Back to Library

Summary

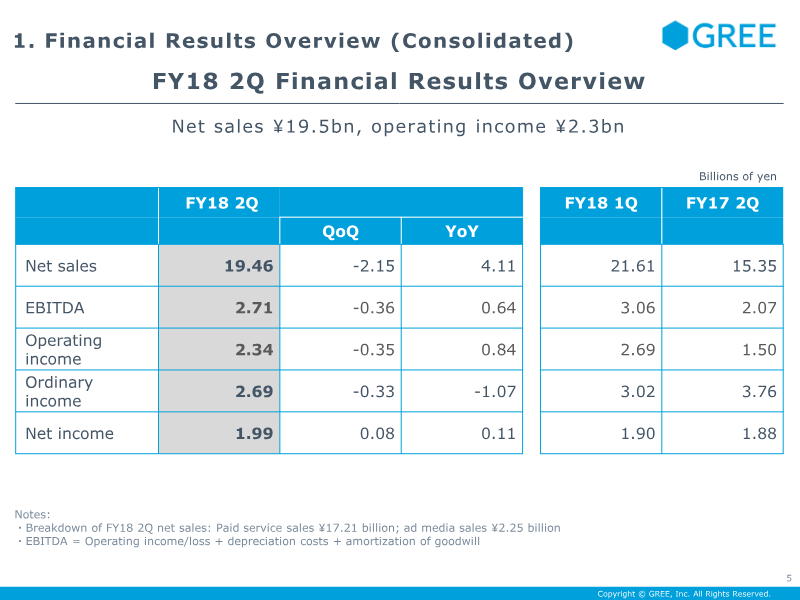

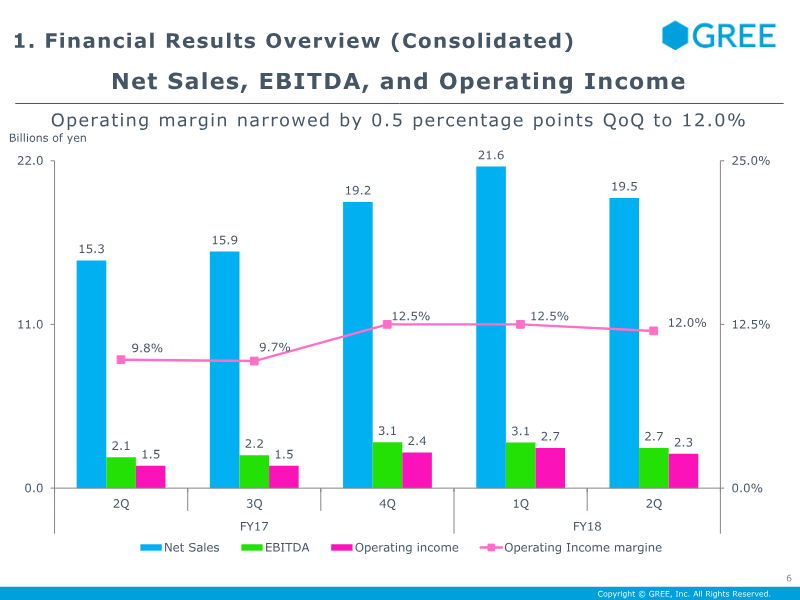

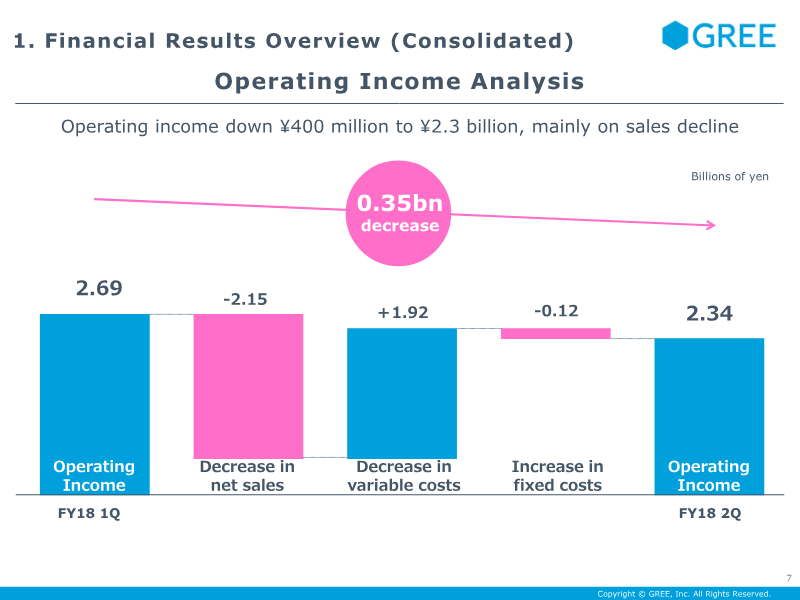

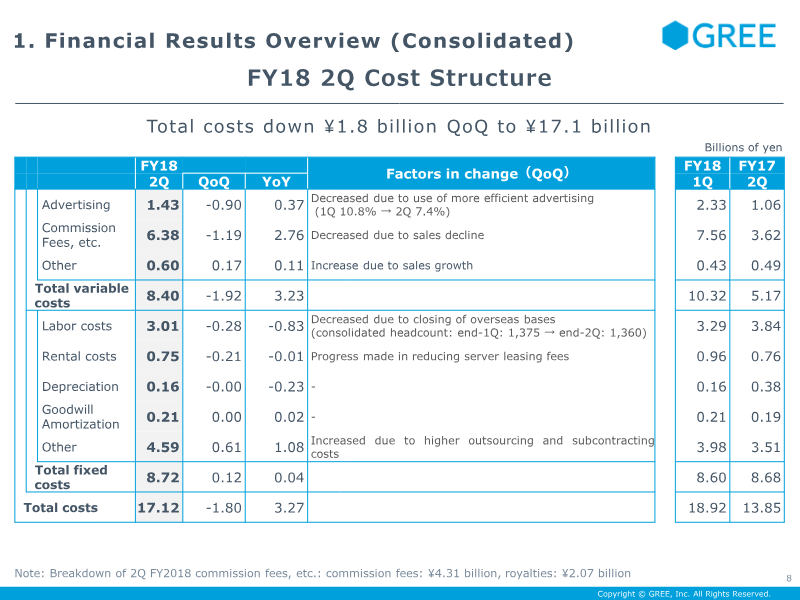

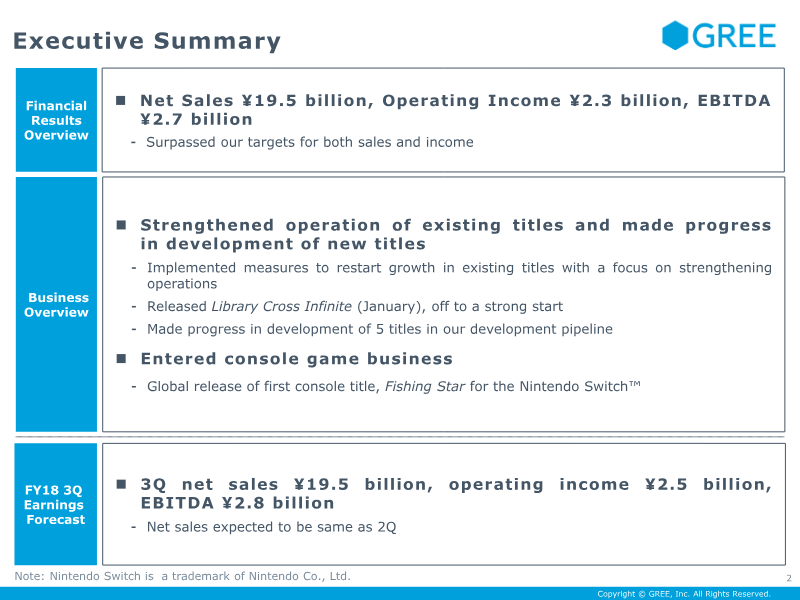

The FY2018 second‑quarter results demonstrate a successful rebound in sales and profitability, with net sales reaching ¥19.5 billion and operating income at ¥2.3 billion, slightly below the prior quarter but still surpassing year‑on‑year targets. EBITDA stood at ¥2.7 billion, reflecting a 12.0 % operating margin that narrowed by 0.5 percentage points QoQ. Revenue was dominated by paid‑service sales (¥17.21 billion) and ad‑media sales (¥2.25 billion). Cost control initiatives reduced total costs by ¥1.8 billion QoQ, driven mainly by lower advertising spend and commission fees; variable costs fell ¥1.92 billion while fixed costs remained stable. Strategically, the company expanded its portfolio by launching “Library Cross Infinite” in January and entering the console market with the Nintendo Switch title “Fishing Star.” Development pipelines now include five mobile titles, with two already released and three in advanced stages. Mobile operations benefited from new scenarios and large‑scale collaborations, while the advertising arm reported 1.8× QoQ growth in page views and advertiser numbers across its media brands. Forecasts for the third quarter project net sales of ¥19.5 billion and operating income of ¥2.5 billion, assuming continued cost discipline and steady growth in paid services. The company’s geographic focus remains global, with releases across Japan, Australia, India, South Korea, and Taiwan. Methodologically, figures derive from consolidated financial statements, with headcount totaling 1,407 across game, advertising, and corporate functions.

