Report

Annual Report and Accounts 2025

ANNUAL REPORT AND ACCOUNTS 2025 ANNUAL REPORT AND ACCOUNTS 2025 Frontier is a leading independent developer and CONTENTS publisher of video games for PC and consoles, HEADLINES STRATEGIC REPORT creating immersive and fun gameplay with high See a summary of the headlines for FY25, 01 Headlines production values.

Frontier Developments

Report

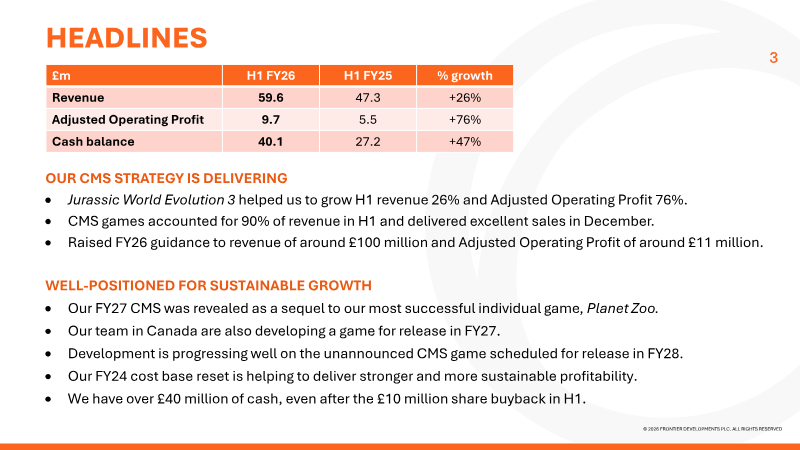

FY26 H1 Results Presentation

The information contained in this confidential the account or benefit of, U.S. Persons (as defined in or advisers take any responsibility for, or will accept any shareholders, directors, officers, agents, employees or document ("Presentation") has been prepared liability whether direct or indirect, express or implied, advisers.

