Skip to main content

Game Industry

Library

Library

Search

Ask AI

News

Connect your AI

Browse

The Catch Up

Topics

Collections

Writers

Help

Subscribe

Game Industry

Library

Library

Search

Ask AI

Saved

Library

1,254 reports matching your filters

All Types

Reports

Articles

Presentations

Whitepapers

Financial

Legal

Other

Search

Market Analysis

Global

Mobile

Monetization

Investment

PC

Game Publishing

Marketing

Player Behavior

Console

Steam

Game Development

User Acquisition

Player Demographics

Employment

Europe

Mergers & Acquisitions

Japan

Clear

Filters

1

Market Analysis

Recently added

Newest first

Oldest first

Title A–Z

Title Z–A

Report

46 pages

Digital Market Index: Q2 2025

In Q2 2025, non-gaming applications surpassed mobile games for the first time, accounting for 52% of the record $40 billion in total in-app purchase revenue.

Global mobile gaming downloads contracted by 6.8% year-over-year, while Strategy titles replaced RPGs as the highest-grossing gaming category with a 23% increase.

ChatGPT became the fastest application to reach one billion downloads and secured a top-five position in global revenue, signaling a major shift toward AI-driven utility.

Market Analysis

Global

Mobile

+1

Sensor Tower

Aug 2025

Report

104 pages

Annual Report 2025

Games Workshop achieved record financial results for 2024/25 with £617.5 million in revenue and £262.8 million in profit before taxation, leading to its promotion to the FTSE 100.

Licensing operating profit nearly doubled to £49.5 million, largely driven by the commercial success of the Space Marine 2 video game.

Core sales grew by 14.2%, fueled by strong performance in the trade channel and North American markets.

Game Publishing

Investment

UK

+1

Games Workshop Group

Aug 2025

Presentation

37 pages

Consolidated Financial Results Briefing Materials: FY3/26 Q1

Akatsuki Inc. reported a 44% year-over-year decline in consolidated sales to ¥2,313 million and an operating loss of ¥1,698 million for Q1 FY3/26.

The core Games business revenue contracted by 52% due to title withdrawals, a reactionary decline from the previous quarter, and high development costs for the upcoming 'Kaiju No. 8 The Game'.

IP Solutions revenue grew 168% to ¥298 million, driven by the consolidation of CRAYON, Inc. and the expansion of the Slash Gift online lottery service.

Market Analysis

Mergers & Acquisitions

Investment

+1

Akatsuki

Aug 2025

Report

133 pages

Vorhaus Digital Strategy Study: All Findings 2025

Digital-first entertainment has become the US standard, with smart TV penetration at 63% and connected devices officially surpassing traditional broadcast media.

Gaming is now a near-universal activity with 80% of the population participating, driven by daily mobile play and a significant rise in total annual in-game spending.

Consumers are adopting 'subscription cycling' to manage costs, despite the average household maintaining 3.5 video services and younger consumers (18–34) increasing annual digital media spending by $235.

Market Analysis

Player Behavior

Mobile

+1

Vorhaus Advisors

Aug 2025

Report

31 pages

Les Français et le jeu vidéo: 2025

The French video game market has reached 40.2 million players, representing 66% of the national population with an average player age of 40.

Social and multiplayer gaming are primary engagement drivers, with 86% of players using multiplayer modes and 60% reporting the formation of direct friendships through gaming.

Gender parity is a defining characteristic of the market, with women now comprising a 55% majority of players in the 16–30 age demographic.

Market Analysis

Player Demographics

France

+1

SELL – Syndicat des Éditeurs de Logiciels de Loisirs

Jul 2025

Report

20 pages

Games Industry Region Report China

The Chinese games market generated $48.7 billion in 2024, accounting for approximately 30% of total global industry revenue.

Chinese entities now dominate the global landscape, owning or developing 14 of the top 30 highest-grossing games worldwide as of early 2025.

The market supports a massive player base of over 701 million, with a significant shift occurring as domestic firms expand from mobile dominance into premium triple-A PC and console development.

Market Analysis

Monetization

China

PocketGamer.biz

Jul 2025

Report

34 pages

Llibre Blanc de la Indústria Catalana del Videojoc 2024

The provided report content contains no factual data, statistics, or industry insights regarding the Catalan video game industry, as it consists only of a meta-commentary requesting further information.

Market Analysis

Europe

Investment

+2

Direcció General d’Innovació i Cultura Digital

Jul 2025

Report

18 pages

The State of PC Game Distribution

Steam maintains a dominant market position, generating $10.8 billion in 2024 revenue with concurrent users increasing from 25.4 million in 2021 to 40.5 million by September 2025.

Developer reliance on Steam is extreme, with 88% of studios deriving over 75% of their revenue from the platform and 37% relying on it for more than 90%.

