefit from sophisticated live-ops strategies and aggressive user acquisition scaling that smaller genres struggle to replicate. This concentration indicates that developers are prioritizing proven monetization frameworks over experimental gameplay, leading to a more predictable but highly competitive environment for stakeholders. Methodological analysis of app store performance and consumer spending metrics during the six-month period reveals that the Puzzle genre remains the undisputed leader in value generation. The growth in Simulation and Lifestyle categories further points to a shift in player demographics toward audiences seeking long-term progression and social expression. Ultimately, the H1 2025 data confirms that the casual gaming sector is no longer a broad field of equal opportunity, but rather a top-heavy ecosystem where strategic alignment with the dominant trio of genres is essential for achieving significant commercial scale.

AppMagicJan 2025

Report

Games Industry in 2025

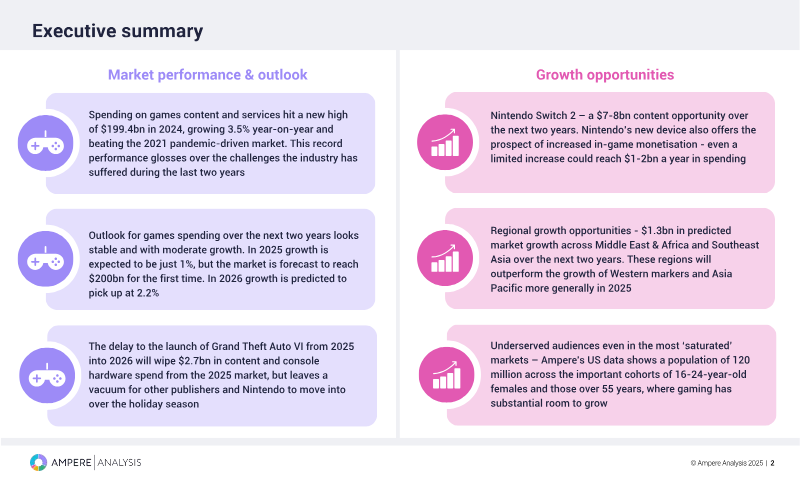

The global games content and services market reached a record $199.4 billion in 2024, a 3.5% year-on-year increase that surpassed pandemic-era peaks. Despite this financial milestone, the industry faces significant structural challenges, including widespread layoffs, studio closures, and a shift toward de-risking strategies. Growth is expected to slow to 0.9% in 2025, largely due to the delay of Grand Theft Auto VI into 2026, which is projected to remove $2.7 billion from the 2025 console market. However, the industry is forecast to surpass the $200 billion threshold for the first time in 2025, with growth accelerating to 2.2% in 2026. Key growth opportunities center on new hardware and emerging markets. The anticipated launch of the Nintendo Switch 2 in 2025 represents a $7-8 billion content opportunity, with significant potential for increased in-game monetization. Geographically, the Middle East, Africa, and Southeast Asia are expected to outperform Western markets, with the Middle East and Africa projected to grow by 6.3% in 2025. Additionally, significant headroom exists in mature markets like the U.S. by targeting underserved cohorts, specifically females aged 16-24 and adults over 55. The industry is navigating a transition in monetization and platform dynamics. In-game spending accounts for 77% of total revenue, while physical media is expected to dwindle to just 2% of the market by 2026. To combat escalating AAA development costs, publishers are increasingly utilizing remakes, remasters, and transmedia franchise strategies. While mobile gaming remains the largest segment at 58% market share, PC gaming showed the strongest growth in 2024 at 5.7%. The analysis utilizes proprietary market modeling, financial KPIs, and quantitative consumer research across global regions to provide a comprehensive outlook through 2026.

Ampere AnalysisJan 2025