ReportUkie

Press Start on Growth: Unlocking the Full Potential of the UK Video Games Industry

1 May 20252 pages~7 min full read

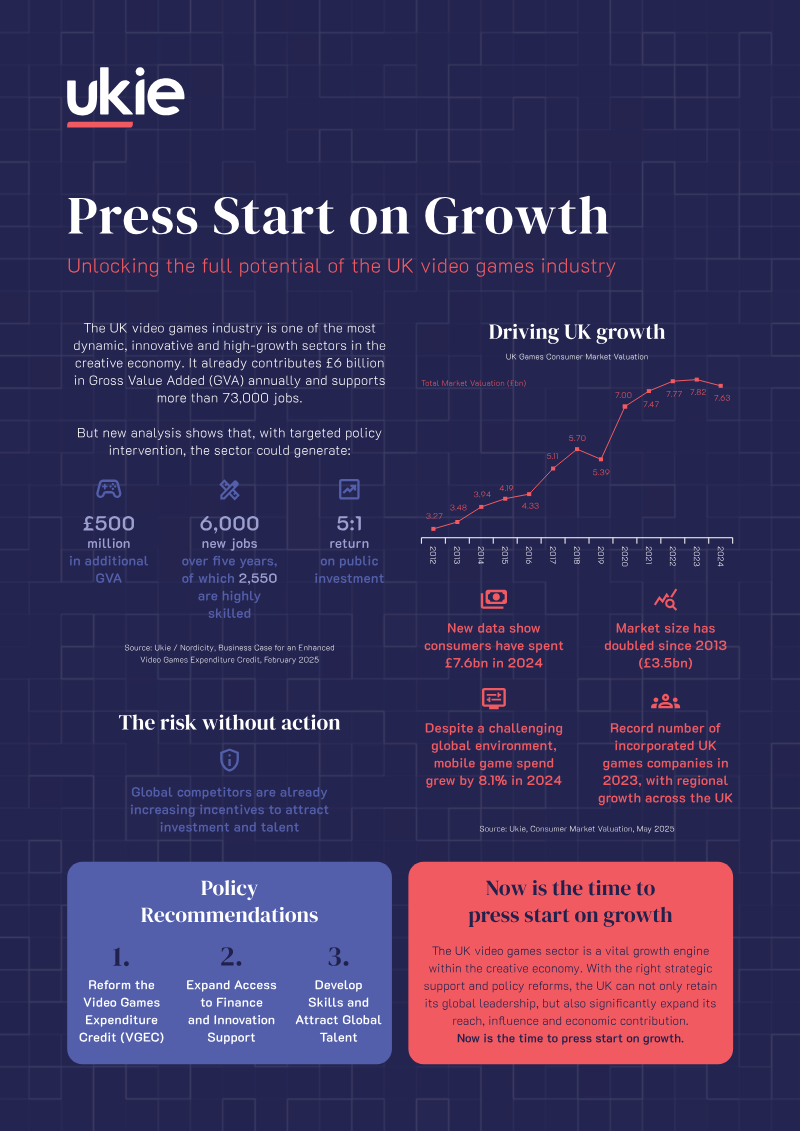

The UK video games industry currently contributes £6 billion in gross value added (GVA) and supports over 73,000 jobs, with the potential to add £5.7 billion in GVA and 5.4 million jobs over the next five years through strategic policy intervention.

See it on page 1Physical boxed software sales have collapsed, falling 34% year-on-year to represent only 4% of total market spend.

See it on page 2Esports experienced a significant surge of 44% year-on-year, driven by an increase in UK-based tournaments, contrasting with a 15% contraction in live-event spending.

See it on page 2Mobile gaming in the UK grew by 8%, though this remains below the 13% regional Western-European average.

See it on page 2Hardware sales for major consoles, including the PS5 disc edition, Xbox, and Nintendo Switch, weakened, while the PS5 digital edition achieved record software sales at a lower price point.

See it on page 2Game-culture engagement across PC and console categories declined by 13%, accompanied by an 8.5% drop in related toy and merchandise sales.

See it on page 2The analysis argues that the United Kingdom’s video‑games sector is a high‑growth pillar of the creative economy, already delivering roughly £6 billion in gross value added (GVA) and supporting more than 73 000 jobs, and that strategic policy action could lift its contribution to about £7.6 billion in 2024 and generate an additional £5.7 billion GVA and up to 5.4 million jobs over the next five years. The assessment covers the full UK market from 2022 through 2024, spanning software, hardware, live events, esports, ancillary merchandise and related media, and benchmarks performance against Western‑European averages.

Key findings show a continued erosion of physical boxed software, which fell 34 % year‑on‑year and now accounts for only 4 % of total spend, while mobile games grew 8 %—still below the 13 % regional average. Full‑game digital purchases slipped due to a thin slate of blockbuster releases, yet overall game volume remained stable. Live‑event spending contracted 15 % after pandemic‑related cancellations, whereas esports surged 44 % YoY, driven by a rise in UK‑based tournaments. Subscription revenue rose modestly as price hikes offset a near‑saturation of console subscriber bases. Hardware sales weakened for PS5 disc and Xbox consoles and for the Nintendo Switch, while the PS5 digital edition posted record software sales at a lower price point. Game‑culture engagement declined 13 % across PC and console categories, and related toy and merchandise sales fell 8.5 %.

The conclusions stress that without targeted reforms—particularly in financing, skills development, and talent support—the sector risks losing its global leadership. Conversely, coordinated policy could unlock further growth, broaden international reach, and reinforce the UK’s position as a leading hub for video‑games innovation and cultural influence. Data are drawn from industry sources such as Omdia, Ukie, NielsenIQ/GfK Entertainment, BFI, Comscore and the Official Charts Company, reflecting a comprehensive market‑valuation approach across multiple