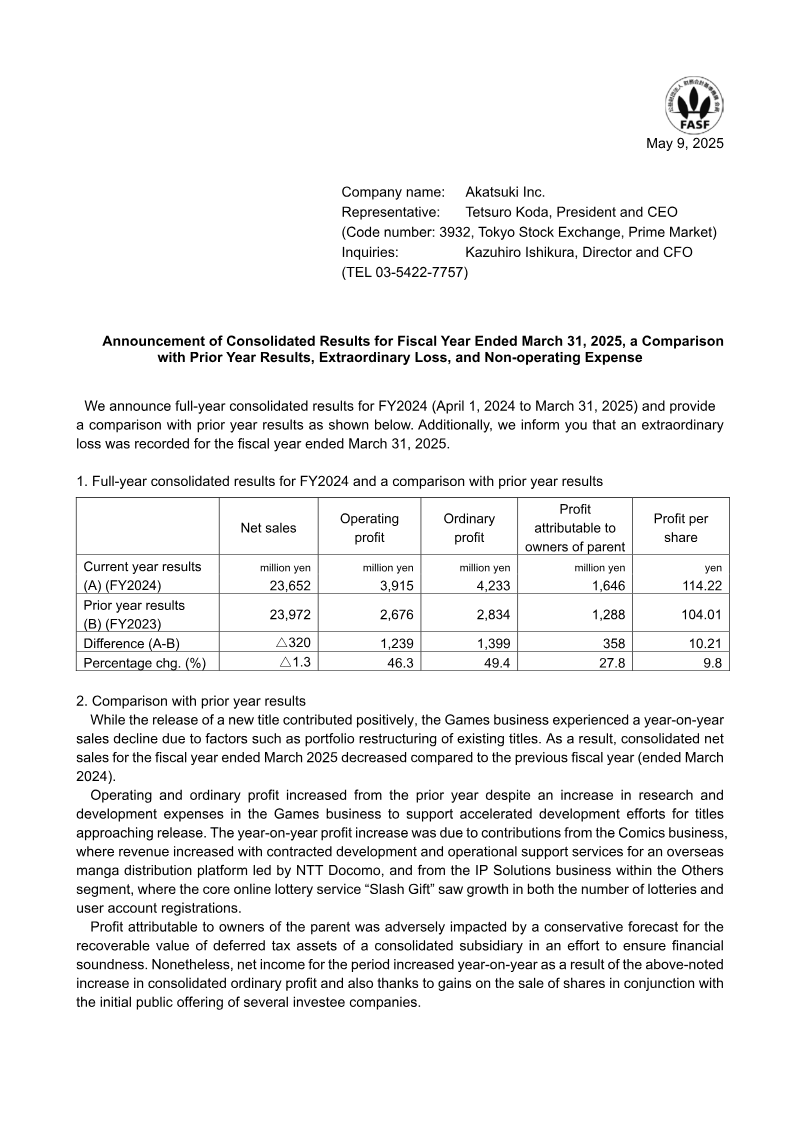

ReportAkatsuki

Announcement of Consolidated Results for Fiscal Year Ended March 31, 2025, a Comparison with Prior Year Results, Extraordinary Loss, and Non-operating Expense

2 pages~3 min full read

Akatsuki Inc. reported a 49.4% increase in ordinary profit to ¥4,233 million for the fiscal year ending March 31, 2025, despite a 1.3% decline in net sales to ¥23,652 million.

See it on page 1Operating ordinary profit grew by 46.3% to ¥3,915 million, driven by strong performance in the Comics segment and the 'Slash Gift' online lottery service within the IP Solutions business.

See it on page 1Net income attributable to owners of the parent rose 27.8% to ¥1,646 million, bolstered by gains from share sales related to the IPOs of investee companies.

See it on page 1The Games segment experienced a decline in revenue during FY2025, failing to offset the overall sales decrease despite the launch of a new title.

See it on page 1The company recorded an extraordinary loss of ¥593 million due to a conservative valuation of investment securities held by the group.

See it on page 2Non-consolidated financial statements included a ¥5,776 million provision for doubtful accounts and a ¥2,454 million loss on valuation of shares in affiliated companies, though these had a minimal impact on consolidated results.

See it on page 2Profitability was partially constrained by a conservative write-down of deferred tax assets, which reduced the final net income attributable to owners.

See it on page 1Akatsuki Inc. reported consolidated financial results for the fiscal year ending March 31, 2025 (April 1 2024–March 31 2025). Net sales fell by 1.3 % to ¥23,652 million from ¥23,972 million in FY2023, reflecting a decline in the Games segment despite a new title launch. Operating ordinary profit rose by ¥1,239 million (46.3 %) to ¥3,915 million, driven largely by gains in the Comics and IP Solutions businesses; the former benefited from contracted services for an overseas manga platform, while the latter saw growth in its online lottery service “Slash Gift.” Ordinary profit attributable to parent shareholders increased by ¥1,399 million (49.4 %) to ¥4,233 million, and net income attributable to owners of the parent grew by ¥358 million (27.8 %) to ¥1,646 million, aided by gains on share sales from IPOs of investee companies. A conservative write‑down of deferred tax assets reduced the profit attributable to owners, yet overall net income still improved.

An extraordinary loss of ¥593 million was recorded on the valuation of investment securities held by the group, reflecting a conservative assessment of recoverable value amid market uncertainty. On a non‑consolidated basis, the company recorded a ¥5,776 million provision for doubtful accounts and a ¥2,454 million loss on valuation of shares in affiliated companies; these items are largely confined to consolidated subsidiaries and have a minor impact on the consolidated results. The report covers Japan‑based operations for FY2025, with data derived from internal financial statements and market assessments.