Skip to main content

Game Industry

Library

Library

Search

Ask AI

News

Connect your AI

Browse

The Catch Up

Topics

Collections

Writers

Help

Subscribe

Game Industry

Library

Library

Search

Ask AI

Saved

Library

175 reports matching your filters

All Types

Reports

Articles

Presentations

Whitepapers

Financial

Legal

Other

Search

Player Demographics

Market Analysis

Global

Player Behavior

Monetization

Mobile

Europe

USA

PC

Diversity & Inclusion

Esports

Market Forecast

Marketing

North America

Console

Africa

Game Design

Steam

Clear

Filters

1

Player Demographics

Recently added

Newest first

Oldest first

Title A–Z

Title Z–A

Report

14 pages

Female Gamers in Asia: Version for Women in Games Asia Panel

Female gamers in Asia represent 35% of the region's 1.46 billion total gamers, with a year-over-year growth rate of 7.6% that outpaces the 5.0% growth of the general gaming population.

In 2021, female gamer spending on mobile titles reached $13.07 billion in China and $5.52 billion across the Asia-10, while PC spending reached $9.70 billion and $3.93 billion respectively.

Mobile is the primary platform for this demographic, with 95% of female gamers playing on mobile devices, compared to 60% on PC and 17% on consoles.

Player Demographics

Market Analysis

Diversity & Inclusion

+1

Niko Partners

Oct 2022

Report

48 pages

Market Outlook 2022: An Overview & Analysis of Industry Trends

The global mobile gaming market is projected to reach $117 billion in annual revenue by 2026, despite a 6% year-over-year revenue decline to $21.2 billion in early 2022.

Mid-core genres, specifically RPG and strategy, drive 60% of total player spending, while casual titles account for 78% of total downloads.

Asian markets contribute 80% of total RPG and MMORPG revenue, though Western appetite for these complex titles is growing, evidenced by Diablo Immortal earning $28 million in the U.S. during its first six weeks.

Market Analysis

Player Demographics

Monetization

+1

Sensor Tower

Aug 2022

Report

28 pages

Essential Facts About the Video Game Industry 2022

The U.S. gaming industry generated $60.4 billion in total sales in 2021, with 67% of players participating in in-game purchases.

Approximately 215.5 million Americans, or 66% of the population, play video games at least weekly.

Pandemic-era engagement levels have stabilized, with 90% of players maintaining or increasing their playtime since the peak of the pandemic.

Market Analysis

Player Demographics

Player Behavior

+1

Entertainment Software Association

Jun 2022

Report

48 pages

Mobile Gaming Market Outlook 2022

The mobile gaming market is in a stabilization phase, with quarterly downloads holding at 14 billion despite a 6% year-over-year revenue decline to $21.2 billion in early 2022.

Casual games dominate volume at 80% of all downloads, while Mid-Core titles remain the primary revenue driver, accounting for 60% of total player spending.

The Asia-Pacific region is a critical economic force, generating 80% of global MMORPG revenue and 62% of Card Battler revenue.

Market Analysis

Market Forecast

Player Demographics

+2

Sensor Tower

May 2022

Report

31 pages

Motivations and Demographics Snapshot Report

Renovation and customization mechanics are now a fundamental requirement for casual gaming, appearing in 100% of the top-100 grossing casual titles released in the last two years.

Motivational drivers for US mobile gaming are highly demographic-specific, with younger males prioritizing mastery and competition in PvP, while players aged 45 and older favor social slots.

The 'Expression' driver, centered on customization and decoration, is a primary engagement factor particularly among female players who show a strong preference for tycoon and creative titles.

Market Analysis

Player Demographics

Mobile

+1

GameRefinery

Feb 2022

Report

31 pages

Motivations and Demographics Snapshot Report: The Motivations Driving Top Mobile Games, February 2022

Gender and age are primary indicators of genre preference, with women comprising 63% of the audience for Match3 and Hidden Object games, while men make up 76% to 84% of the audience in 4X strategy and synchronous PvP titles.

Every top-grossing casual game released between 2020 and 2022 has integrated renovation and customization elements to increase player expression and broaden market appeal.

Motivational drivers are demographic-specific; younger males prefer high-sensomotoric challenges like Battle Royales, while players aged 45 and older seek similar thrills through low-sensomotoric experiences like Slots.

