Report

Half-Yearly Report: 2014

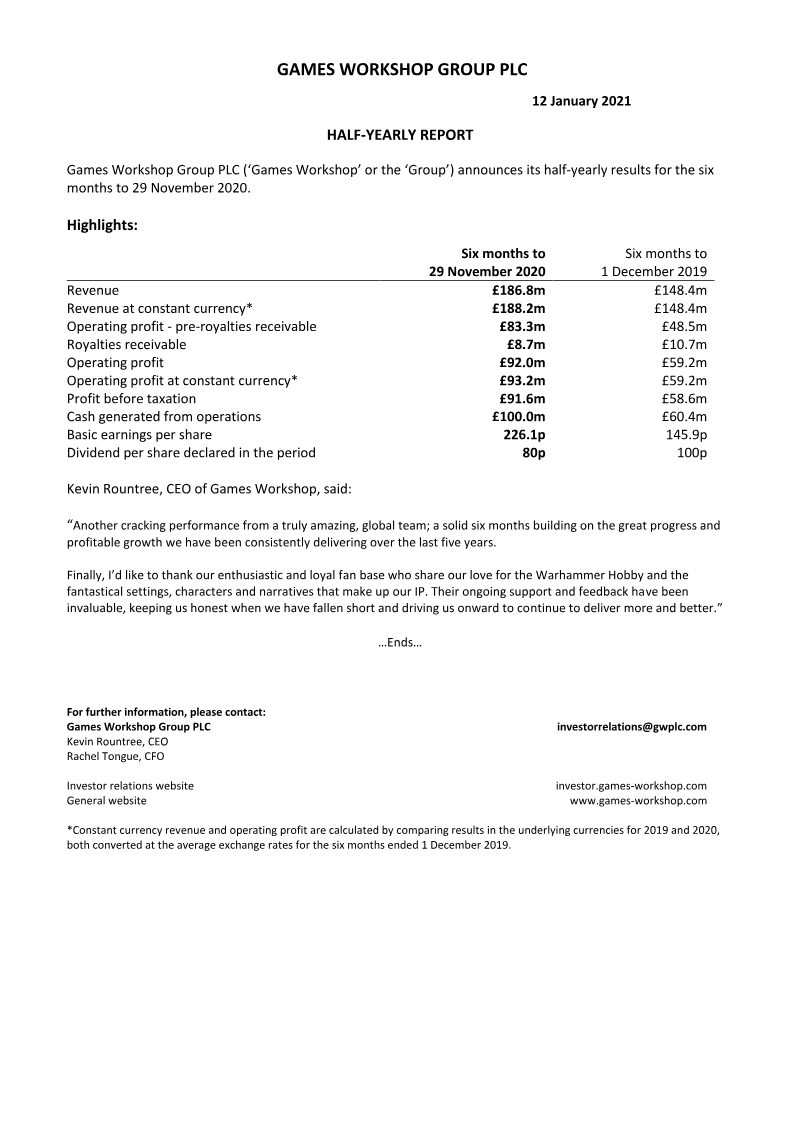

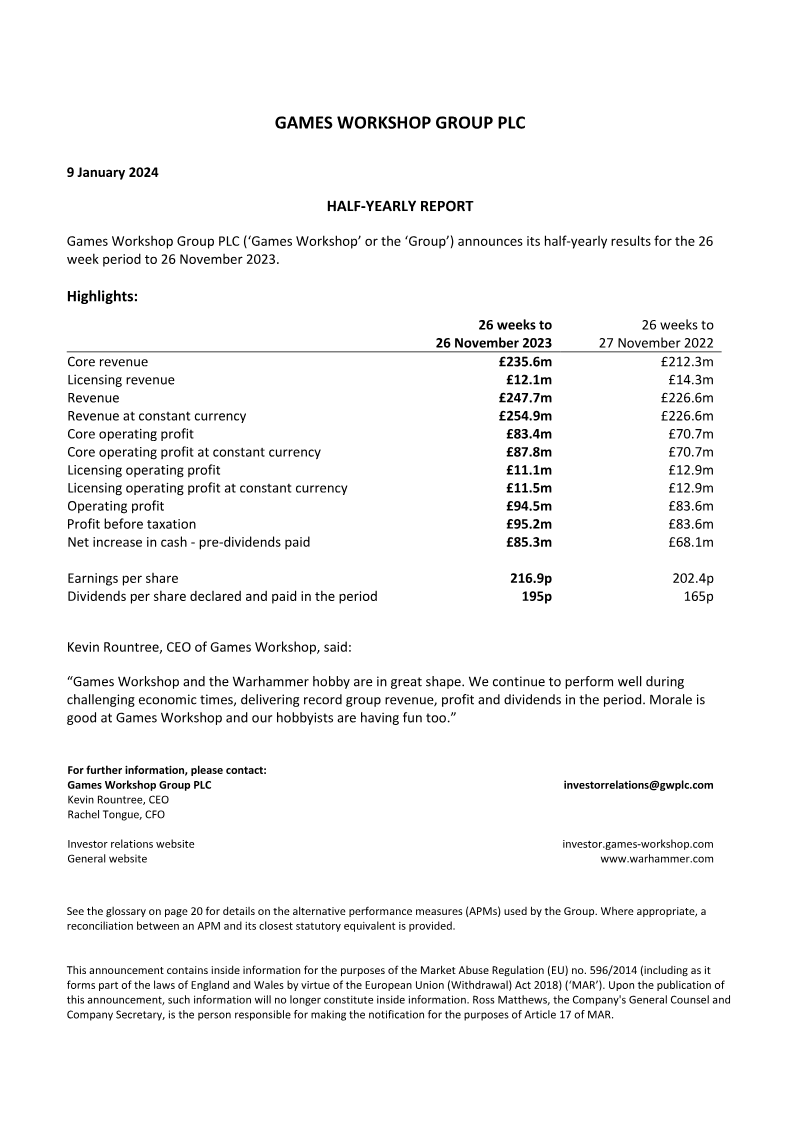

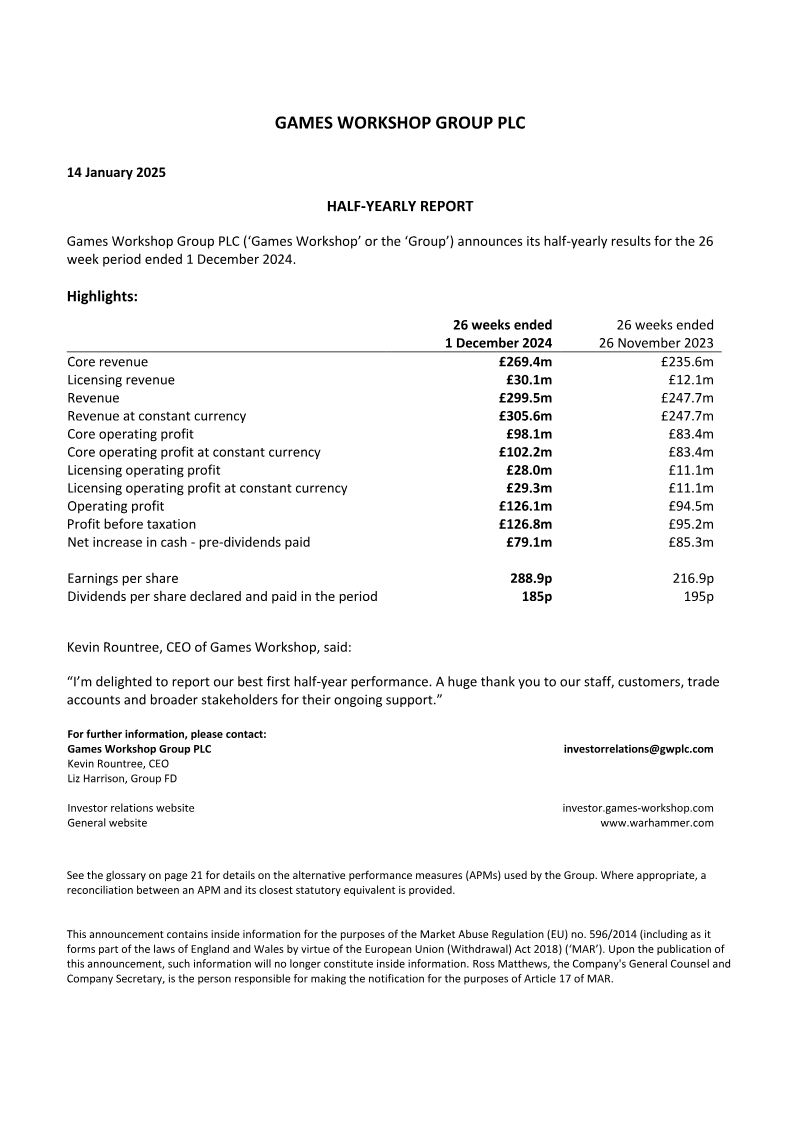

