Skip to main content

Game Industry

Library

Library

Search

Ask AI

News

Connect your AI

Browse

The Catch Up

Topics

Collections

Writers

Help

Subscribe

Game Industry

Library

Library

Search

Ask AI

Saved

Country Reports | Game Industry Library

Collections

Country Reports

Back to Collections

Country Reports

Reports in the Country Reports category.

42 documents

Reports

Presentations

Whitepapers

Articles

Financial

Legal

Other

Recently added

Newest first

Oldest first

Title A–Z

Title Z–A

Report

19 pages

What Does the Monetization Landscape Look Like for Video Games in MENA?

The MENA-3 gaming market (KSA, UAE, Egypt) generated $2 billion in player spending in 2024 and is projected to grow to over $2.7 billion by 2028.

Payment infrastructure is a major barrier, as 67% of the regional population lacks access to traditional credit or debit cards, necessitating the integration of local payment networks like Mada in Saudi Arabia and Fawry in Egypt.

Direct-to-consumer (D2C) web shops are essential for bypassing 30% app store fees, with 53% of paying gamers in the region already utilizing official game websites for purchases.

Monetization

Market Analysis

Player Demographics

+1

Xsolla & Niko Partners

Jan 2025

Report

37 pages

Japan Market Report 2025

Japan generates 9.1% of global games revenue from only 2.2% of the global player base, with an average revenue per user of $223 compared to $145 in the UK.

International stakeholders have a $2.5 to $3.0 billion market opportunity when excluding mobile and Nintendo platforms, which currently command 70% of console hardware dominance.

Japanese gamers prioritize narrative depth, character design, and solo play, contrasting with Western preferences for open worlds, high-end graphics, and competitive multiplayer.

Market Analysis

Player Demographics

Player Behavior

+1

UKIE – UK Interactive Entertainment

Jan 2025

Report

29 pages

Mobile Game Market Insights: India 2025

India is the world's largest mobile gaming market by volume, recording 8.45 billion downloads in the 2024-25 fiscal year.

Despite high download volume, in-app purchase revenue is limited to $400 million, though it is growing at 8.5% year-over-year due to increased digital payment adoption and high-value iOS spenders.

Revenue is heavily concentrated in core competitive genres, with Battle Royale titles like Garena Free Fire and Battlegrounds Mobile India accounting for 50% of total market earnings.

Market Analysis

Monetization

India

+1

Sensor Tower

Jan 2025

Report

22 pages

Mobile App Trends Spotlight Edition: Türkiye 2025

The Turkish mobile app market is projected to reach $1.65 billion in revenue by 2029, supported by an 87% internet penetration rate and a global top-ten ranking for downloads and time spent in-app.

Generative AI applications experienced a 142.5% surge in downloads between 2023 and 2024, driven by local hyper-casual studios pivoting to AI-first development and proprietary Turkish-language models.

Finance app installs grew by 30% in the first half of 2025, bolstered by an 85% mobile banking adoption rate and retention rates that consistently outperform global medians.