Frontier Developments

Report

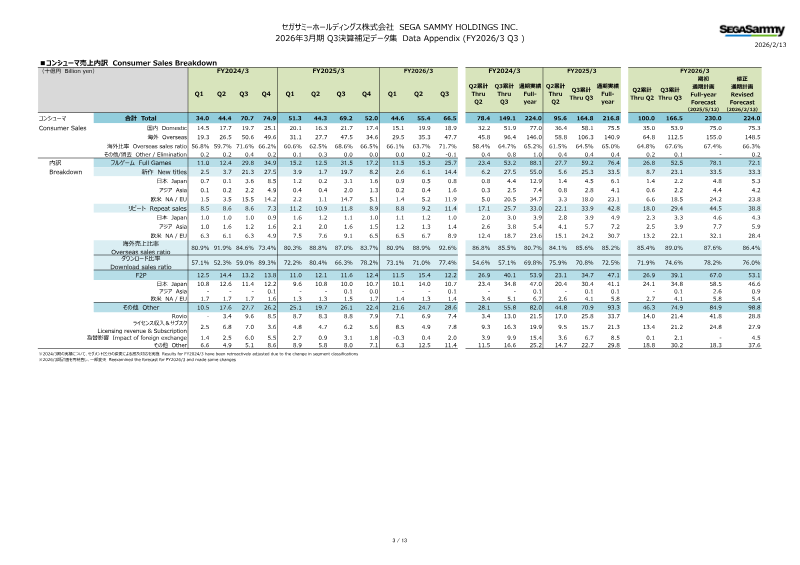

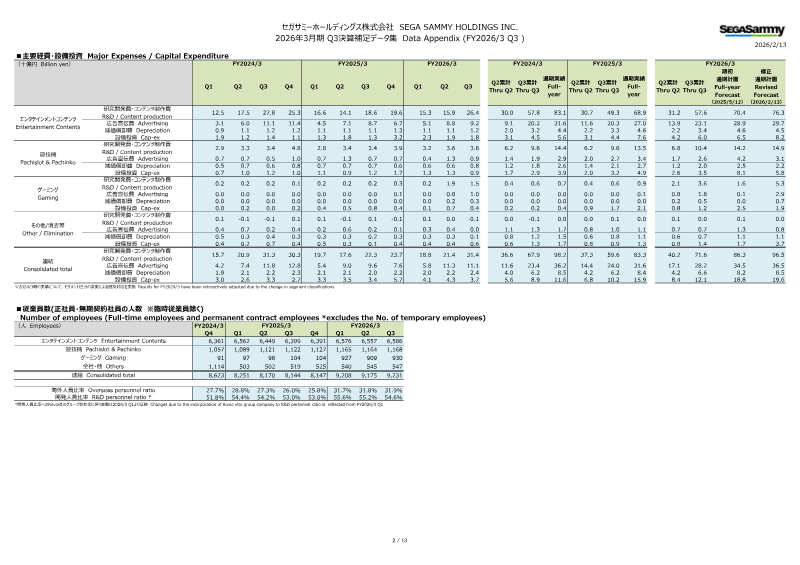

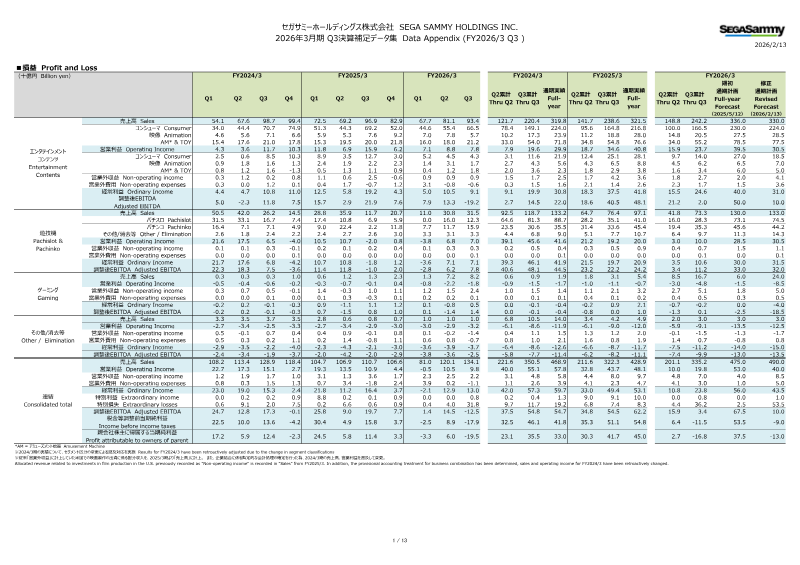

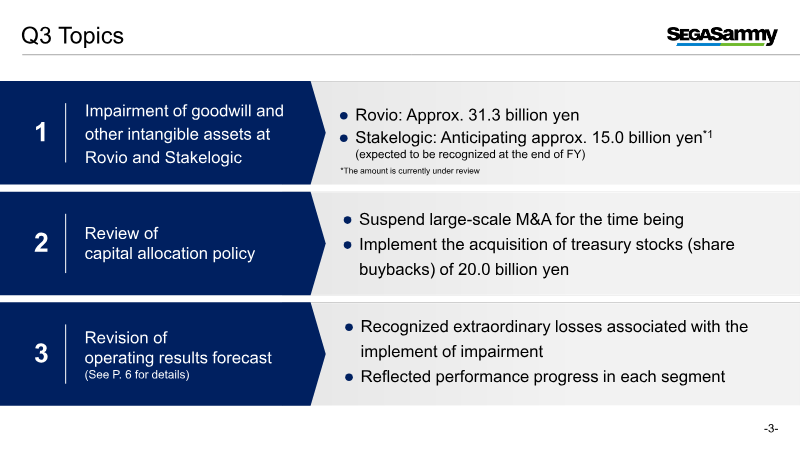

Results Presentation: Q3 for the Fiscal Year Ending March 2026

Q3 for the Fiscal Year Ending March 2026 The market forecasts, performance outlooks, plans, strategies, and other forward-looking statements contained in this document are based on information available to the Company and the judgment of its management at the time this material was created. They do not constitute a guarantee of future performance.

Sega Sammy Holdings