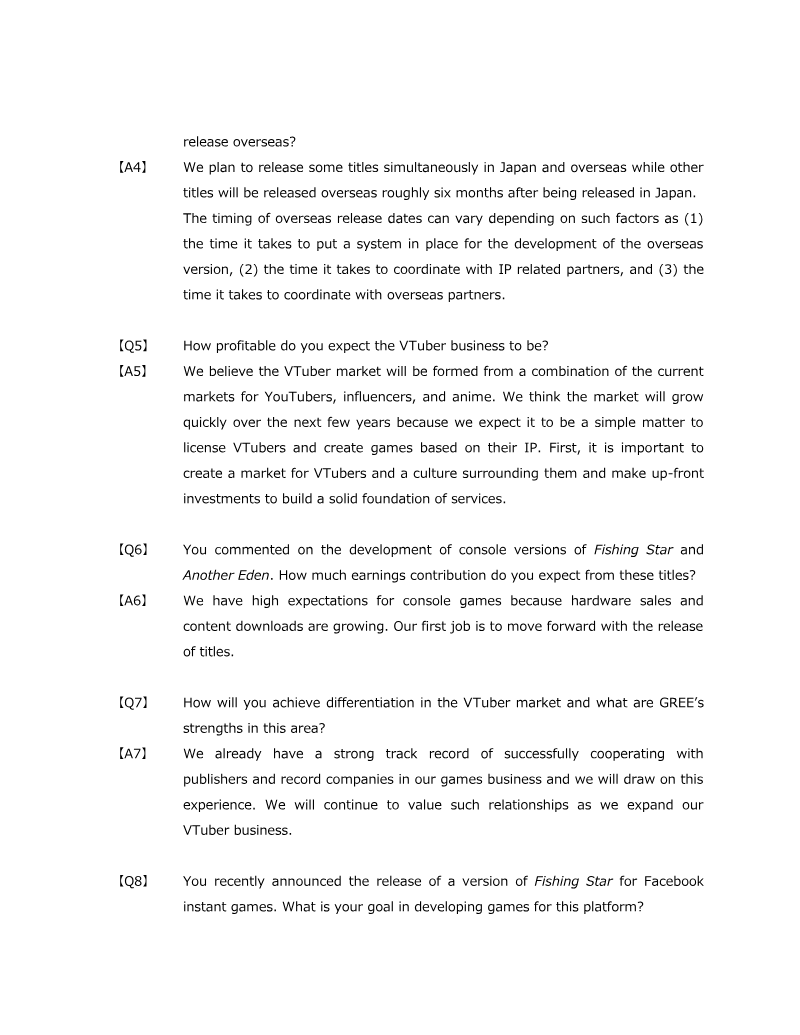

Market Analysis

Report

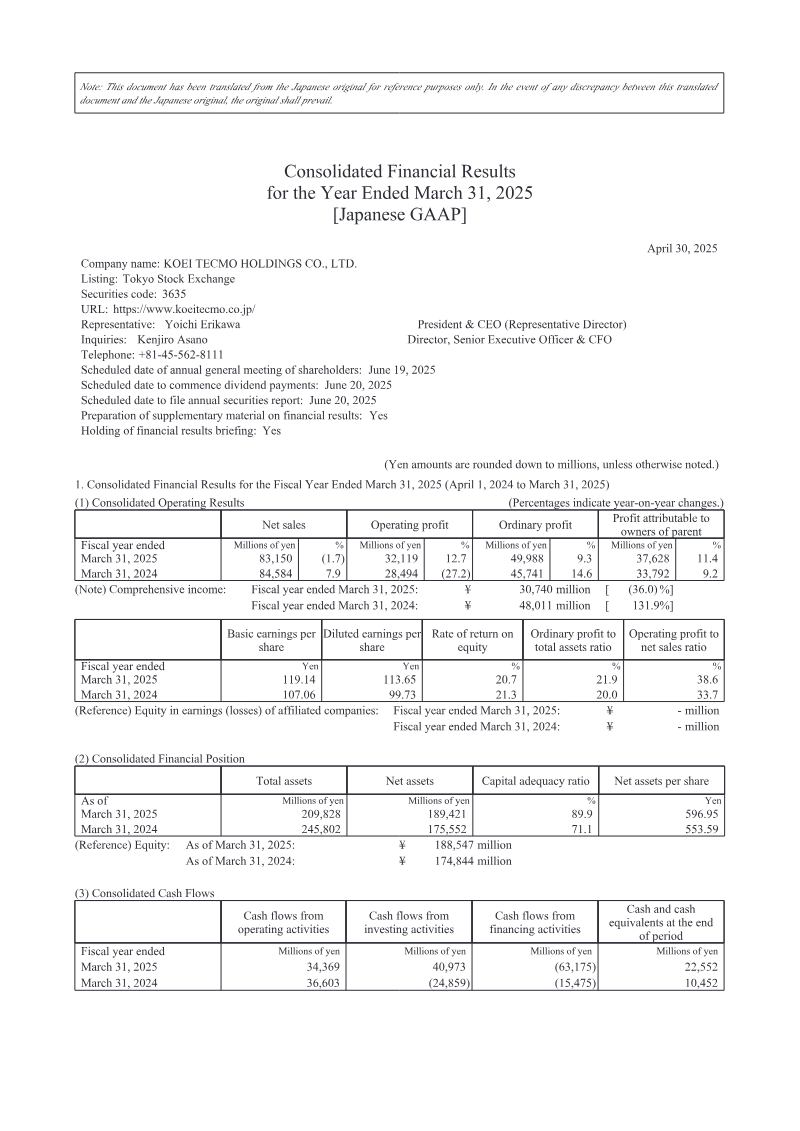

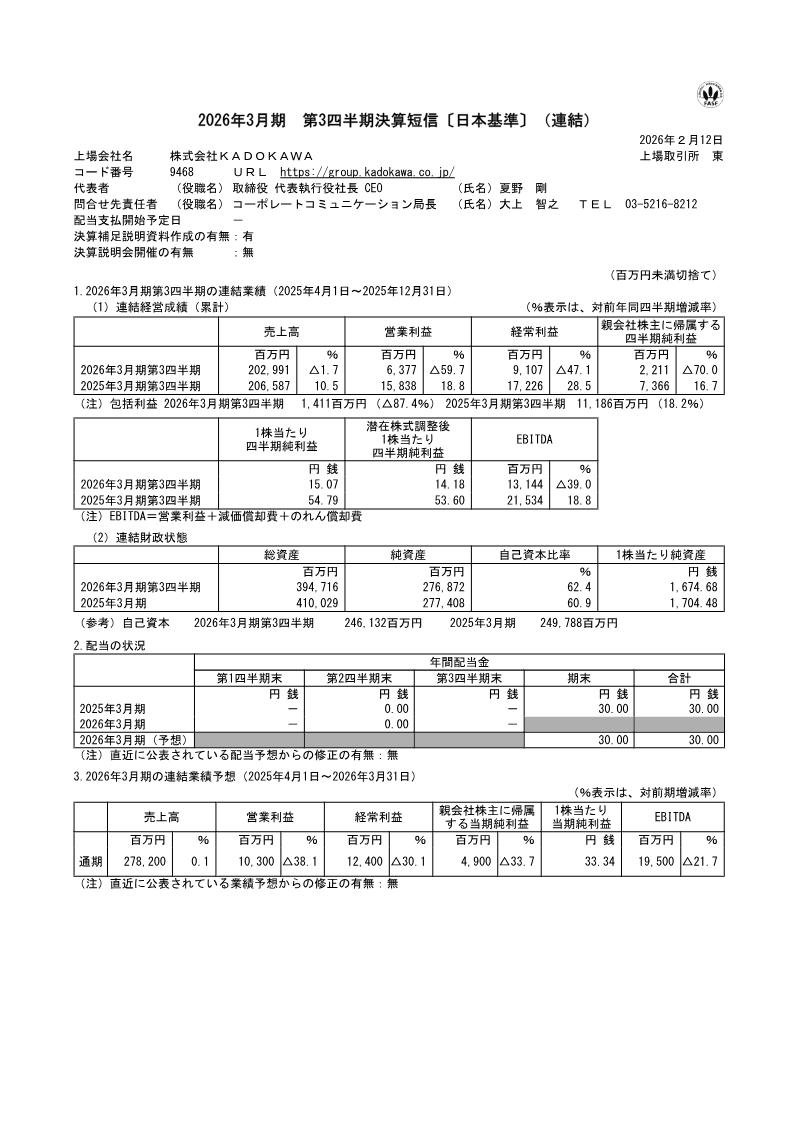

Consolidated Financial Results: Q3 Fiscal Year Ending March 2026

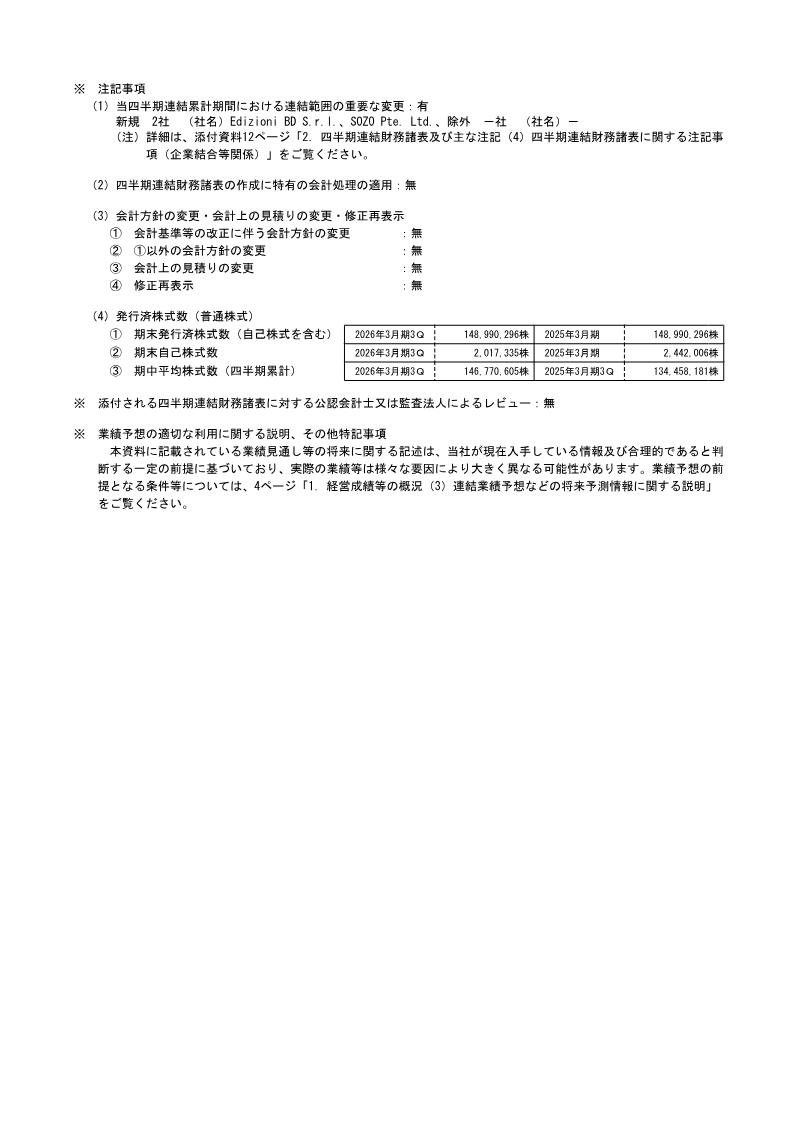

Kadokawa Corporation reported a decline in its third‑quarter consolidated results for the fiscal year ending March 2026. Total sales fell 1.7 % to ¥20,299 billion, while operating profit dropped 59.7 % to ¥637 million and ordinary profit fell 47.1 % to ¥910 million, leading to a parent‑shareholder net loss of ¥221 million. EBITDA contracted 39.0 % to ¥1,314 million, and the diluted earnings per share fell from ¥54.79 to ¥15.07. Net assets decreased modestly, with total assets at ¥394 billion and equity at ¥277 billion; the equity ratio remained healthy at 62.4 %. Cash and cash equivalents ended the quarter at ¥73 billion after significant outflows from investment activities (¥5.2 billion) and financing (¥5.0 billion). Segment performance varied: the publishing/IP creation unit posted a 90.2 % drop in operating profit to ¥623 million despite flat sales, whereas the web services segment achieved a 21.5 % revenue increase and an operating profit of ¥2187 million. The animation/film segment recorded a loss of ¥940 million, and the game unit saw an 11.6 % revenue decline with a modest operating profit of ¥8050 million. Education and other segments delivered modest gains. The company added two subsidiaries—Edizioni BD S.r.l. in Italy and SOZO Pte. Ltd. in Singapore—to its consolidation, increasing goodwill by ¥2,427 million and ¥1,846 million respectively. A significant system‑failure expense of ¥2,338 million related to a cyberattack on the Niconico service was recorded as a special loss. Dividend policy remained unchanged, with no dividends declared for the current year and a forecast of ¥30 million per quarter. The report covers Japan, the United States, Asia and other regions for the period April 1 2025 to March 31 2026, using Japanese GAAP and a survey of consolidated financial statements.