Market Analysis

Player Behavior

Monetization

+2

Adjust

Jan 2025

Report

7 pages

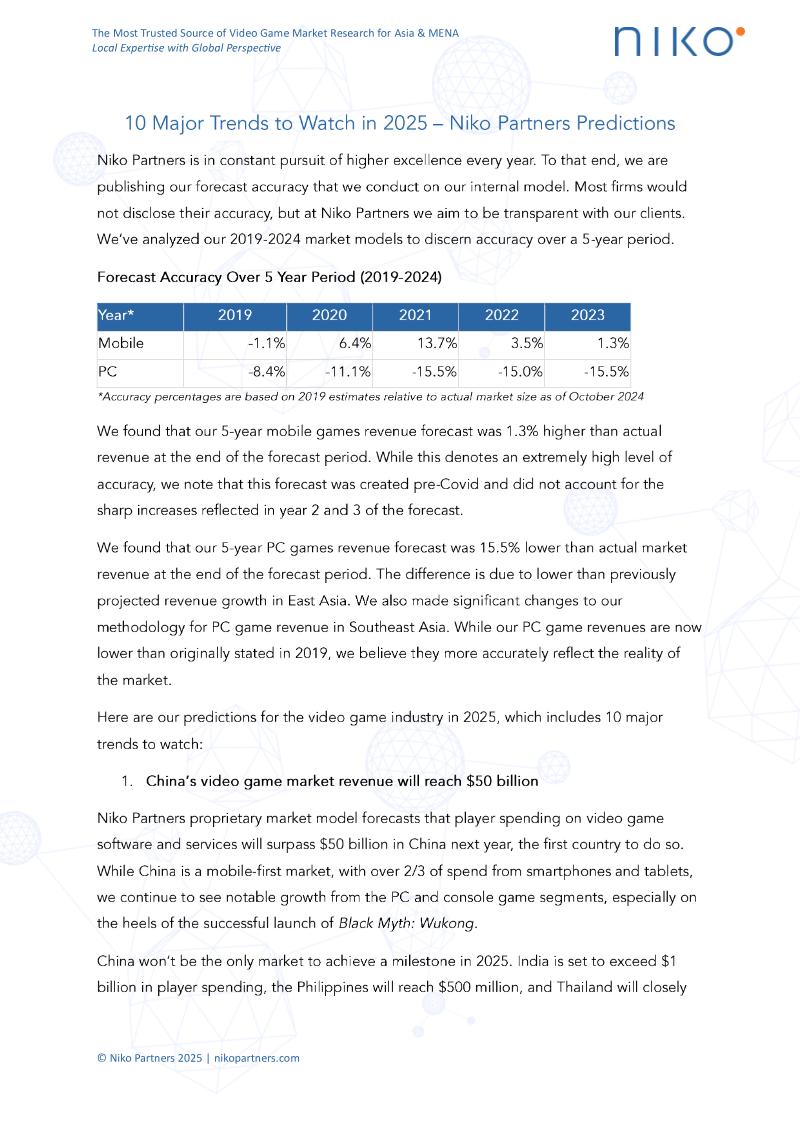

10 Major Trends to Watch in Asia & MENA

Asia and MENA are the primary engines of global gaming growth, driven by a mobile-first audience and a rising middle class with increased discretionary income.

Government-backed investments in Saudi Arabia and the UAE are rapidly establishing these nations as central hubs for international esports and game development infrastructure.

Market success in these regions now requires hyper-localization and the adoption of innovative payment ecosystems that bypass traditional storefront limitations.

Market Analysis

Player Demographics

Asia

+2

Niko Partners

Jan 2025

Report

72 pages

Africa Games Industry Report 2025

The African games industry is projected to exceed $1 billion in revenue in 2024, driven by a mobile-first market that generates nearly 90% of total sector earnings.

Nigeria has shown the most significant momentum in the region, with mobile revenues increasing fivefold since 2019, while South Africa remains the most lucrative individual market.

The developer ecosystem has grown to approximately 250 studios by 2024, with West Africa emerging as the primary hub after a fivefold increase in active studios over the past year.

Market Analysis

Market Forecast

Africa

Maliyo Games

Jan 2025

Report

15 pages

Levelling Up: State of India Interactive Media & Gaming Research FY'24

The Indian interactive media and gaming market reached a $3.8 billion valuation in FY24 and is projected to grow at a 20% CAGR to exceed $9.2 billion by FY29.

In-app purchase revenue grew 41% year-on-year, with the midcore segment serving as a primary growth driver after experiencing a 53% increase.

India’s gaming population has reached 590 million, including 148 million paying users who now spend an average of 13 hours per week gaming, a 30% increase from previous metrics.

Market Analysis

Market Forecast

Monetization

+1

Lumikai

Nov 2024

Report

53 pages

Mobile App Trends 2024: Japan Edition

The Japanese mobile market generated $17.9 billion in consumer spending in 2023, with Q1 2024 showing a 3.5% increase in spending and a 3% rise in downloads.