Tags

Pages

View all

Citation

Citation

Generating citation...

Similar Documents

Report

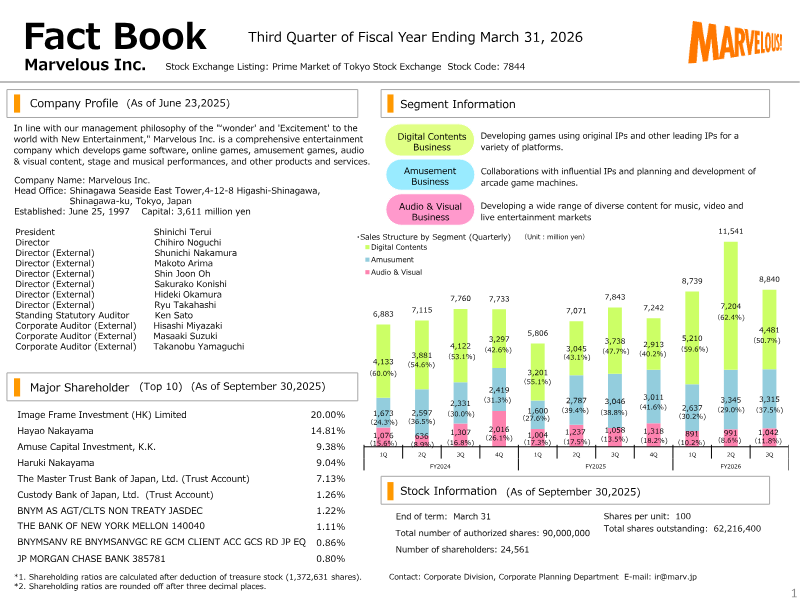

Factbook: Third Quarter of Fiscal Year Ending March 31, 2026

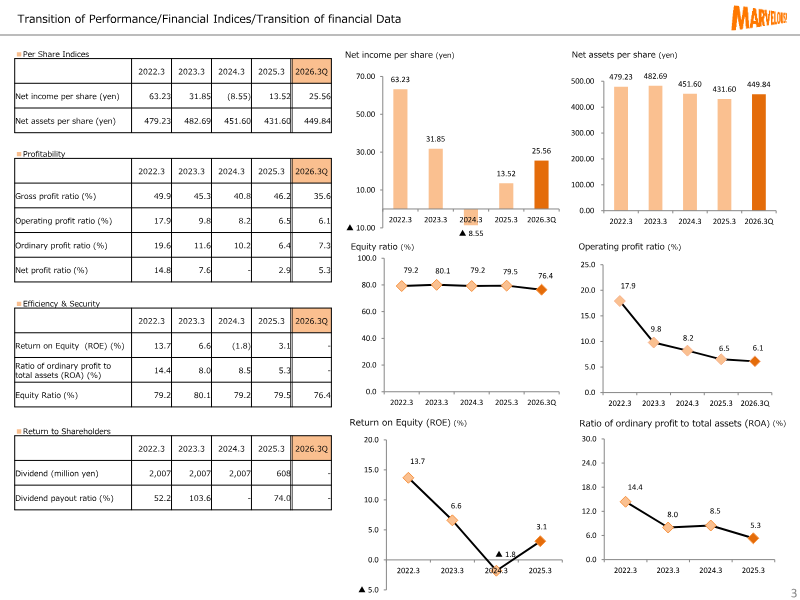

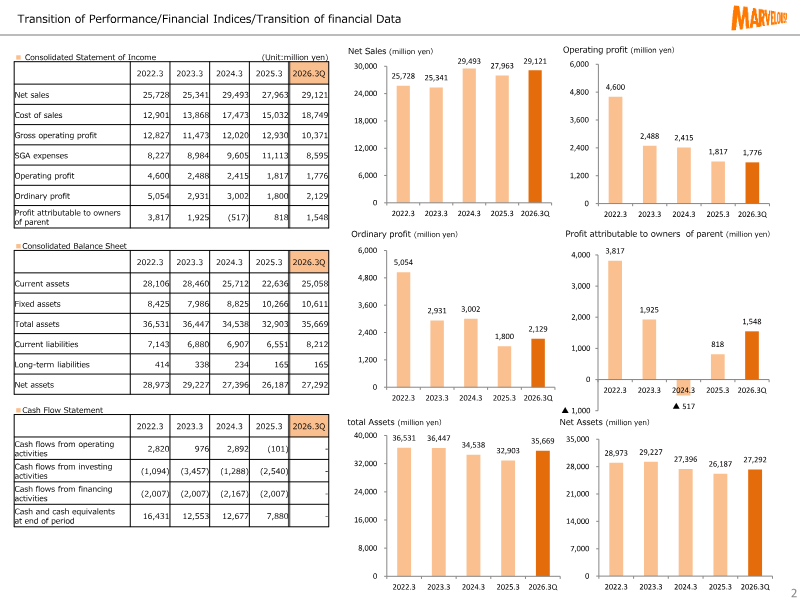

Marvelous Inc., listed on Tokyo’s Prime Market, released its third‑quarter financial results for the fiscal year ending March 31 2026. The company’s core business spans digital content, amusement, audio‑visual production and live entertainment, with a focus on original IPs and collaborations. Revenue rose to ¥29.1 billion in Q3, up 4.5% from the prior quarter and 10.6% year‑on‑year, driven primarily by digital content sales of ¥7.2 billion and amusement revenue of ¥3.0 billion. Gross operating profit reached ¥10.4 billion, a 12% increase over Q2 and a 9% rise versus the same period last year, reflecting improved cost control in production and marketing. Operating profit fell to ¥1.8 billion, a 12% decline from Q2, largely due to higher selling‑general‑administrative expenses of ¥8.6 billion compared with ¥7.9 billion in Q2. Net income attributable to shareholders was ¥1.5 billion, down 18% from Q2, with a net profit margin of 5.3%. The company’s cash‑flow position remained solid, with operating cash flow of ¥2.8 billion and a cash‑equivalent balance of ¥16.4 billion at quarter end. Geographically, the report covers Japan and overseas markets where Marvelous operates. The data derive from consolidated financial statements prepared under Japanese GAAP, covering all subsidiaries and affiliates. Key metrics such as return on equity (13.7%) and asset turnover (0.82) indicate healthy profitability, while dividend payout remained at 52% of net income. Overall, the quarter shows revenue growth but margin pressure from higher operating costs, prompting management to focus on cost efficiency and portfolio diversification.