Despite 72% of developers labeling Steam a monopoly, diversification is underway, with 48% of studios utilizing the Epic Games Store and the Xbox PC store for distribution.

Market Analysis

Game Publishing

PC

+2

Rokky

Jun 2025

Report

16 pages

Mobile Game Feature Impact Spotlight

Strategic feature selection, rather than exhaustive feature adoption, is the primary driver of commercial success across the top 1,000 mobile games globally.

In the hybridcasual segment, implementing in-app purchase (IAP) bundles correlates with a $1.77 increase in lifetime revenue per download.

Casual puzzle leaders like Royal Match and Candy Crush Saga maintain market dominance with lower feature density, proving that core gameplay often outweighs the addition of luxury elements like cinematic cutscenes.

Market Analysis

Global

Mobile

+1

Sensor Tower

Jun 2025

Report

37 pages

Southeast Asia: Mobile Game Market Insights 2025

Southeast Asia is the world’s second-largest mobile gaming market by volume, recording 1.93 billion installs in early 2025, while ranking seventh globally in revenue at $625 million.

Indonesia is the region's primary volume driver with 870 million installs, whereas Thailand leads in monetization, generating $162 million in consumer spending.

Publishers based in Singapore and Vietnam have become a dominant global force, contributing over 5.8 billion installs to the international market through hypercasual and competitive titles.

Market Analysis

Mobile

Southeast Asia

+3

Sensor Tower

Jun 2025

Presentation

17 pages

Financial Results Q1 2025

PCF Group S.A. reported Q1 2025 revenue of 63.0 million PLN, an increase from 56.9 million PLN in Q1 2024.

The company recorded a net loss of 3.9 million PLN in Q1 2025, widening from a 0.9 million PLN loss in the same period last year.

Adjusted EBITDA fell significantly year-over-year, dropping from 11.0 million PLN to 1.7 million PLN.

Investment

Market Analysis

Europe

+1

PCF Group

Jun 2025

Report

1 pages

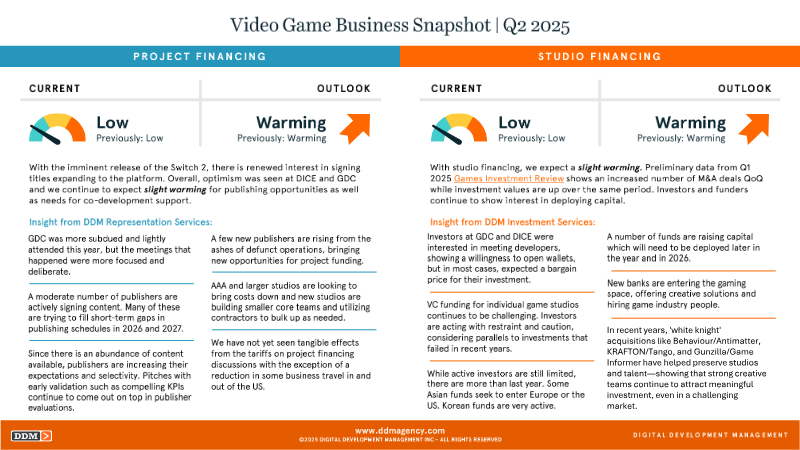

Video Game Business Snapshot: Q2 2025

Q2 2025 is defined by a surge in 'white knight' acquisitions, where major conglomerates are purchasing studios facing closure or downsizing to preserve creative talent and intellectual property.

Notable rescue acquisitions this quarter include KRAFTON’s purchase of Tango Gameworks, Behaviour Interactive’s absorption of Antimatter, and Gunzilla Games’ involvement with Game Informer.

The industry is shifting away from speculative growth toward strategic preservation, as large publishers prioritize securing proven development teams to stabilize long-term production pipelines.

