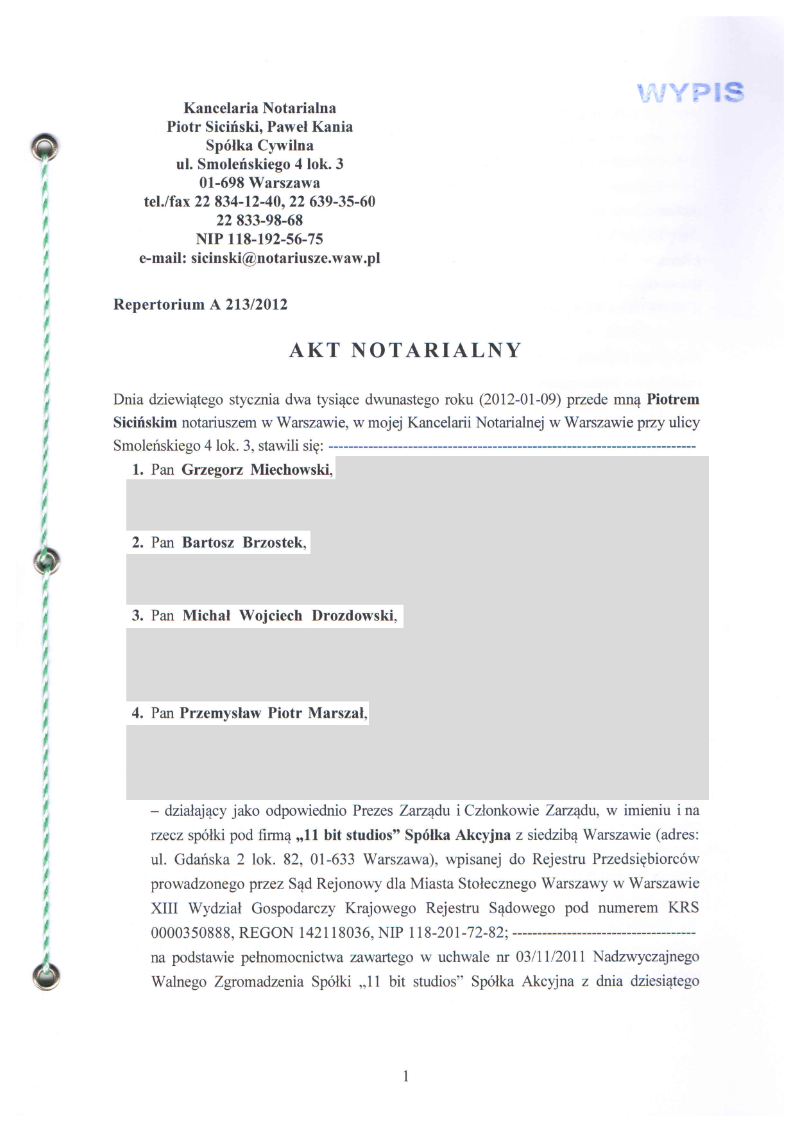

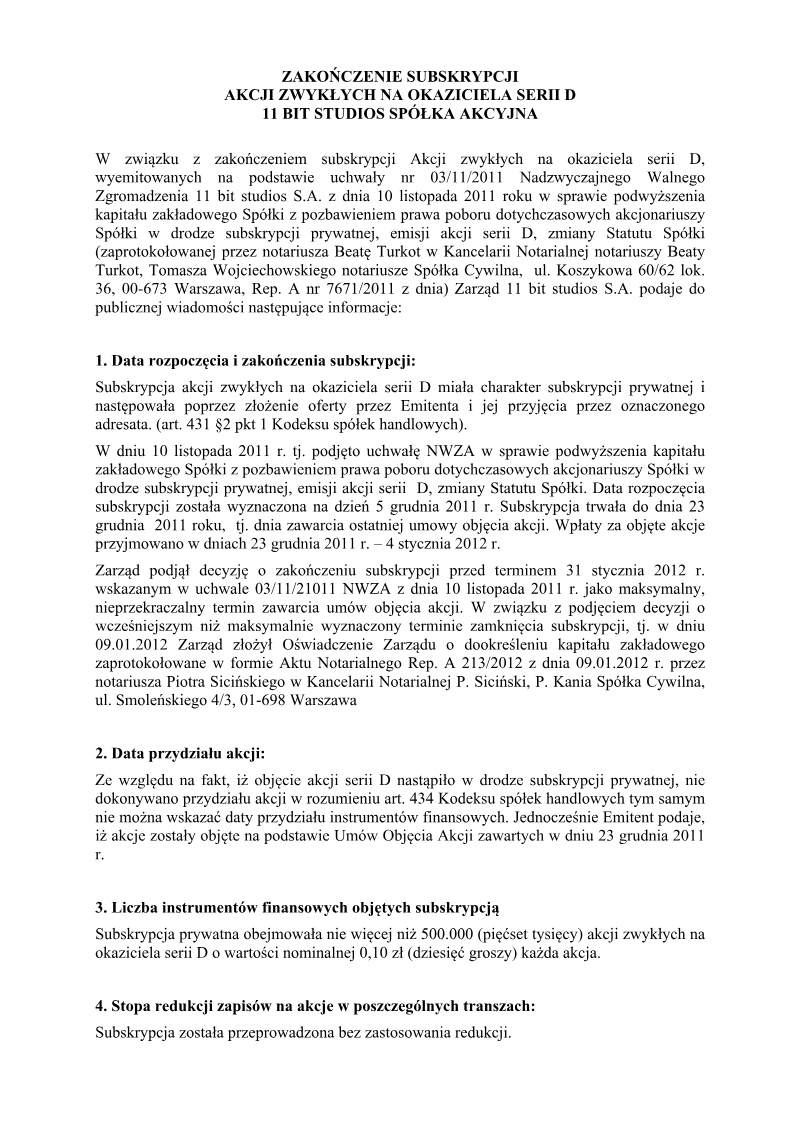

The notarized act dated January 9, 2012 records the formal approval by 11 Bit Studios’ board—Grzegorz Miechowski, Bartosz Brzostek, Przemysław Marszal, and Michał Drozdowski—of a capital increase for the Warsaw‑based public limited company. The board, empowered by Extraordinary General Meeting resolutions of November 10, 2011 (notary file A 7671/2011), authorized the issuance of up to 500,000 new ordinary shares (Series D) at a nominal value of PLN 0.10 each, raising the share capital from PLN 187,076.10 to a maximum of PLN 237,076.10. The resolution also amended the company’s statute to reflect a new share structure: 1,000,000 Series A shares, 494,200 Series B shares, 376,561 Series C shares, and up to 500,000 Series D shares.

By December 31, 2011 the board confirmed that 10 subscription agreements had been executed for a total of 40,938 Series D shares, amounting to PLN 4,093.80 in subscription proceeds. The act further specifies that the capital increase was fully paid in cash, with shares deposited into the company’s account before registration. It outlines provisions for voluntary share cancellation and issuance of utility certificates, as well as the allocation of costs: notarial fees, VAT at 23 %, and a civil‑law transaction tax.

The document is limited to Warsaw, Poland, covering the period from the November 2011 resolutions through the January 2012 notarization. It relies on statutory provisions under Polish commercial law (articles 431 §7, 310 §2, and related tax statutes) to validate the corporate actions. The act concludes with notarized signatures and fee details, confirming compliance with legal formalities for the capital increase.