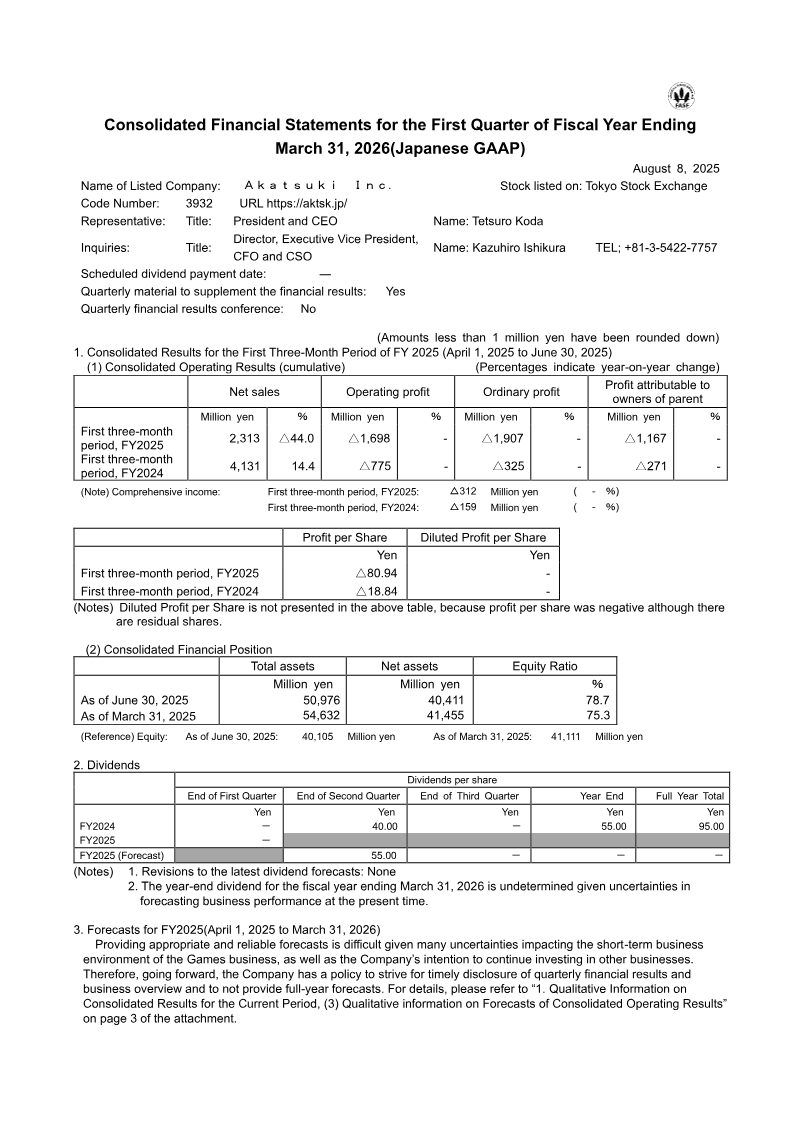

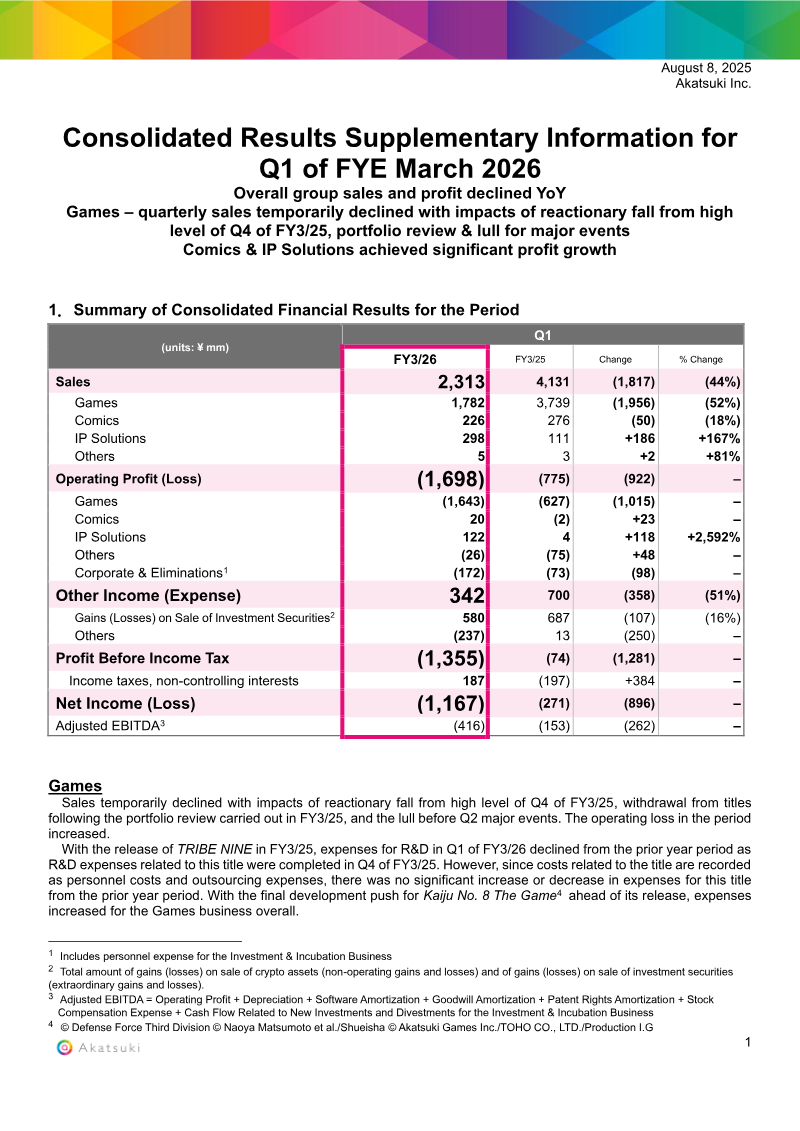

Akatsuki Inc. reported a sharp decline in consolidated sales and operating results for Q1 of the fiscal year ending March 2026, with total group sales falling 44% YoY to ¥2,313 million. The Games segment suffered the largest hit, dropping 52% to ¥1,782 million and recording an operating loss of ¥1,643 million, largely due to a post‑Q4 portfolio review withdrawal and the absence of high‑profile releases. R&D spending for the Games business fell from the previous year as development on “TRIBE NINE” concluded, but costs for the upcoming title “Kaiju No. 8 The Game” increased personnel and outsourcing expenses.

In contrast, the Comics division saw a modest 18% sales decline to ¥226 million but improved profitability, with operating profit rising from a loss of ¥2 million to ¥20 million. The division’s focus on original works and continued service provision to the overseas platform MANGA MIRAI contributed to this turnaround. The IP Solutions unit experienced explosive growth, with sales up 167% to ¥298 million and operating profit soaring 2,592% to ¥122 million, driven by the successful online lottery “Slash Gift” and the inclusion of CRAYON, Inc. in consolidation.

Other income sources shifted, with gains on investment securities decreasing by ¥107 million to ¥580 million. Net income swung from a loss of ¥271 million in FY3/25 to a larger loss of ¥1,167 million in FY3/26, reflecting the combined impact of segment downturns and higher operating losses. Adjusted EBITDA also deteriorated from ¥153 million to a loss of ¥416 million.

The financial data cover the Japanese market, covering all core segments—Games, Comics, IP Solutions, and ancillary services—from Q1 FY3/24 through Q1 FY3/26. The analysis relies on consolidated financial statements, trend tables, and explanatory notes detailing segment performance, expense composition, and investment activity.