Skip to main content

Game Industry

Library

Library

Search

Ask AI

News

Connect your AI

Browse

The Catch Up

Topics

Collections

Writers

Help

Subscribe

Game Industry

Library

Library

Search

Ask AI

Saved

Library

1,254 reports matching your filters

All Types

Reports

Articles

Presentations

Whitepapers

Financial

Legal

Other

Search

Market Analysis

Global

Mobile

Monetization

Investment

PC

Game Publishing

Marketing

Player Behavior

Console

Steam

Game Development

User Acquisition

Player Demographics

Employment

Europe

Mergers & Acquisitions

Japan

Clear

Filters

1

Market Analysis

Recently added

Newest first

Oldest first

Title A–Z

Title Z–A

Report

15 pages

Association Canadienne du Logiciel de Divertissement Rapport Annuel 2024

The Canadian video game sector contributed $5.5 billion to the national GDP in 2024, supported by a resilient, virtual-first operational model.

The industry successfully secured exemptions from the Streaming Act levy and the Online Harms Act, signaling significant growth in its regulatory and political influence.

Major global publishers including Epic Games, Roblox, and Tencent joined the association, driving revenue beyond forecasts and expanding the sector's reach.

Market Analysis

Diversity & Inclusion

North America

ESAC – Entertainment Software Association of Canada

Jan 2024

Report

12 pages

Inside Gaming: It's Personal! 2024

46% of gamers now prioritize creation and imagination as their primary motivation for playing, representing a 10% year-over-year increase.

Games that facilitate self-expression through customization, open worlds, and constant updates—such as Roblox, Fortnite, and The Sims—achieve 60% higher engagement than industry norms.

72% of consumers report they would view brands more favorably if those companies helped them translate their gaming-inspired self-expression into real-world products, skills, or lifestyle alignments.

Market Analysis

Player Behavior

Marketing

+1

Fandom

Jan 2024

Report

12 pages

Inside Gaming: It's Personal!

Nearly two-thirds of gamers report feeling more authentic while playing than in their daily lives, a sentiment that has driven a 30% increase in time spent gaming among those who view these platforms as spaces for self-presentation.

In-game character customization is the primary driver of self-expression for 76% of players, significantly outpacing other features like usernames (48%) and communication tools or emotes (30–35%).

Fandom’s 2024 data indicates a psychological disconnect where gamers maintain distinct online personas that they perceive as separate from their real-life identities.

Market Analysis

Player Behavior

Diversity & Inclusion

+2

Fandom

Jan 2024

Report

55 pages

Xsolla Report: State of Play – Winter 2024 Edition

The global gaming industry is projected to grow from $106.8 billion in 2023 to $205.7 billion by 2026, supported by a total player base of 3.79 billion people.

Mobile gaming remains the industry's primary revenue driver, accounting for nearly 50% of total consumer spending and reaching a projected $111.4 billion in 2024.

Strategic investment value saw a massive 577% surge in mid-2023 to reach $7 billion in a single quarter, despite an overall cooling in M&A activity and a volatile investment climate.

Market Analysis

Diversity & Inclusion

Player Demographics

+1

Xsolla

Jan 2024

Report

54 pages

Save Point 2024: Recapping the Year's Biggest Trends in Live Streaming

The live streaming industry shifted toward a creator-led, multi-platform model in 2024, characterized by widespread simulcasting and the rise of alternative platforms like Kick following Twitch’s withdrawal from the Korean market.

Co-streaming has become a dominant force in competitive gaming, now accounting for nearly 45 percent of total esports viewership.

Large-scale, non-gaming spectacles like La Velada del Año 4 demonstrated that independent creators can now command millions of concurrent viewers, rivaling traditional broadcast media.

Market Analysis

Streaming

Esports

+1

Stream Hatchet

Jan 2024

Report

27 pages

Global Sports Tech Report 2024

The provided source text contains no factual data, metrics, or findings from the Global Sports Tech Report 2024.

The content consists solely of a request for additional information rather than report substance.

No specific growth rates, company names, or dates are available to summarize.

