FinancialGames Workshop Group

Half-Yearly Report: 26 Weeks Ended 30 November 2025

1 Jan 202524 pages~71 min full read

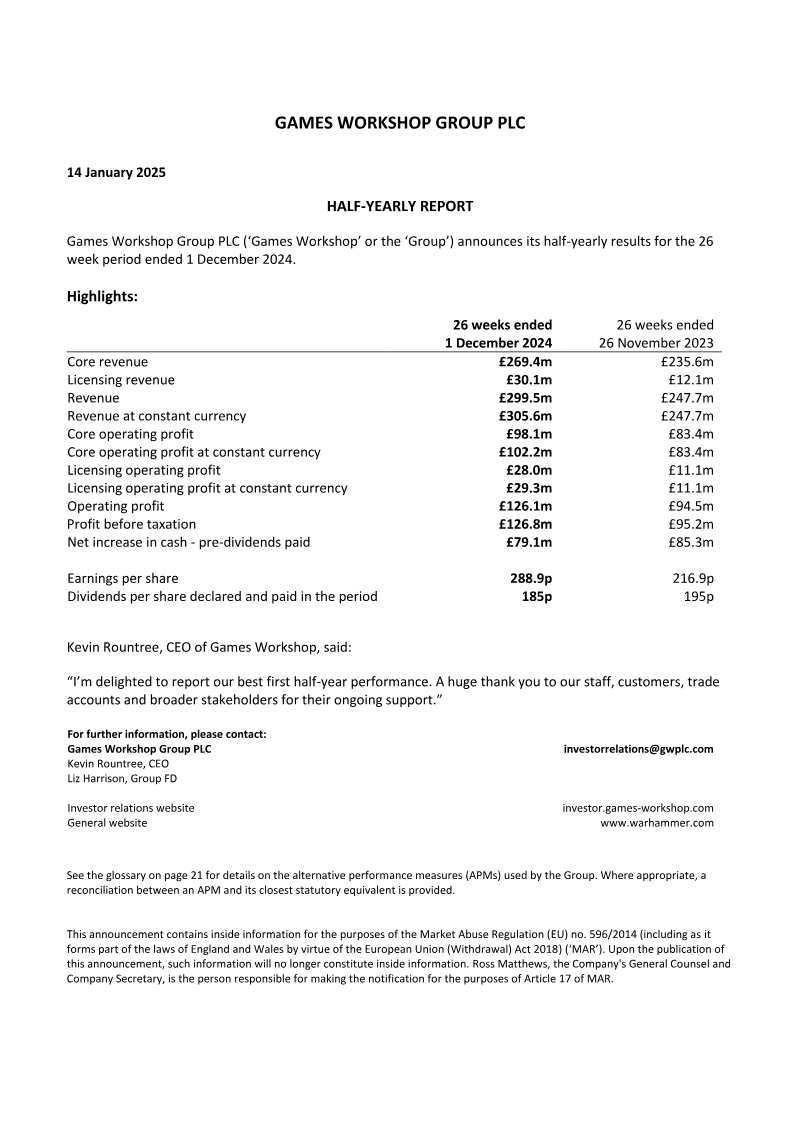

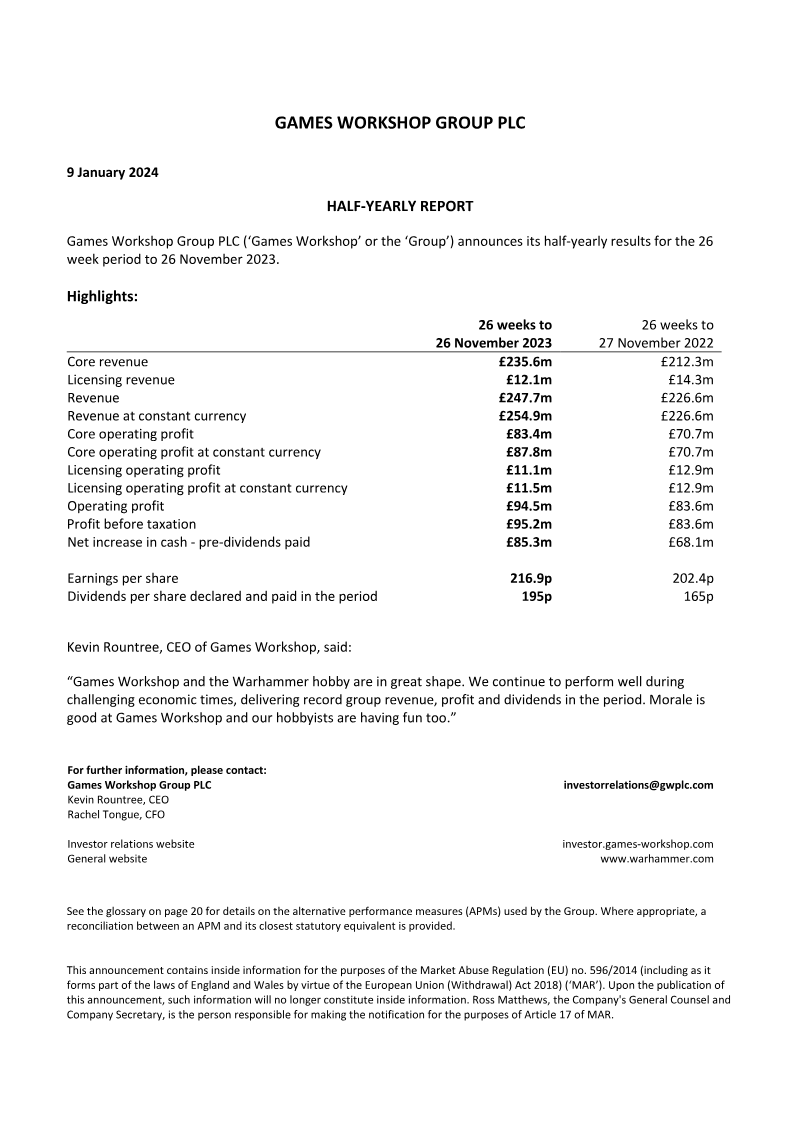

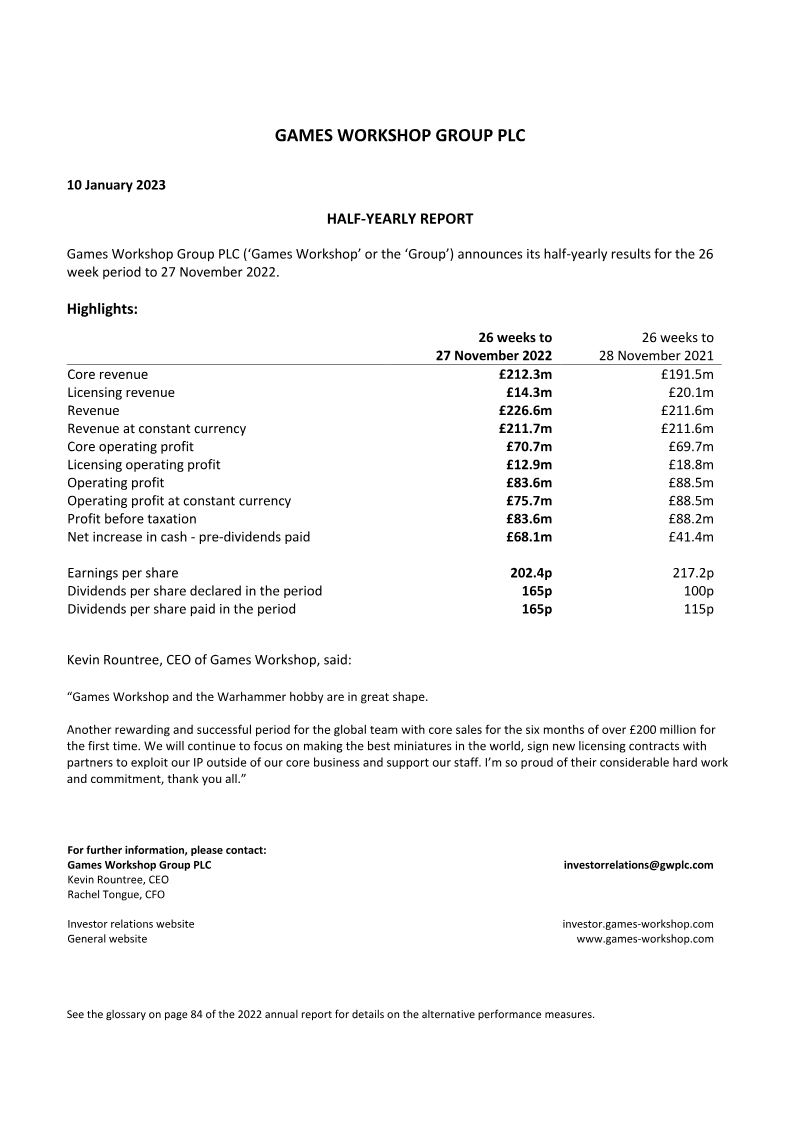

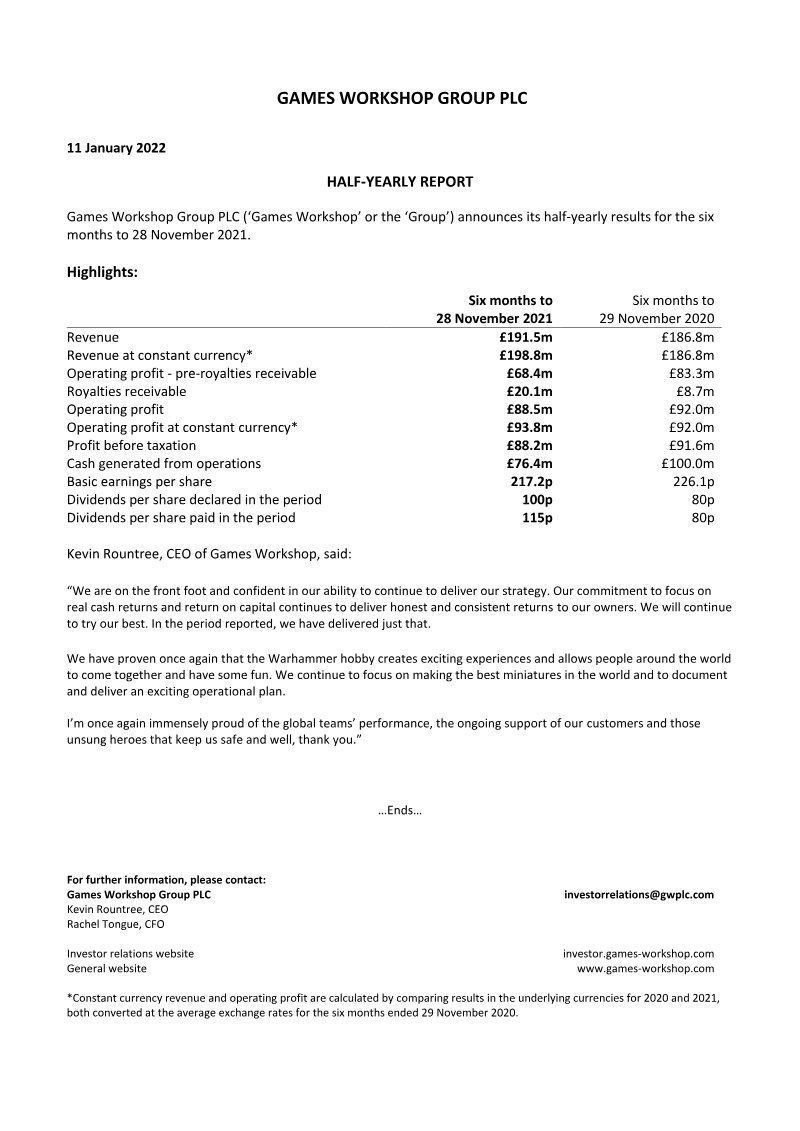

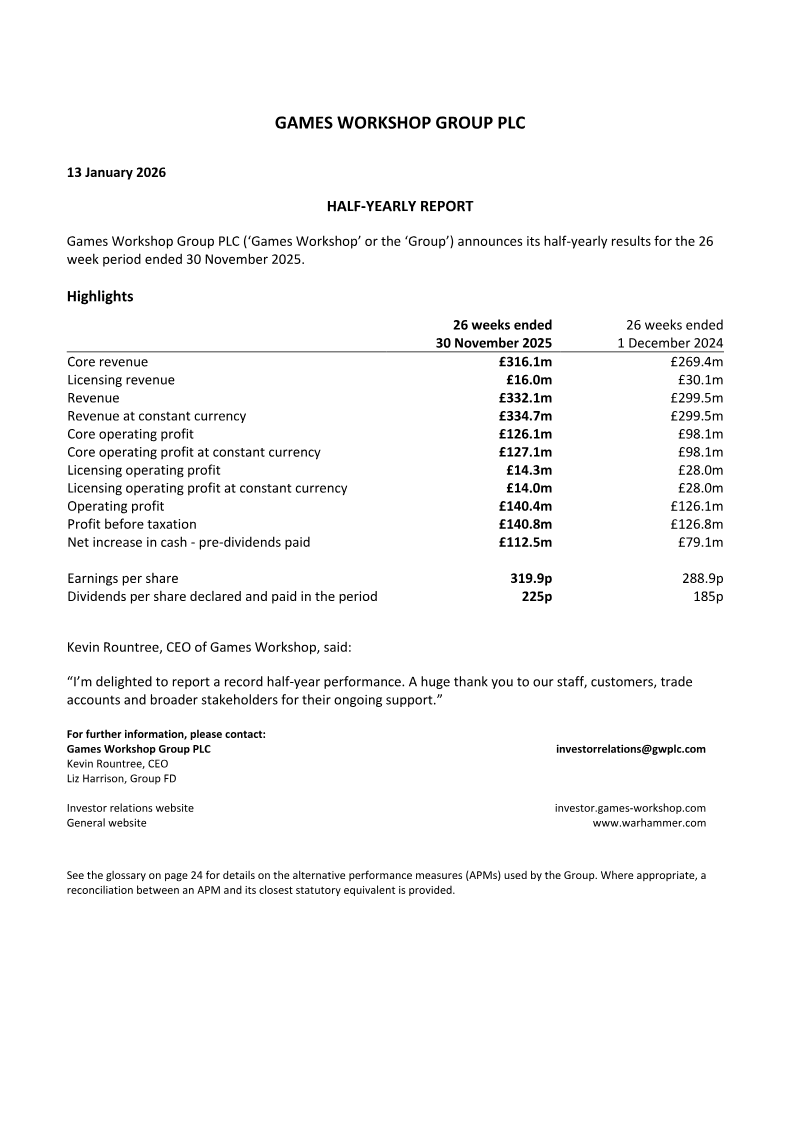

Games Workshop reported record financial performance for the 26 weeks ending November 30, 2025, with total revenue rising 10.9% to £332.1 million and profit before tax reaching £140.8 million.

Core business growth was driven by a 25.2% increase in trade channel revenue to £207.4 million, bolstered by successful product launches including the Space Wolves army box and updates to Horus Heresy and Age of Sigmar.

Licensing revenue fell by nearly half to £16.0 million compared to the previous year, primarily due to the absence of a major release comparable to the prior-year launch of Space Marine 2.

