Digital Market Index: Q1 2024

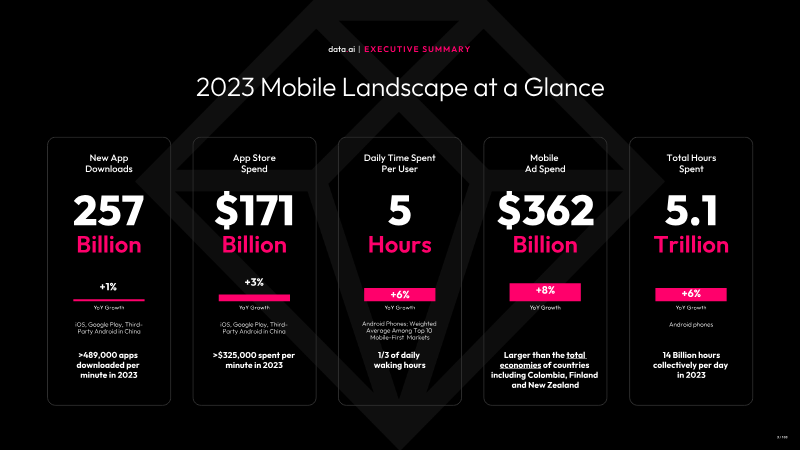

Global consumer spending on mobile applications reached a record $45 billion in the first quarter of 2024, reflecting a 9.5% year‑over‑year increase that was largely driven by the iOS ecosystem, which grew 11.5% versus a 5.3% rise on Google Play. Despite this surge in spend, total app downloads fell 3.5%, marking the third consecutive quarterly decline since Q1 2021; nevertheless, iOS maintained its highest quarterly download volume since 2020. Entertainment and productivity categories led the spend growth, each expanding over 30% YoY, while gaming spending rebounded on iOS but remained flat on Google Play.

Hyper‑casual games continued to dominate the download landscape, with racing and action titles generating the largest volumes. Conversely, casual sub‑genres such as arcade and simulation experienced double‑digit declines. TikTok remained the top spender globally, generating more than $1.2 billion in revenue and outpacing YouTube by a wide margin, while emerging short‑form drama apps—ReelShort, DramaBox, and ShortMax—entered the top ten for both revenue and download growth. In mobile gaming, “Monopoly GO” set a new quarterly spend record of $770 million, surpassing the previous $765 million benchmark and standing alone as a title to exceed $600 million in a single quarter.

Retail‑media advertising in the United States was led by Walmart and Target, which together delivered over 18 billion impressions in Q1 2024. Specialized retailers such as Chewy and Home Depot captured significant niche shares, with personal care emerging as the top category overall—driven by Ulta and Sephora. Walmart dominated food, beverages, and consumer packaged goods, while Target excelled in shopping, household supplies, and baby & toddler segments. Co‑branded partnerships—including Chewy × Purina, Walmart × Unilever, and Target × Apple—generated hundreds of millions of impressions, underscoring the strategic value of retailer‑brand collaborations in expanding digital ad reach.