Market Analysis

Mergers & Acquisitions

Investment

+1

Drake Star Partners

Jan 2024

Report

24 pages

From Volatility to Stability: Q3 2024 Gaming Deals Report

The gaming industry has transitioned to a normalized market environment, with Q3 2024 private investment totaling approximately $1 billion across 120 rounds.

AA and indie publishers are outperforming the broader market, driving a 35% year-over-year growth in gross revenue while AAA titles remain stagnant.

Investor capital is shifting away from traditional content toward infrastructure, payment systems, and development tools.

Market Analysis

Mergers & Acquisitions

Investment

+3

InvestGame

Jan 2024

Report

7 pages

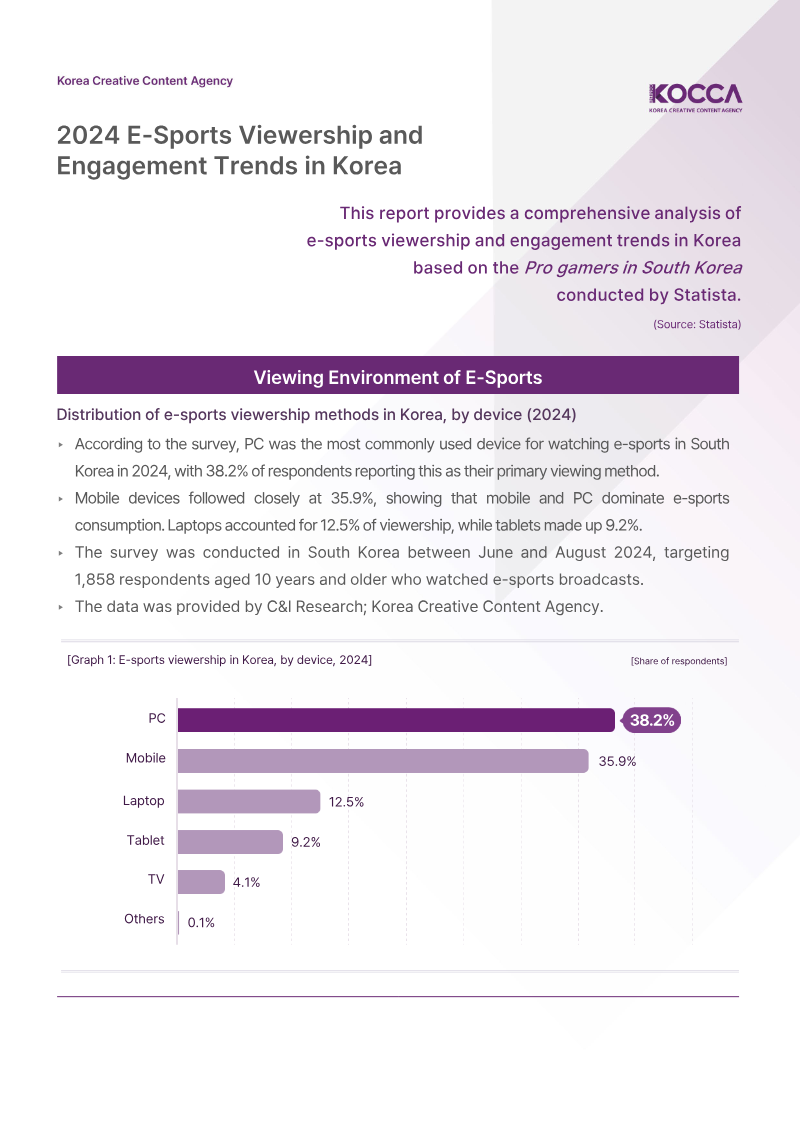

2024 E‑Sports Viewership and Engagement Trends in Korea

YouTube dominates the South Korean e-sports market with a 78.5% platform share, significantly outpacing competitors SOOP (14.1%) and CHZZK (7.2%).

E-sports consumption is primarily mobile and desktop-driven, with PCs (38.2%) and mobile phones (35.9%) accounting for 74.1% of all viewing devices.

Engagement is frequent and consistent, as 58.9% of viewers watch e-sports content at least once a week, with 20.4% watching 3–4 times weekly.

