Report

FY2018 Second Quarter Financial Results

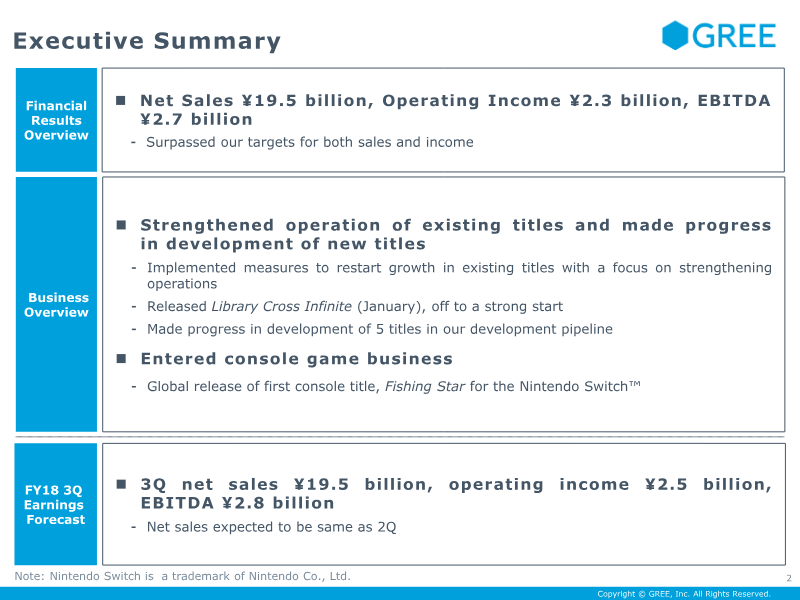

The FY2018 second‑quarter results demonstrate a successful rebound in sales and profitability, with net sales reaching ¥19.5 billion and operating income at ¥2.3 billion, slightly below the prior quarter but still surpassing year‑on‑year targets. EBITDA stood at ¥2.7 billion, reflecting a 12.0 % operating margin that narrowed by 0.5 percentage points QoQ. Revenue was dominated by paid‑service sales (¥17.21 billion) and ad‑media sales (¥2.25 billion). Cost control initiatives reduced total costs by ¥1.8 billion QoQ, driven mainly by lower advertising spend and commission fees; variable costs fell ¥1.92 billion while fixed costs remained stable. Strategically, the company expanded its portfolio by launching “Library Cross Infinite” in January and entering the console market with the Nintendo Switch title “Fishing Star.” Development pipelines now include five mobile titles, with two already released and three in advanced stages. Mobile operations benefited from new scenarios and large‑scale collaborations, while the advertising arm reported 1.8× QoQ growth in page views and advertiser numbers across its media brands. Forecasts for the third quarter project net sales of ¥19.5 billion and operating income of ¥2.5 billion, assuming continued cost discipline and steady growth in paid services. The company’s geographic focus remains global, with releases across Japan, Australia, India, South Korea, and Taiwan. Methodologically, figures derive from consolidated financial statements, with headcount totaling 1,407 across game, advertising, and corporate functions.

GREE

Report

FY2021 Third Quarter Financial Results

The FY2021 third‑quarter results demonstrate a robust performance driven largely by the launch of new titles and cost efficiencies. Net sales rose to ¥13.9 billion, up 0.23 % QoQ and down 1.53 % YoY from ¥15.44 billion in the same period of FY2020, while operating income increased to ¥1.72 billion, a 1.16 % QoQ gain and a 0.49 % YoY rise from ¥1.24 billion. EBITDA reached ¥1.91 billion, up 1.15 % QoQ and 0.55 % YoY from ¥1.36 billion, reflecting a 15 % operating‑income margin. Net income surged to ¥5.08 billion, a 2.09 % QoQ increase and 3.90 % YoY growth, largely attributable to profit from investment‑fund operations. Key drivers include the strong start of “Assault Lily: Last Bullet,” which entered distribution on January 20 and achieved a 16th‑place ranking in app sales, and the development of third‑party titles such as “That Time I Got Reincarnated as a Slime” and “Mao to Ryu no Kenkokutan.” Advertising costs fell by ¥0.38 billion QoQ, while commission fees declined due to reduced royalties from app games. Total costs decreased by ¥0.93 billion QoQ, driven by lower variable and fixed expenses. The company maintained a flexible capital policy through a stock‑repurchase program of up to 20 million shares (≈¥12 billion) and announced a dividend of ¥11 per share, up from ¥10 in FY2020. Geographic coverage spans Japan, North America, Europe, and Asia, with ongoing overseas distribution of multiple IP titles. The methodology relies on consolidated financial statements and quarterly operational data, providing a comprehensive view of performance across game development, live entertainment, and advertising initiatives.

GREE