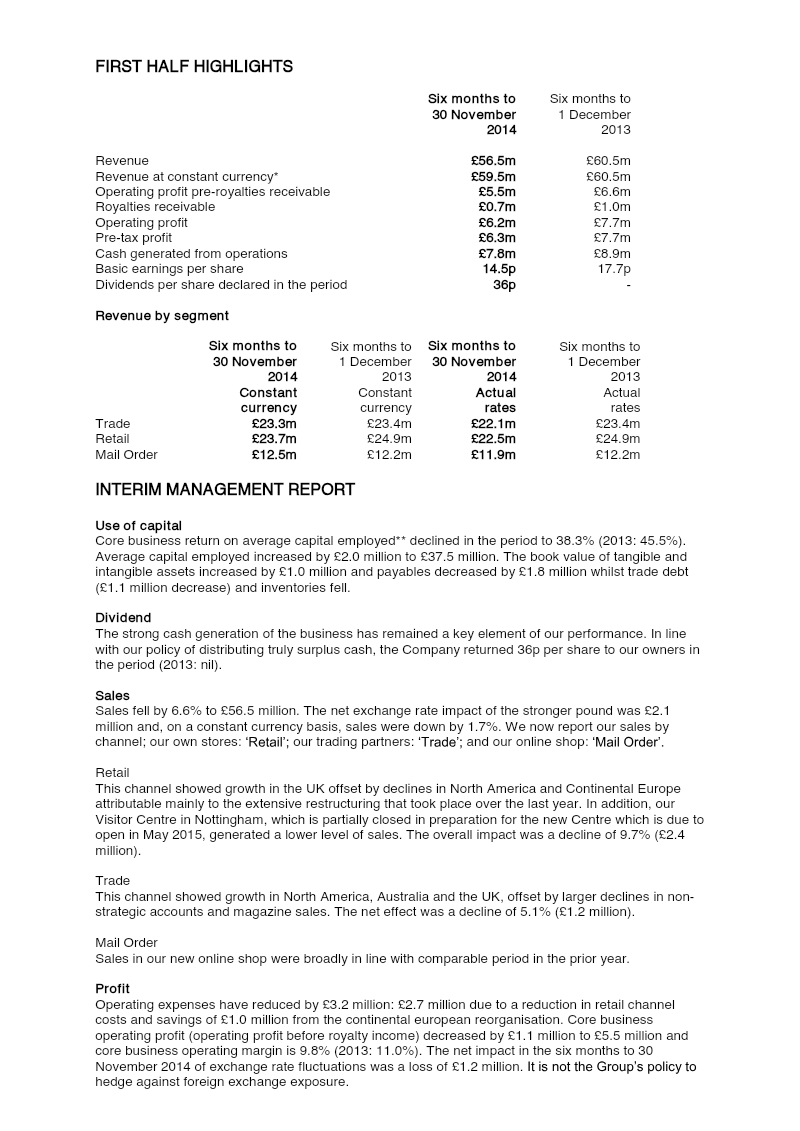

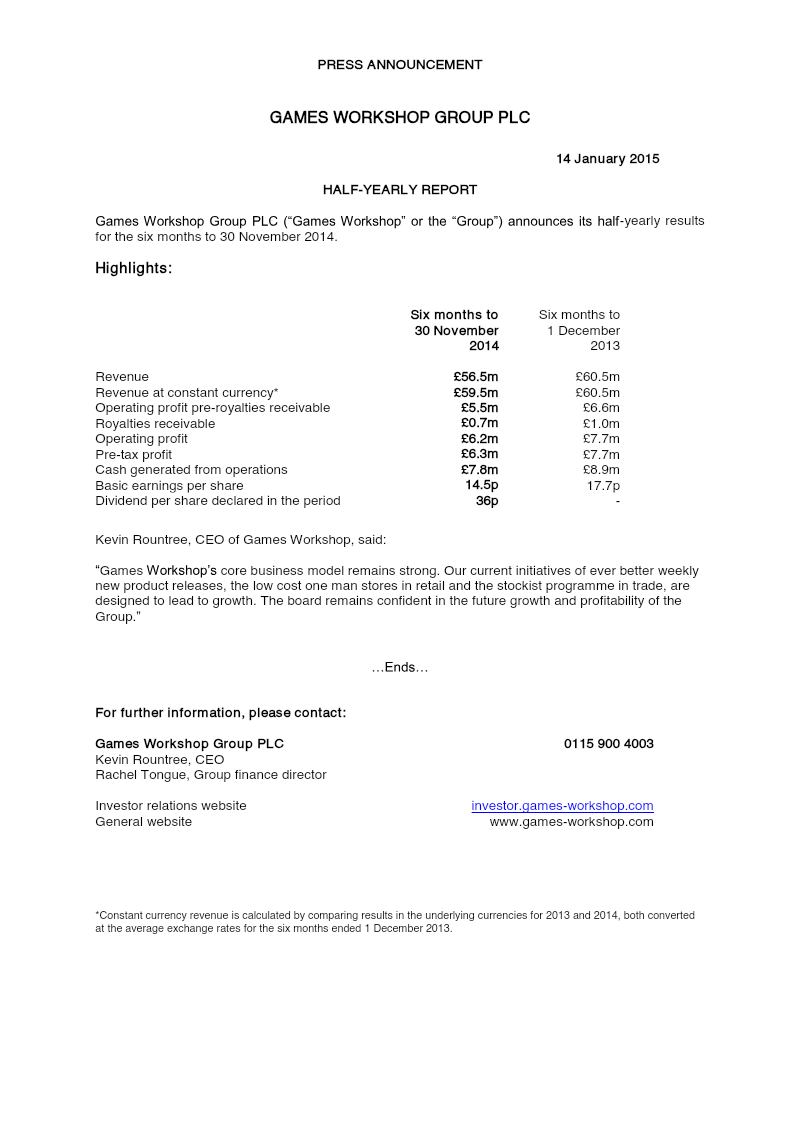

Games Workshop Group PLC (“Games Workshop” or the “Group”) announces its half-yearly results for the six months to 30 November 2014. Six months to Six months to Revenue £56.5m £60.5m Revenue at constant currency* £59.5m £60.5m Operating profit pre-royalties receivable £5.5m £6.6m Royalties receivable £0.7m £1.0m Operating profit ...