Market Analysis

Player Demographics

Esports

+1

KOCCA – Korea Creative Content Agency

Jan 2024

Report

276 pages

India's Media & Entertainment Sector: March 2024

India's media and entertainment sector is projected to reach INR 3.1 trillion ($37 billion) by 2026, growing at a 10% CAGR as online platforms overtake traditional television as the primary revenue driver.

Mobile-first consumption is the primary growth engine, supported by 904 million broadband subscriptions and 574 million smartphone users who spend over four hours daily on mobile media.

Gaming is a dominant market force, with Free Fire and BGMI accounting for 25% of in-app purchase revenue and esports viewership reaching 78% of the gaming population.

Market Analysis

India

Streaming

EY

Jan 2024

Report

19 pages

Top 500 Titles on Twitch 2023

The top 500 Twitch titles generated nearly 15 billion hours of watch time in 2023, with 50% of that total concentrated in just 11 games.

Grand Theft Auto V was the most-watched title of 2023, accumulating 1.3 billion hours of viewership.

Fortnite led the industry in creator engagement with 2.8 million unique channels, more than double the count of its nearest competitor.

Streaming

Market Analysis

Global

Lurkit

Jan 2024

Report

32 pages

Midcore Gaming Apps Report 2023

Midcore games now account for 35% of total US iOS gaming revenue, driven by a player migration from hyper-casual titles toward deeper, more complex gameplay.

Android is significantly more cost-effective for developers than iOS, with a $0.73 CPI compared to $3.86 and nearly double the Day-7 ROAS at 6.1%.

The EMEA region offers the best market value, balancing a low $0.80 CPI with a competitive 4.4% ROAS, while North America remains the most expensive market at a $5.45 CPI.

Market Analysis

Global

Mobile

+1

Liftoff

Jan 2024

Report

27 pages

Games Market Trends to Watch in 2024

The global games market is in a period of stabilization and recovery throughout 2024, supported by the growing install base of current-generation consoles like the PlayStation 5 and Xbox Series X|S.

Developers are increasingly pivoting back to premium, finite gaming experiences to counter the oversaturation of the live-service market.

Mobile developers are expanding to PC platforms to mitigate the impact of rising user acquisition costs and stricter privacy regulations.

Market Analysis

Market Forecast

Player Demographics

+1

Newzoo

Jan 2024

Report

72 pages

Serbian Gaming Industry Report 2023

The Serbian gaming industry generated €175 million in revenue in 2023, marking a 17% year-on-year increase.

The sector's workforce nearly doubled to approximately 4,300 professionals, supported by talent inflows from Russia, Ukraine, and Belarus.

The ecosystem now includes 38 active studios producing 81 titles, with a strategic shift occurring from mobile-first games toward core and original-IP projects.

Market Analysis

Monetization

Investment

+1

SGA

Jan 2024

Report

6 pages

The Alumni Effect: A Deep Dive into Studios Founded by Ex-Rioters

Startups founded by former Riot Games employees have raised nearly $500 million across 27 companies since 2020.

Ex-Riot founders command a 53% premium in average round size, securing $11 million per round compared to the $7 million industry average.

Venture capital firms Andreessen Horowitz and Bitkraft Ventures are the primary backers, participating in deals worth $339.3 million and $236.3 million respectively.