To offset £6.0 million in US tariff costs and protect a 69.4% gross margin, the company implemented a 3.5% price increase across its products.

The company is aggressively expanding infrastructure, with a fourth factory planned for 2026 and a robotic UK warehouse scheduled for 2027, supported by a strong cash position of £171.1 million.

Warhammer+ reached 248,000 subscribers, while the company maintains a strict policy against using artificial intelligence in creative processes to preserve brand integrity.

The group returned £74.2 million to shareholders in dividends while maintaining a global retail footprint of 575 stores and continuing progress toward 2032 carbon emission targets.

Games Workshop achieved record financial performance for the 26-week period ending November 30, 2025, characterized by robust core revenue growth and significant operational expansion. Total revenue rose to £332.1 million, a 10.9% increase over the previous year, while profit before tax climbed to £140.8 million. This growth was primarily fueled by the core business, particularly the trade channel, which saw a 25.2% increase to £207.4 million. High-profile product launches, including the record-breaking Space Wolves army box and new iterations for Horus Heresy and Age of Sigmar, underpinned this success.

While core operations flourished, licensing revenue experienced a contraction, falling from £30.1 million to £16.0 million. This decline is attributed to high prior-year comparatives following the major release of Space Marine 2, though long-term media prospects remain strong through ongoing development with Amazon MGM Studios. To protect margins against external pressures, such as £6.0 million in US tariff costs, the company implemented a 3.5% price increase and achieved a gross margin of 69.4%. Management also reaffirmed a strict policy against utilizing artificial intelligence in creative processes to preserve the brand's artistic integrity.

The company is aggressively investing in its global infrastructure to support future demand, with a fourth factory scheduled for 2026 and a robotic warehouse in the UK planned for 2027. Digital engagement continues to scale, with Warhammer+ reaching 248,000 subscribers and active digital users nearing 800,000. Supported by a strong cash position of £171.1 million and a global retail footprint of 575 stores, the Group remains a highly liquid going concern, returning £74.2 million to shareholders in dividends while maintaining progress toward its 2032 carbon emission targets.