Marvelous

Report

Financial Results Briefing Session of Fiscal Year Ended December 31, 2025 [17,284KB]

GungHo Online Entertainment’s FY 2025 financial briefing outlines a strategic pivot from Japan‑centric mobile development toward global expansion, emphasizing action titles on consoles and PCs. The company reports a 64.1 % overseas net‑sales ratio in FY 2025, up from 47.7 % in 2019 and 56.2 % in 2020, reflecting intensified sales in North America and Europe through new releases such as “Let It Die: Inferno” on PlayStation 5, Steam, and Nintendo Switch. The launch of nine global titles in 2025, including the “Ragnarok” series and “Puzzle & Dragons,” is highlighted as a key growth driver, with the latter celebrating its 5 000‑day anniversary and hosting cross‑platform events to boost user activity. Financially, consolidated net sales fell by 1.3 % YoY to ¥125.3 billion, driven mainly by declines in mobile titles and “Ragnarok”‑related revenue under subsidiary Gravity. Operating profit contracted by 9.3 % YoY to ¥276 million, as SG&A expenses rose due to increased advertising spend and personnel costs following the full acquisition of Alim in December 2024. Non‑consolidated results remained flat, but mobile sales slipped and Gravity’s “Ragnarok” titles underperformed, contributing to the consolidated loss. The briefing covers a global geographic scope—North America, Europe, Latin America, and Asia—with a 2025 focus on launching titles in over 150 countries. Methodologically, data derive from consolidated financial statements and quarterly performance metrics, with a clear emphasis on aligning product development with international market demand.

GungHo Online Entertainment