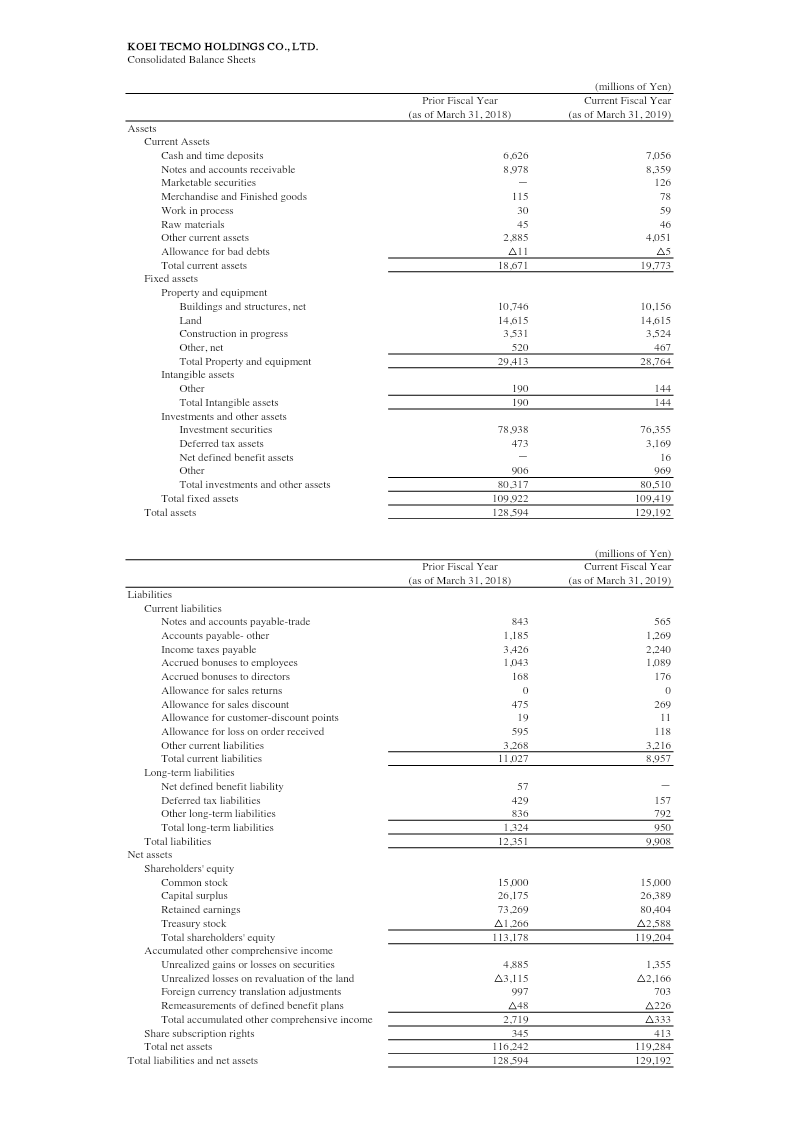

Kadokawa Corporation

Report

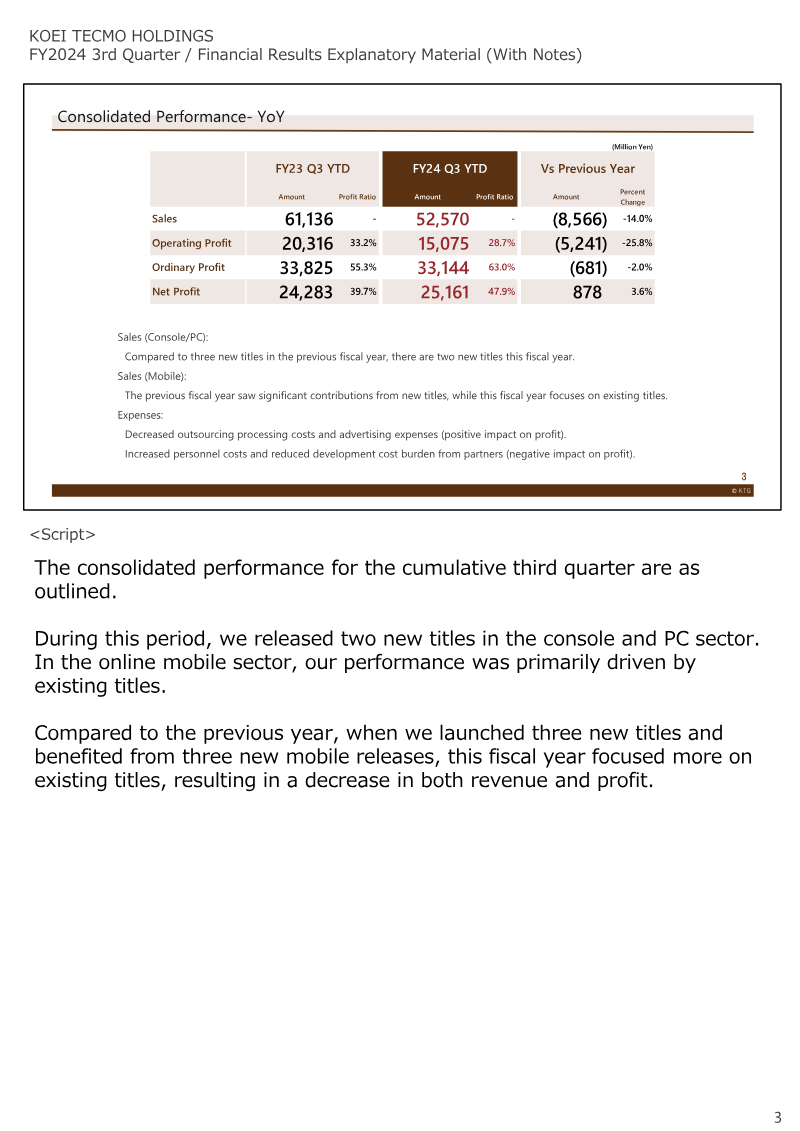

Financial Results for the Third Quarter: Fiscal Year Ending March 2024

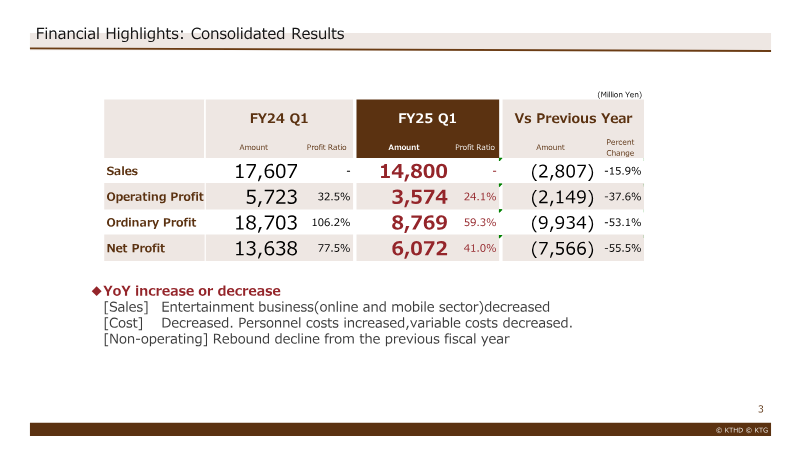

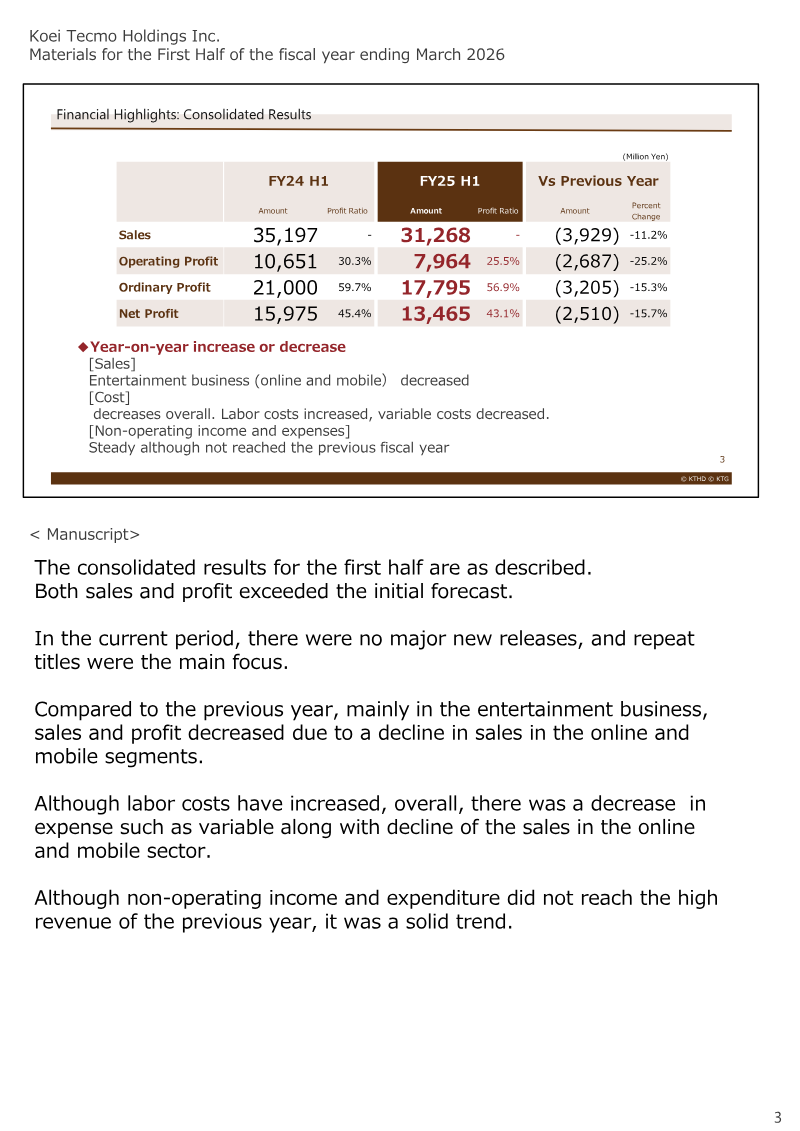

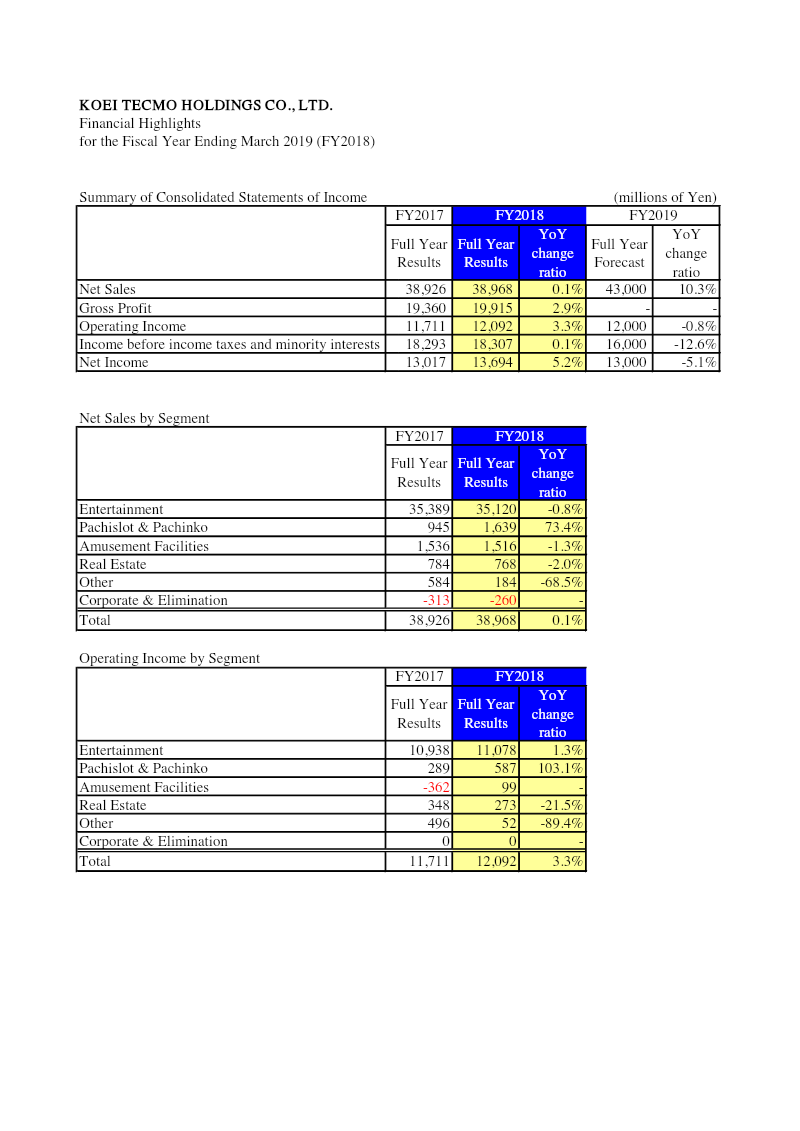

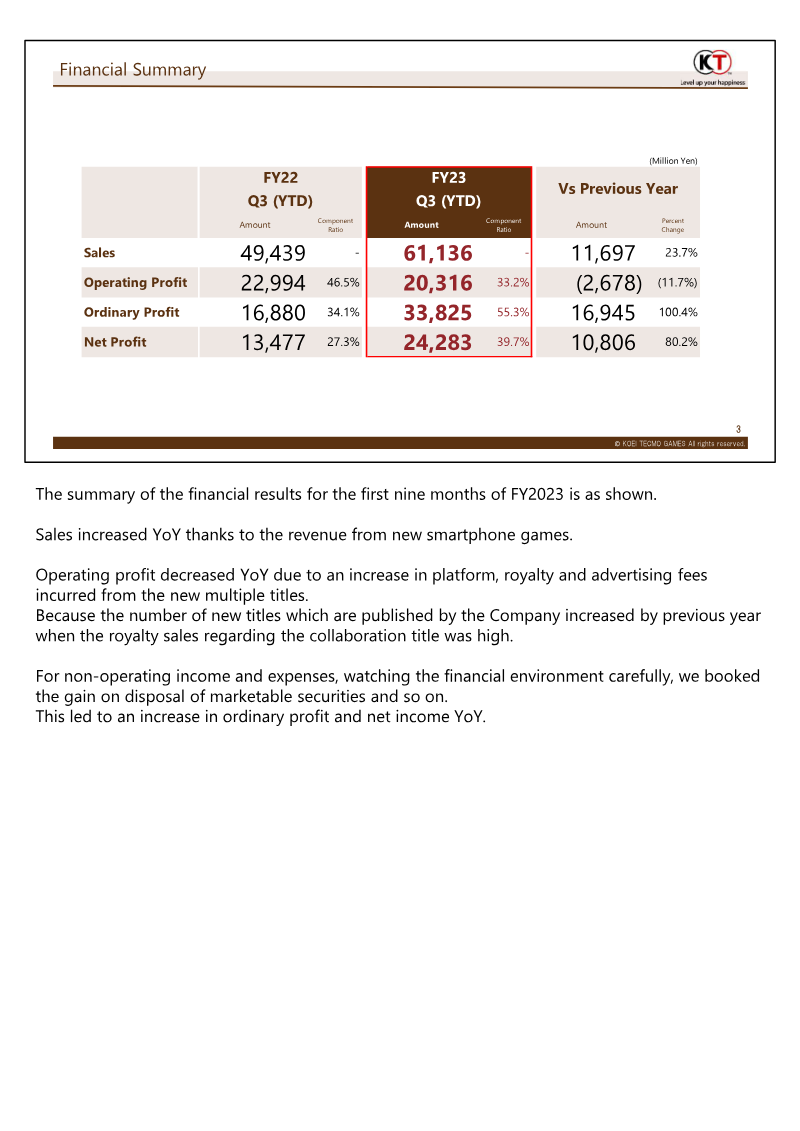

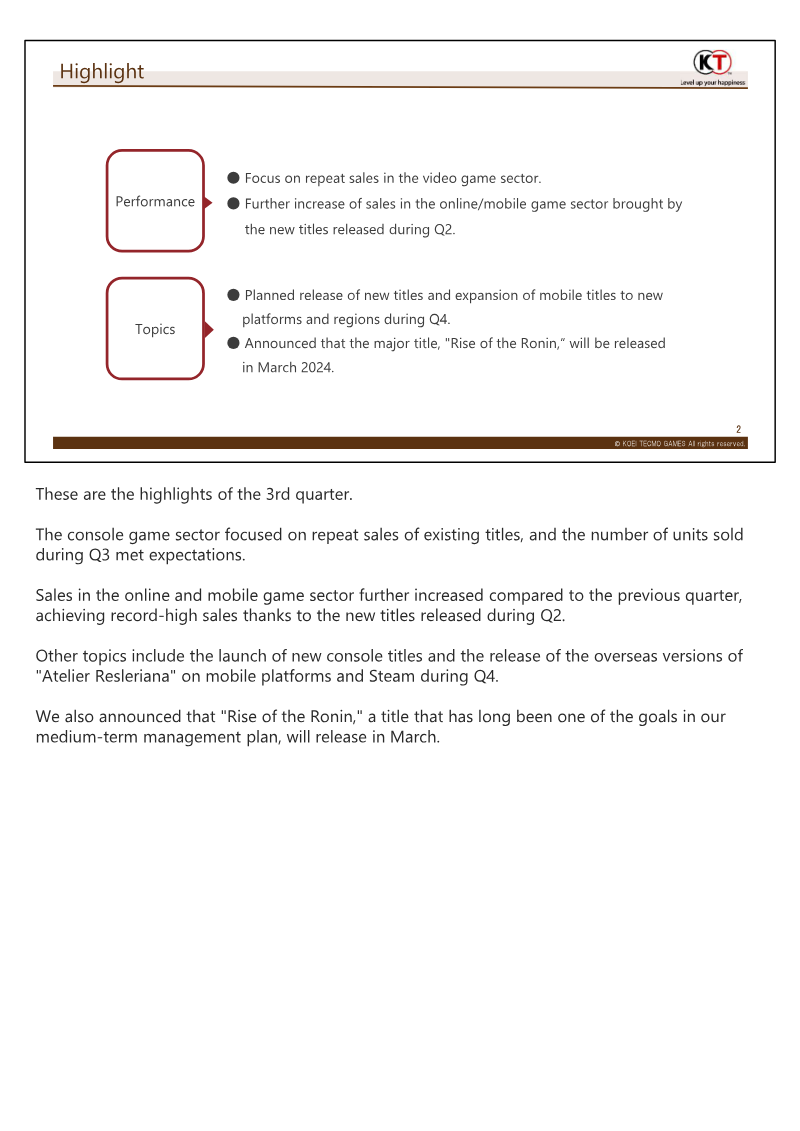

