FinancialTOHO HOLDINGS CO.

Financial Results for the First Half of Fiscal Year Ending March 2015: Japan

15 pages~24 min full read

Key insights

6 takeaways · ~2 min read- 01

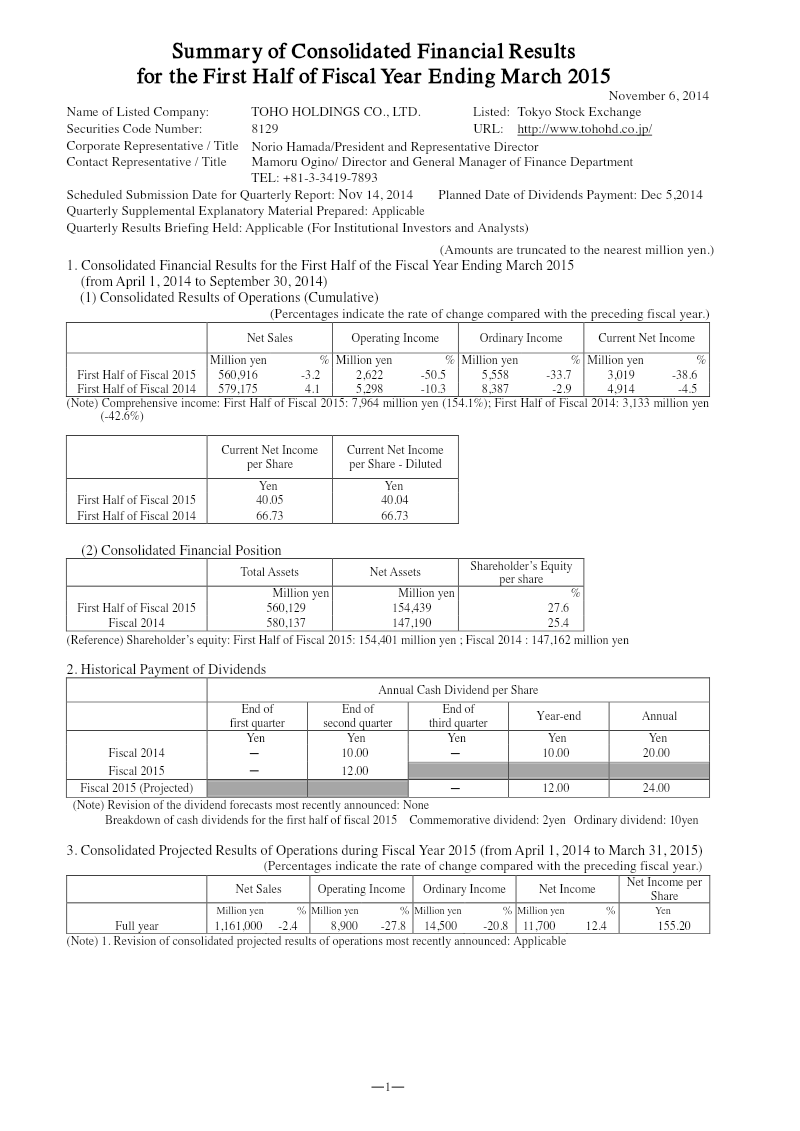

TOHO HOLDINGS reported a 50.5% decline in operating income to 2,622 million yen and a 3.2% decrease in net sales to 560,916 million yen for the first half of the fiscal year ending March 2015.

See it on page 1 - 02

The primary pharmaceutical wholesaling segment experienced a 42.6% drop in segment income, driven by faster-than-expected transitions to generic drugs and national health insurance price reductions.

See it on page 4 - 03

The dispensing pharmacy business saw an 86.7% collapse in segment income despite a 6.3% increase in sales, primarily due to elevated personnel and new pharmacy opening costs.

See it on page 4 - 04

Ordinary income and net income fell by 33.7% and 38.6% respectively, prompting the company to revise its full-year earnings forecast for the fiscal year ending March 2015.

See it on page 1 - 05

Operating cash flow improved to an inflow of 15,184 million yen, supported by a reduction in notes and accounts receivable, while total liabilities decreased by 6.3% to 405,690 million yen.

See it on page 5 - 06

Market performance was negatively impacted by a combination of national health insurance drug price cuts, a shift toward generic pharmaceuticals, and a contraction following a consumption tax hike.

See it on page 4