ReportInvestGame

The Alumni Effect: Studios Founded by Ex-Activision, Blizzard, and King Employees

6 pages~3 min full read

The analysis examines venture capital activity directed toward studios founded by former Activision Blizzard employees between 2020 and 2024. It identifies 30 such startups that secured a total of approximately $0.7 billion across 45 VC‑led funding rounds, compared with 27 alumni studios from Riot Games that raised $0.5 billion in 38 rounds. Funding is concentrated in early‑stage rounds, with an average check size of $15.8 million for ex‑Activision studios versus $13.1 million for ex‑Riot ventures, and a notable skew toward PC & console and multiplatform projects. Web3 gaming represents a smaller share of the portfolio.

The study highlights a “first‑round momentum” effect: ex‑Activision studios are roughly twice as likely to secure a second round of financing within the same calendar year as other VC‑backed gaming startups. In 2021, 43 % of ex‑Activision studios raised a subsequent round versus only 9 % of peers; by 2023 the gap narrowed to 33 % versus 8 %. This pattern suggests stronger investor confidence in alumni teams during the 2021‑2022 peak.

Key investors include gaming‑focused funds such as GRIFFIN, PARTNERS COLLECTIVE, and SSSU, which together accounted for more than half of the capital deployed. Notable portfolio companies include Mythical Games (Series C, $262 million), Second Enap (Series B, $100 million), and TheoryCraft (Series A, $87.5 million). While many projects remain in development, releases such as Marvel Snap and Stormgate demonstrate commercial viability, whereas titles like Lightforge’s Project O.R.C.S. were shut down due to lack of traction.

Overall, the report underscores a robust investment climate for studios led by former Activision Blizzard talent, driven by early‑stage funding success and a higher likelihood of follow‑on rounds compared to broader gaming startup cohorts.

InvestGame · 2026

InvestGame · 2026

InvestGame · 2026

InvestGame · 2026

InvestGame · 2026

InvestGame · 2026

InvestGame · 2026

InvestGame · 2026

InvestGame · 2026

InvestGame · 2025

InvestGame · 2025

InvestGame · 2025

Drake Star · 2025

The Games Fund · 2025

Game Developer Collective · 2024

Konvoy · 2024

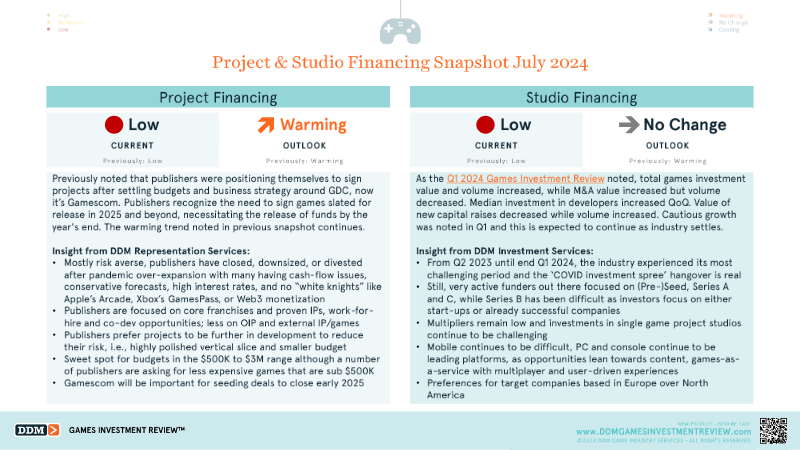

DDM · 2024

Konvoy · 2024

PitchBook · 2024

InvestGame · 2024

InvestGame · 2024

Konvoy · 2024

InvestGame · 2024

PitchBook · 2024