Market Analysis

Player Demographics

Player Behavior

+2

GameRefinery

Feb 2022

Report

18 pages

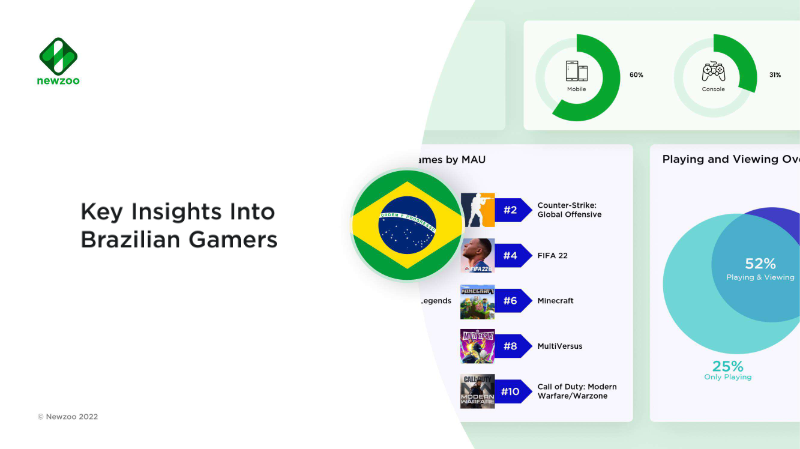

Key Insights into Brazilian Gamers

Brazil is the 10th largest gaming market globally by revenue and 5th by total player count as of 2022.

Engagement is high, with 80% of the online population identified as game enthusiasts and 60% of players also consuming gaming video content.

Mobile is the dominant platform, used by 60% of the gaming population, followed by consoles at 31% and PC at 30%.

Player Demographics

Market Analysis

Brazil

Newzoo

Jan 2022

Report

18 pages

Consumer Insights: Games & Esports 2022

Gaming has become a primary entertainment ecosystem for 79% of the global online population, with Gen Alpha prioritizing gaming over social media and streaming video.

Consumer spending in the gaming sector is projected to exceed $200 billion in 2023, driven by a payer base that includes approximately 50% of Gen Alpha, Gen Z, and Millennial gamers.

Game worlds are increasingly used for social interaction rather than gameplay, with 75% of players and 44% of non-players utilizing these environments for non-gaming social engagement.

Market Analysis

Player Demographics

Esports

+1

Newzoo

Jan 2022

Report

11 pages

Key Insights Into South Korean Gamers

South Korea is the world's fourth-largest gaming market, generating $8.3 billion in annual revenue from a highly engaged base of 33 million gamers.

Gaming is a deeply integrated social activity, with 76% of the online population participating, 48% both playing and watching content, and 22% specifically following esports.

Mobile is the primary platform for 59% of the online population, though PC gamers demonstrate higher engagement with an average of five hours of play per week.

Player Demographics

Player Behavior

Market Analysis

+1

Newzoo

Jan 2022

Report

19 pages

State of Anime Gaming 2022

Anime-themed mobile games generated 20% of total global mobile game consumer spend in 2021 despite accounting for only 1% of total usage.

Japan remains the dominant market, representing 55% of global anime-game spend in 2021, though its market share has declined by nine percentage points since 2018.

Global downloads for anime-style games grew 50% between 2018 and 2021, with South Korea emerging as a top growth market showing a 170% increase in downloads and 85% increase in spend.

Market Analysis

Global

Mobile

+1

data.ai

Jan 2022

Report

4 pages

Southeast Asia’s Games Market

The Southeast Asian games market across six major countries generates approximately $5 billion in revenue from 270 million gamers and is projected to grow at a compound annual rate of 8.6% through 2025.

Esports is a primary market driver, with over 200 million viewers and 60% of the regional gaming population expressing a strong interest in competitive play.

Female gamers represent 40% of the total gaming population, with growth in this demographic outpacing the general market and reaching nearly 50% in Indonesia and Singapore.

Market Analysis

Market Forecast

Player Demographics

Niko Partners

Jan 2022

Report

19 pages

Video Games – A Force for Good: Europe's Video Game Industry

The European video game market maintained a stable value of €23.3 billion in 2021, following the initial pandemic-driven surge.

The industry employs over 98,000 people across Europe, with 74,000 of those roles based within the EU.

Digital revenue dominates the sector, accounting for 81% of total market value through app-based gaming and in-game purchases.

Market Analysis

Player Demographics

Esports

+1

Interactive Software Federation of Europe

Jan 2022

Report

29 pages

Analyzing the Consumer and Market Impacts of Chinese Games Market Policies: China

China’s regulatory environment has tightened through strict anti-addiction laws for minors, which now cap playtime, limit in-game spending, and restrict live-streaming access for users under 18.

The licensing framework now requires detailed content reviews and real-name verification, increasing operational costs and long-term investment risks for both domestic and foreign developers.

While the licensing process is complex, a new policy allowing a single license for multiplatform releases is incentivizing developers to prioritize cross-platform title development.