Games Workshop Group

Report

Half-Yearly Report and Trading Update: 2015-2016

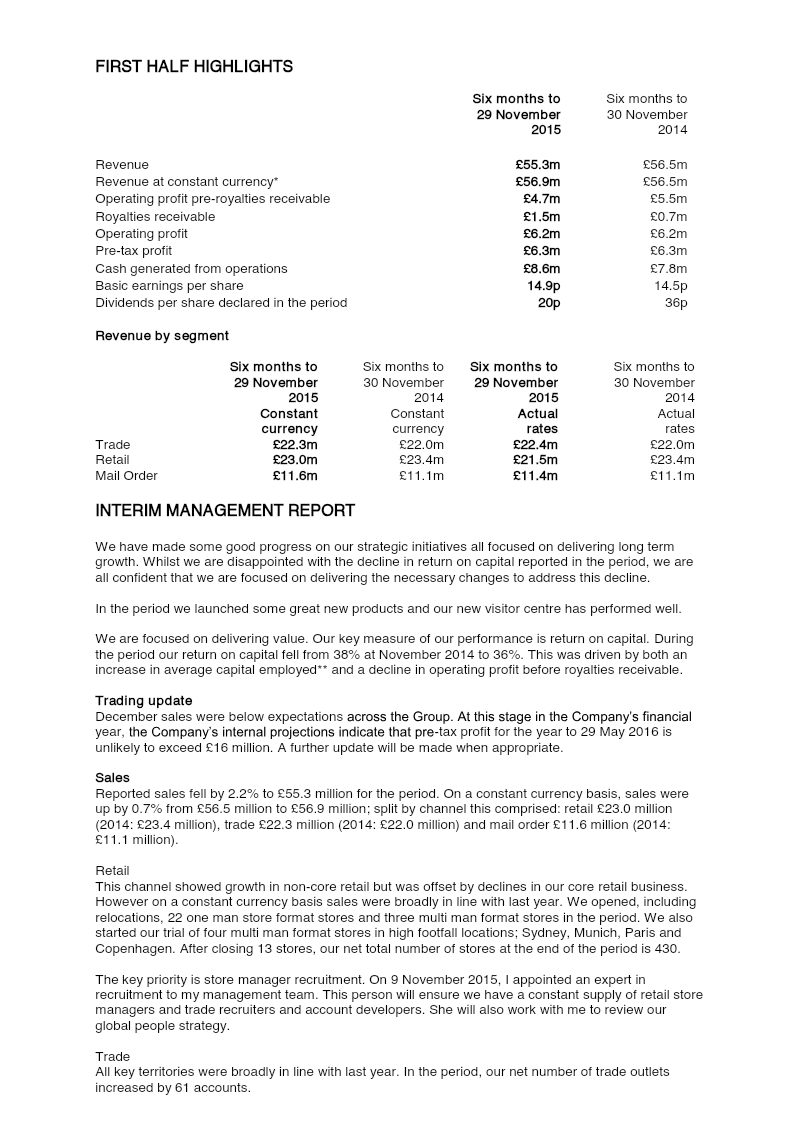

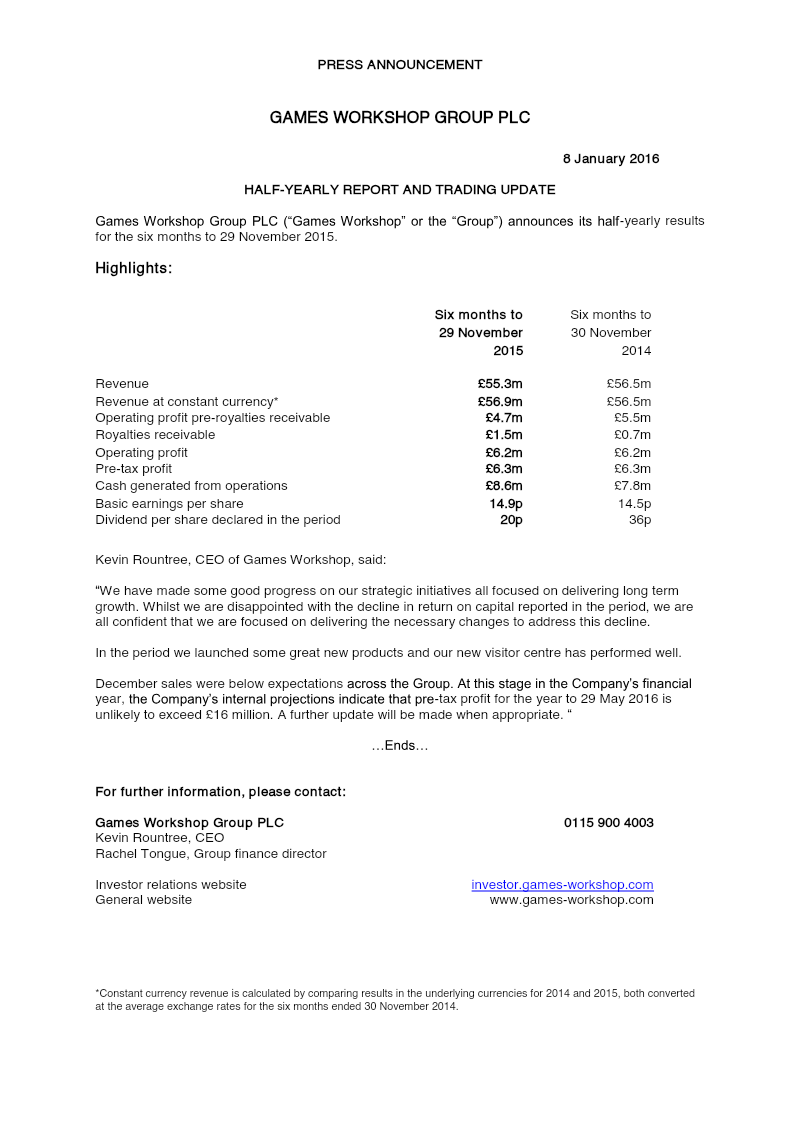

HALF-YEARLY REPORT AND TRADING UPDATE Games Workshop Group PLC (“Games Workshop” or the “Group”) announces its half-yearly results for the six months to 29 November 2015. Six months to Six months to 29 November 30 November 2015 2014 Revenue £55.3m £56.5m Revenue at constant currency* £56.9m £56.5m Operating profit pre-royalties receivable ...