Investment

Funding

Market Analysis

+1

InvestGame

Jan 2024

Report

4 pages

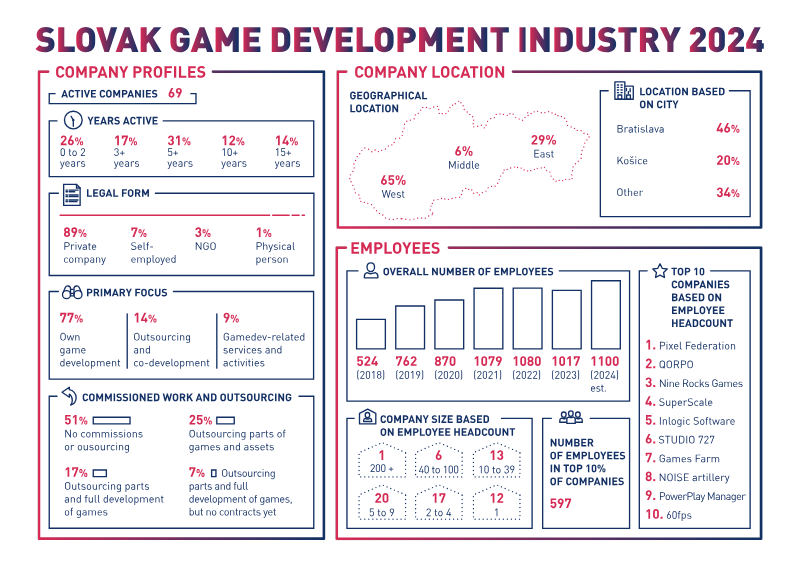

Company Profiles: Slovakia 2024

The Slovak game industry is highly concentrated, with the top 10% of companies—including Pixel Federation and Nine Rocks Games—generating 83.5% of the sector's 70 million EUR annual turnover.

The industry consists of 69 active companies, 77% of which focus on original game development rather than outsourcing services.

After a slight contraction in 2023, the workforce is projected to reach approximately 1,100 employees by the end of 2024, with a median age of 31 and 21% female representation.

Market Analysis

Employment

Game Development

+1

Swiss Game Developers Association

Jan 2024

Report

52 pages

Global Games Market Report

The global games market is projected to reach $184.0 billion in 2023, with a forecast to grow to $205.4 billion by 2026 supported by a 3.31 billion-person player base.

Mobile gaming remains the largest revenue segment at $89.7 billion, though it is currently experiencing a 1.4% decline due to privacy-related challenges in user acquisition and monetization.

PC and console gaming are the primary industry growth engines for 2023, driven by improved hardware supply and a strong pipeline of high-profile software releases.

Market Analysis

Monetization

Player Demographics

+1

Newzoo

Jan 2024

Report

72 pages

Africa Games Industry Report 2024

The Sub-Saharan gamer base grew from 77 million in 2015 to 186 million in 2021, with mobile gaming driving 95% of the player base and nearly 90% of the region's $778.6 million revenue in 2022.

Free-to-play with in-app purchases is the dominant revenue model, with approximately one-third of players currently making in-app purchases.

Infrastructure remains the primary barrier to growth, with 71% of developers citing unreliable power and 57% citing high internet costs as significant impediments.

Market Analysis

Player Demographics

Game Development

Maliyo Games

Jan 2024

Report

15 pages

Interactive Entertainment 2025: Global Market Sizing & Forecast

The global interactive entertainment market is projected to reach $250.2 billion in consumer spending by 2025, marking a 4.6% year-over-year growth.

Mobile gaming remains the industry's largest segment, with forecasted consumer spending of $115.7 billion in 2025.

Console hardware is experiencing a significant cyclical downturn, with spending expected to decline by 31% in 2024 ahead of next-generation device launches.

Market Forecast

Market Analysis

Global

+3

Aldora

Jan 2024

Report

47 pages

Study Report on African Video Games: Premier Results in Francophone Countries

Awareness of locally developed games is extremely low, with over 82% of gamers in Senegal, Côte d’Ivoire, and Cameroon reporting they have never heard of an African-produced title.

Financial infrastructure is a major barrier to monetization, as approximately 51% of surveyed gamers lack a bank card to facilitate in-game purchases.

The market is dominated by a young, mobile-first demographic, with 45% of players aged 19–25 and over 80% utilizing Android devices.

Market Analysis

Player Demographics

Market Forecast

+1

The Game Hub Senegal

Jan 2024

Report

36 pages

Localization in the MENA Region

The MENA gaming market is a high-growth frontier projected to reach $3.24 billion in player spending and 38.9 million gamers by 2028.

There is a significant supply gap in the region, as only 3.5% of Steam titles are currently localized despite 41% of regional gamers prioritizing localized content.

Deep culturalization can drive exponential growth, with some titles increasing their MENA-based revenue and daily active users from 3% to 80% of their global total.

Market Analysis

Player Demographics

Esports

+1

Saudi Esports Federation

Jan 2024

Previous

1

…

35

36

37

…

63

Next