Mobile gaming remains the primary revenue driver, with RPGs capturing nearly 50% of consumer spend and simulation games achieving session lengths exceeding 40 minutes.

Finance apps experienced a 53.5% surge in spending in early 2024, while e-commerce apps reached a first-month lifetime value of $9.67, nearly double the global median.

Market Analysis

Player Behavior

Mobile

+1

Sensor Tower

Mar 2024

Report

292 pages

Reinvent India's Media & Entertainment Sector Is Innovating for the Future

The Indian media and entertainment sector reached a valuation of INR2.32 trillion in 2023 and is projected to exceed INR3 trillion by 2026, growing at a 10% CAGR.

Digital media is expected to overtake television as the dominant industry segment by 2024, supported by a projected expansion to nearly one billion active screens by 2030.

Online gaming has become the fourth-largest segment, surpassing filmed entertainment despite the implementation of a 28% GST mandate.

Market Analysis

Market Forecast

India

+1

Ernst & Young

Mar 2024

Report

40 pages

European Key Facts 2024: Video Games

The European video games industry generated €26.8 billion in 2024, with digital channels accounting for 90% of total sales.

The sector supports 116,000 professionals across 6,000 studios and serves 127 million players, representing 54% of the European population.

Mobile gaming is the primary platform in the region, utilized by 71% of the total player base.

Market Analysis

Player Demographics

Employment

+1

Video Games Europe

Mar 2024

Report

13 pages

FY2024 Report: Australian Game Development Survey

The Australian game development industry generated $339.1 million in revenue during FY2024, reflecting a minor 1.9% year-over-year decline despite global economic headwinds.

The sector is highly export-focused, with 93% of total revenue derived from international markets and 85% of studios prioritizing the development of original intellectual property.

Employment remains stable at 2,465 full-time equivalent workers, with 61% of studios planning to increase their headcount in the coming year.

Market Analysis

Employment

Funding

+1

Interactive Games & Entertainment Association

Jan 2024

Report

4 pages

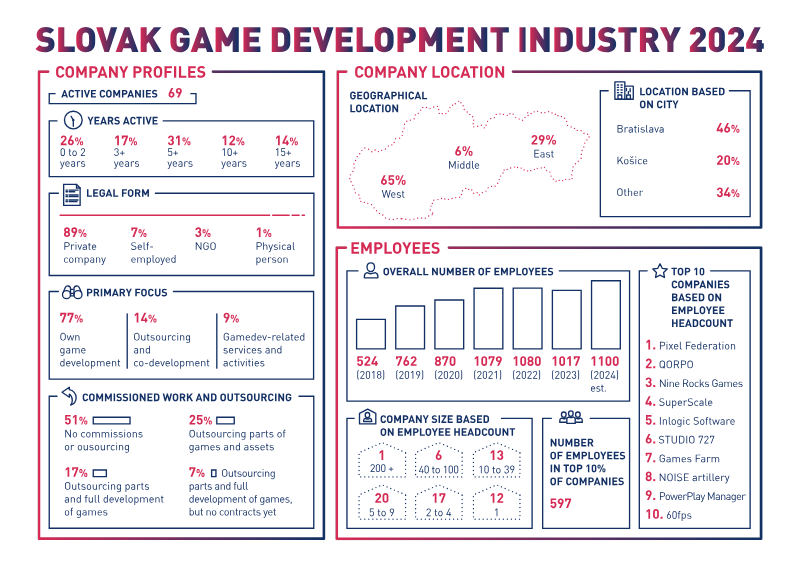

Company Profiles: Slovakia 2024

The Slovak game industry is highly concentrated, with the top 10% of companies—including Pixel Federation and Nine Rocks Games—generating 83.5% of the sector's 70 million EUR annual turnover.

The industry consists of 69 active companies, 77% of which focus on original game development rather than outsourcing services.

After a slight contraction in 2023, the workforce is projected to reach approximately 1,100 employees by the end of 2024, with a median age of 31 and 21% female representation.

Market Analysis

Employment

Game Development

+1

Swiss Game Developers Association

Jan 2024

Previous

1

2

3

4

Next