Games Workshop Group

Report

Half-Yearly Report: 2016-2017

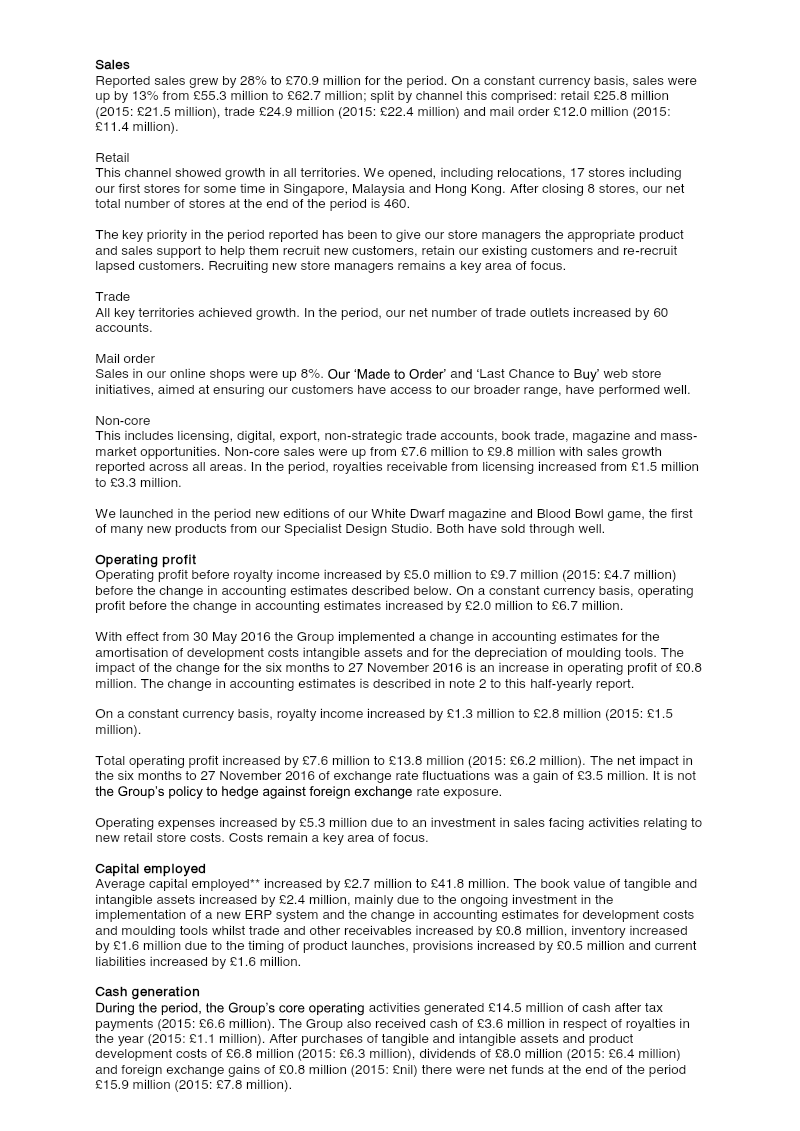

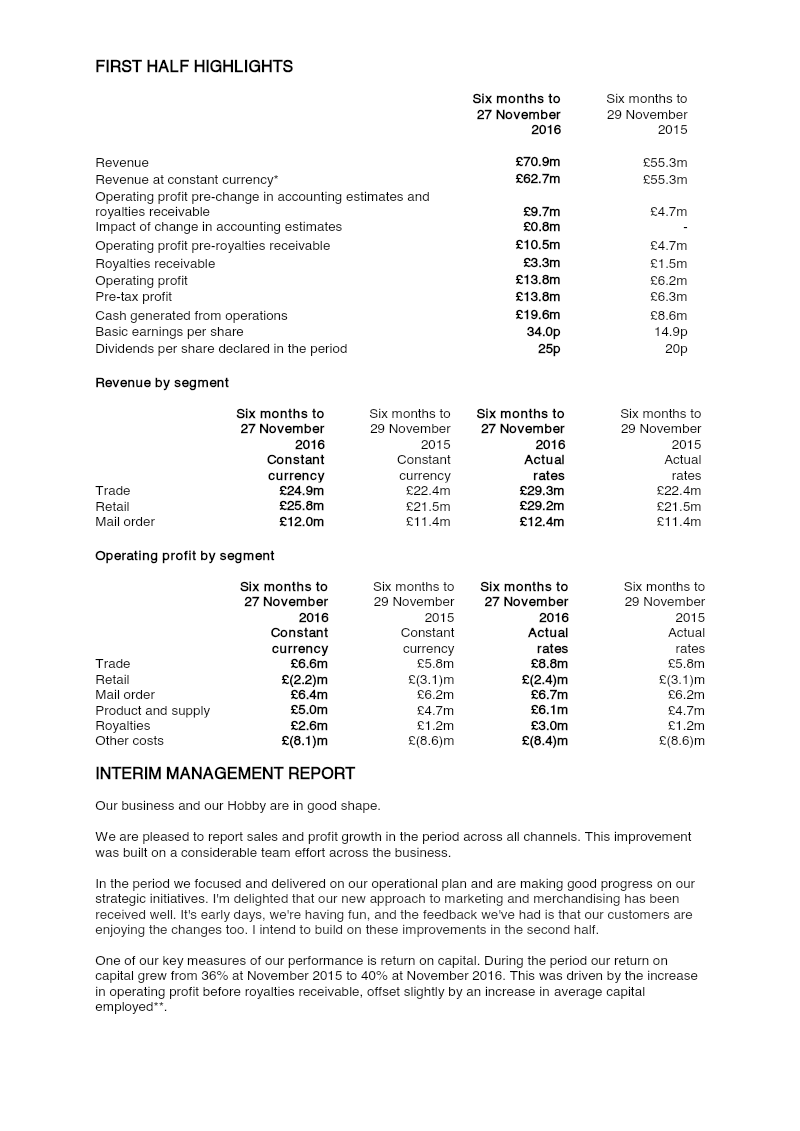

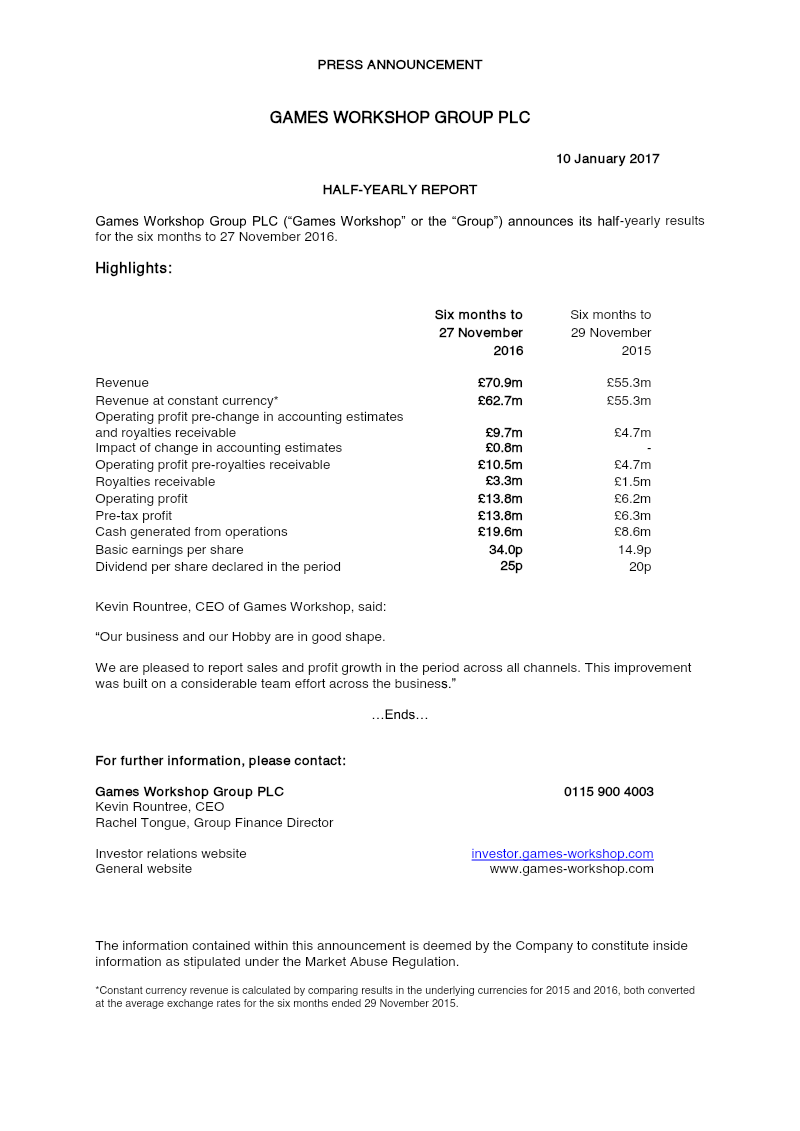

Games Workshop Group PLC (“Games Workshop” or the “Group”) announces its half-yearly results for the six months to 27 November 2016. 27 November 29 November Revenue £70.9m £55.3m Revenue at constant currency* £62.7m £55.3m Operating profit pre-change in accounting estimates and royalties receivable £9.7m £4.7m Impact of change in accounting estimates ...

Games Workshop Group