CESA Game Industry Report 2025: Launch Seminar Report

6 pages~2 min full read

The CESA Game Industry Report 2025 Launch Seminar, held in Tokyo on February 20, 2026, served as a platform to analyze the evolving landscape of the Japanese gaming sector. The event introduced the updated 2025 industry report, which features expanded data sets and enhanced international market research to better support the global expansion of Japanese firms. The seminar aimed to address industry needs for technical knowledge sharing, talent development, and cross-sector networking among corporate and academic stakeholders.

Key findings highlight a significant shift toward the integration of generative AI, with approximately half of domestic game companies now utilizing these tools within their development pipelines. While internal production workflows show high adoption rates, industry experts noted a more cautious approach regarding AI-generated content visible to end-users. Legal discussions emphasized the importance of navigating copyright frameworks, specifically distinguishing between AI learning and generation phases, while balancing innovation with intellectual property risks.

Government representatives from the Ministry of Economy, Trade and Industry and the Agency for Cultural Affairs outlined strategic support for the content industry, targeting 20 trillion yen in overseas sales by 2033. Policy initiatives focus on multi-year funding, tax incentives, and robust talent development programs to ensure long-term competitiveness. Furthermore, legal experts underscored the increasing complexity of global regulatory environments, noting that Japanese companies must proactively manage diverse international requirements regarding data privacy, monetization, and rating systems. By synthesizing perspectives from government, legal, and development sectors, the seminar emphasized that strategic investment and regulatory compliance are essential for the sustainable growth of Japan’s gaming industry in a globalized market.

CESA – Computer Entertainment Supplier's Association · 2026

CESA – Computer Entertainment Supplier's Association · 2025

CESA – Computer Entertainment Supplier's Association · 2025

CESA – Computer Entertainment Supplier's Association · 2025

CESA – Computer Entertainment Supplier's Association · 2025

一般社団法人コンピュータエンターテインメント協会 (Computer Entertainment Supplier’s Association) · 2024

Computer Entertainment Developers Association · 2024

CESA – Computer Entertainment Supplier's Association · 2024

CESA – Computer Entertainment Supplier's Association · 2024

CESA – Computer Entertainment Supplier's Association · 2024

CESA – Computer Entertainment Supplier's Association · 2023

CESA – Computer Entertainment Supplier's Association · 2023

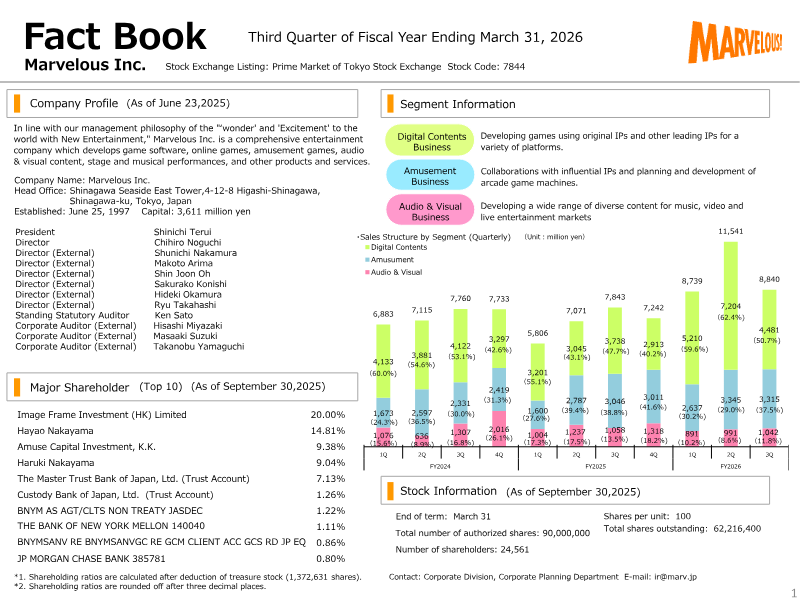

Marvelous · 2026

GungHo Online Entertainment · 2026

InvestGame · 2025

GREE · 2024

GREE · 2018

NEXON Co.

GREE

GREE

GREE

GREE

GREE

GREE