Market Analysis

Player Demographics

China

Newzoo

Jan 2022

Report

11 pages

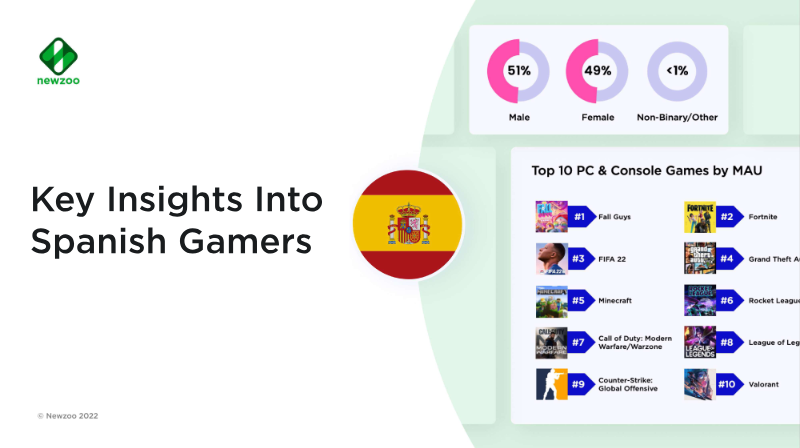

Key Insights Into Spanish Gamers

Spain is the 13th largest global gaming market, generating $2.38 billion in annual revenue with 83% of the online population aged 10 to 65 identified as enthusiasts.

The Spanish gaming audience is gender-balanced at 51% female and 49% male, with peak participation occurring between the ages of 21 and 50.

While mobile is the most popular platform with 60% reach, PC and console users exhibit higher engagement, averaging four hours of weekly play compared to three hours for mobile users.

Market Analysis

Player Demographics

PC

Newzoo

Jan 2022

Report

24 pages

Games India Plays!: A Look into the Gaming Habits of Indian Mobile Gamers and How to Reach Them

The Indian mobile gaming market reached $2.2 billion in 2022, driven by a base of 373 million online gamers where 91% play exclusively on mobile devices.

Real Money Gaming (RMG), including fantasy sports and card games, accounts for over 50% of total industry revenue.

The core demographic for adventure and battle royale genres is young and male-skewing, with 55% of players falling within the 13-27 age bracket.

Market Analysis

Player Demographics

Mobile

+1

Newzoo

Jan 2022

Report

31 pages

Annual Report of the German Games Industry 2022

The German computer games market reached a total valuation of 14 billion euros in 2022.

The industry maintains a significant player base of 8 million individuals across Germany.

The sector is supported by a structured framework of 26 industry-specific companies and employment entities.

Market Analysis

Player Demographics

Germany

Game – Verband der deutschen Games-Branche e.V.

Jan 2022

Report

18 pages

Key Insights Into UK Gamers

The UK is a major global gaming hub, ranking sixth in revenue and tenth in player population, with 71% of the population aged 10-65 identifying as game enthusiasts.

Engagement is evenly split between active players (36%) and those who both play and view gaming video content (35%).

Mobile gaming has the highest reach at 46%, followed by console (41%) and PC (29%), though PC and console users dedicate more time to gaming weekly.

Market Analysis

Player Demographics

Esports

+1

Newzoo

Jan 2022

Report

22 pages

Newzoo Gamer Insights: The Future of Gaming

90% of Gen Alpha and Gen Z are active game enthusiasts, significantly higher than the 79% engagement rate seen in the general online population.

Gaming is the primary entertainment source for Gen Alpha and a top-three source for Gen Z, competing directly with social media and video streaming platforms.

Economic engagement is high, with 52% of Gen Alpha and 48% of Gen Z spending money on games, primarily driven by mobile platform purchases for exclusive content and personalization.

Market Analysis

Player Demographics

Marketing

+1

Newzoo

Jan 2022

Report

21 pages

Newzoo’s Global Gamer Study 2022

Gaming has become a primary entertainment ecosystem for 79% of the global online population, with Gen Alpha prioritizing gaming over social media and streaming.

The gaming sector reached a projected consumer spend exceeding $200 billion in 2023, with approximately 50% of Millennials, Gen Z, and Gen Alpha actively spending money on games.

Gaming is increasingly used as a social platform, as 75% of players engage in game worlds for social interaction rather than playing the primary game mechanics.

Market Analysis

Player Demographics

Player Behavior

+1

Newzoo

Jan 2022

Report

44 pages

VR Games Market Report 2022

The global active VR hardware install base is projected to reach 46 million units by 2024, driven by a 42% compound annual growth rate.

Gaming is the primary driver of the VR ecosystem, with 72% of headset owners using devices for gaming and nearly 60% engaging with them on a weekly basis.

Standalone headsets, such as the Meta Quest 2, are the primary catalysts for market expansion by increasing accessibility compared to traditional PC-based hardware.

Market Analysis

VR

Global

+1

Newzoo

Jan 2022

Previous

1

…

5

6

7

…

9

Next