Mergers & Acquisitions

Investment

Market Analysis

+1

DDM

Jun 2025

Report

28 pages

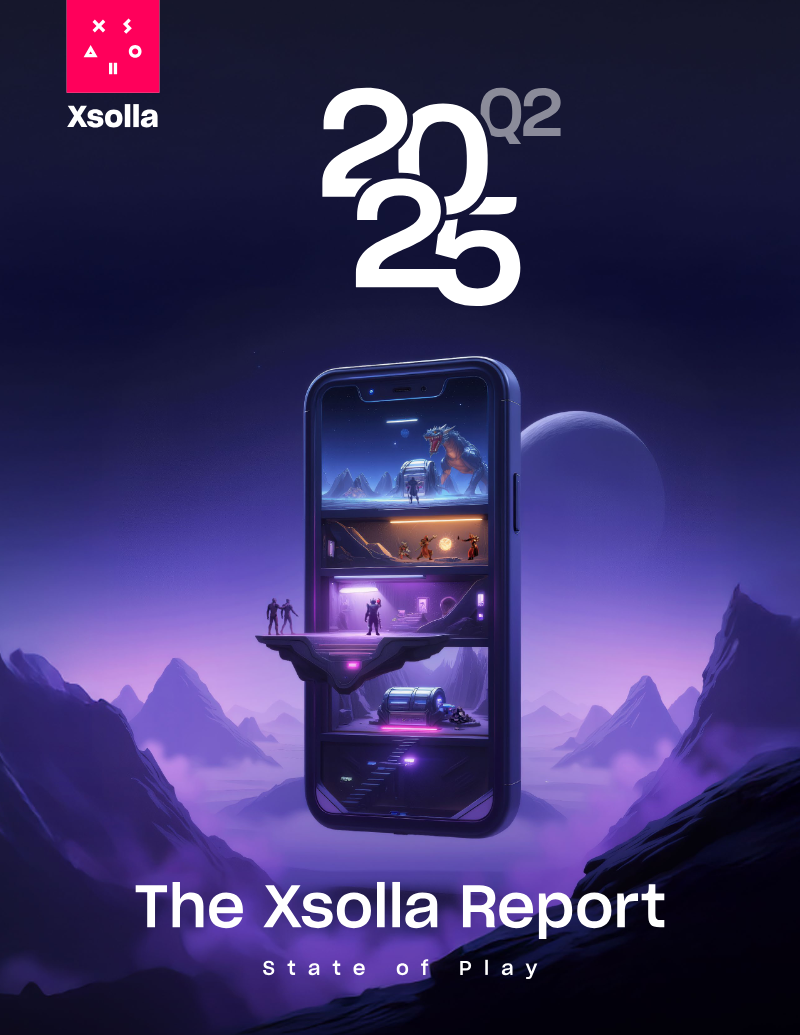

The Xsolla Report: State of Play Q2 2025

Mobile gaming is the industry's primary revenue driver, projected to reach $126 billion in 2025 with a total segment forecast of $150 billion.

Following the April 2025 Epic Games v. Apple court order, developers can now utilize direct-to-consumer web-shops to retain up to 95% of transaction value, with early adopters seeing millions in revenue recovery.

Hybrid monetization models—combining in-app purchases, advertising, and subscriptions—are used by 72% of developers and account for approximately 75% of total mobile revenue.

Market Analysis

Monetization

Market Forecast

+2

Xsolla

Jun 2025

Presentation

33 pages

FY2025.3 4Q Financial Results Presentation: Round One Corporation

Round One Corporation reported its financial results for the fiscal year ended March 2025, covering the period through the fourth quarter of FY2025.

The financial briefing took place on May 12, 2025, via a 60-minute webcast presentation.

The presentation session lasted 37 minutes, followed by a 23-minute Q&A segment.

Market Analysis

Investment

Arcade

+1

Round One Corporation

May 2025

Report

231 pages

The State of Video Gaming in 2026

The video game industry is in a period of contraction, with real-term spending on content declining by approximately 12% since 2021.

AAA production budgets have ballooned to between $200 million and $500 million, contributing to a capital-constrained environment marked by record-high layoffs and studio closures.

A small cohort of entrenched live-service titles now dominates the market, acting as 'black holes' that consume the majority of player time and spending, making new independent launches increasingly difficult.

Market Analysis

Global

Mobile

+2

Epyllion

May 2025

Report

67 pages

Studie Vlaams Gamebeleid: Eindrapport

The Flemish game industry lacks a 'missing middle' of mid-sized companies, with growth concentrated among a few major players despite an increase in total studio numbers between 2020 and 2024.

To compete in the $187.7 billion global market, Flemish policy must shift from project-based subsidies toward business scaling and private capital access for the 2026–2030 period.

Existing support mechanisms like the VAF/Gamefonds and the Tax Shelter are currently insufficient to match the aggressive fiscal incentives offered by international competitors such as Canada and France.

Market Analysis

Game Development

Funding

+1

Departement Cultuur

May 2025

Report

37 pages

2025 GDC Trends Report: Connecting the World Through Games

The mobile in-game advertising market reached $100 billion in 2024, officially surpassing revenue generated from in-app purchases.

Financial instability has forced 56% of studios to rely on personal funding as the publishing landscape becomes increasingly selective.

The industry is experiencing a 17% layoff rate, which has served as a primary catalyst for the formation of the United Videogame Workers union.

Market Analysis

AI

Monetization

+1

Game Developers Conference

May 2025

Presentation

46 pages

Consolidated Financial Results Briefing Materials: FY3/25

Akatsuki Inc. achieved a 46% year-over-year increase in consolidated operating profit to ¥3,915 million for FY3/25, despite a 1% decline in total sales.