The quarterly financial release outlines KOEI TECMO HOLDINGS CO., LTD.’s performance for the first nine months of fiscal 2023, ending March 2024. Total sales rose 23.7 % YoY to ¥61,136 million, driven primarily by new mobile titles that boosted online and mobile game revenue. Operating profit fell 11.7 % to ¥20,316 million due to higher platform, royalty and advertising costs associated with the expanded title portfolio. Ordinary profit increased 100.4 % to ¥33,825 million and net profit grew 80.2 % to ¥24,283 million, largely supported by gains from marketable securities and other non‑operating items. Geographically, Japan contributed 61.1 % of sales while overseas sales accounted for 38.9 %, with the United States and Europe showing modest declines in unit volumes but maintaining strong digital sales. The entertainment segment recorded a 24 % YoY sales increase, with mobile and online channels contributing 47.1 % of segment revenue; console package sales declined by 10.3 %. Digital sales ratio for the entertainment sector rose to 84.2 %, reflecting a shift toward downloadable content and mobile downloads. Cost analysis revealed a 12.9 % rise in employment costs, a 78.8 % jump in subcontracting expenses, and a 92.8 % increase in advertising spend, all linked to new title launches. The company maintains its FY2024 operating profit target of ¥37,500 million, citing anticipated revenue from the March release of “Rise of the Ronin” and continued expansion in mobile markets.

Koei Tecmo