The company maintains ¥33.3 billion in cash reserves to fund a ¥35 billion growth investment plan over the next three years, targeting M&A and next-generation game development.

Shareholder returns are increasing as the target Dividend on Equity (DOE) has been raised from 3% to 4% due to strong liquidity and a positive outlook.

Investment

Market Analysis

Japan

Akatsuki

May 2025

Report

2 pages

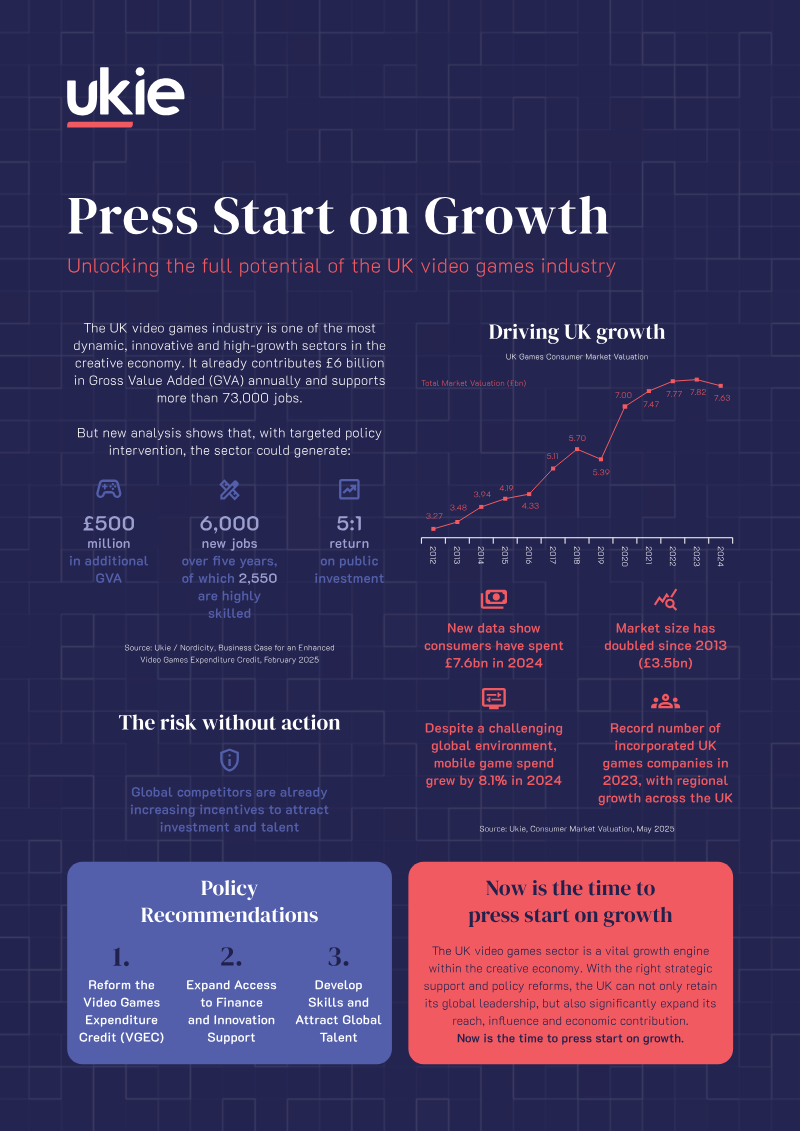

Press Start on Growth: Unlocking the Full Potential of the UK Video Games Industry

The UK video games industry currently contributes £6 billion in gross value added (GVA) and supports over 73,000 jobs, with the potential to add £5.7 billion in GVA and 5.4 million jobs over the next five years through strategic policy intervention.

Physical boxed software sales have collapsed, falling 34% year-on-year to represent only 4% of total market spend.

Esports experienced a significant surge of 44% year-on-year, driven by an increase in UK-based tournaments, contrasting with a 15% contraction in live-event spending.

Market Forecast

Market Analysis

Investment

+1

Ukie

May 2025

Presentation

19 pages

People Can Fly Q4 2024 Financial Results Presentation

People Can Fly is exiting the virtual reality market following the release of Project Bison in late 2025, citing the cessation of platform subsidies as the primary driver.

The company reported a net loss of PLN 175.3 million for fiscal year 2024, driven by significant one-off write-offs for Projects Red and Bifrost and the impairment of its Incuvo subsidiary.

Annual revenue grew to PLN 190.4 million in 2024, up from PLN 150.1 million in 2023, bolstered by work-for-hire contributions from Project Maverick and Project Echo.

Market Analysis

Investment

Game Publishing

+1

PCF Group

Apr 2025

Previous

1

…

22

23

24

…

63

Next