The analysis demonstrates that Sweden’s gaming sector has evolved into a $19 billion capital ecosystem, with 1,100 companies and 202 firms engaging in tracked transactions since 2014. Sweden contributes roughly 20 % of Steam’s projected 2025 gross revenue, and its developers produced five of the platform’s global top‑10 bestsellers in 2024–25. Capital flows have shifted from early‑stage seed rounds to late‑stage growth and acquisition deals, reflecting a maturation of the pipeline. Private investment rebounded in 2024 after a pullback; late‑stage rounds now dominate, with Aonic’s $157 million growth round and Arrowhead’s $80 million investment illustrating investor preference for studios with proven commercial traction. Early‑stage deal counts have normalized from 2021’s peak, indicating a steady but active pipeline.

M&A activity peaked in 2021–22, with ESL’s $1.05 billion sale to Savvy marking the cycle’s apex; subsequent deals have become more selective. Three transactions—King ($5.9 billion), Mojang ($2.5 billion), and ESL ($1.05 billion)—account for 93 % of total M&A value, underscoring the premium paid by global acquirers for Sweden’s IP and engineering talent. Public market activity has shifted from equity‑fueled growth to defensive debt financing; Embracer’s $4.4 billion raised through fixed income and PIPE in 2020–22 exemplifies this trend. Capital concentration is high, with the top ten private rounds comprising over $495 million of an $811 million total.

The data, sourced from InvestGame and market‑cap records through December 2025, cover Sweden’s entire gaming industry—mobile, PC & console, VR/AR, esports, and platforms—from 2014 to the present. Methodology includes tracking VC rounds, public offerings, PIPEs, and M&A transactions across all segments. The findings illustrate a resilient ecosystem that has transitioned from early‑stage bootstrapping to mature, high‑value capital flows driven by proven studios and strategic consolidation.

InvestGame · 2026

InvestGame · 2026

InvestGame · 2026

InvestGame · 2026

InvestGame · 2026

InvestGame · 2026

InvestGame · 2026

InvestGame · 2026

InvestGame · 2026

InvestGame · 2025

InvestGame · 2025

InvestGame · 2025

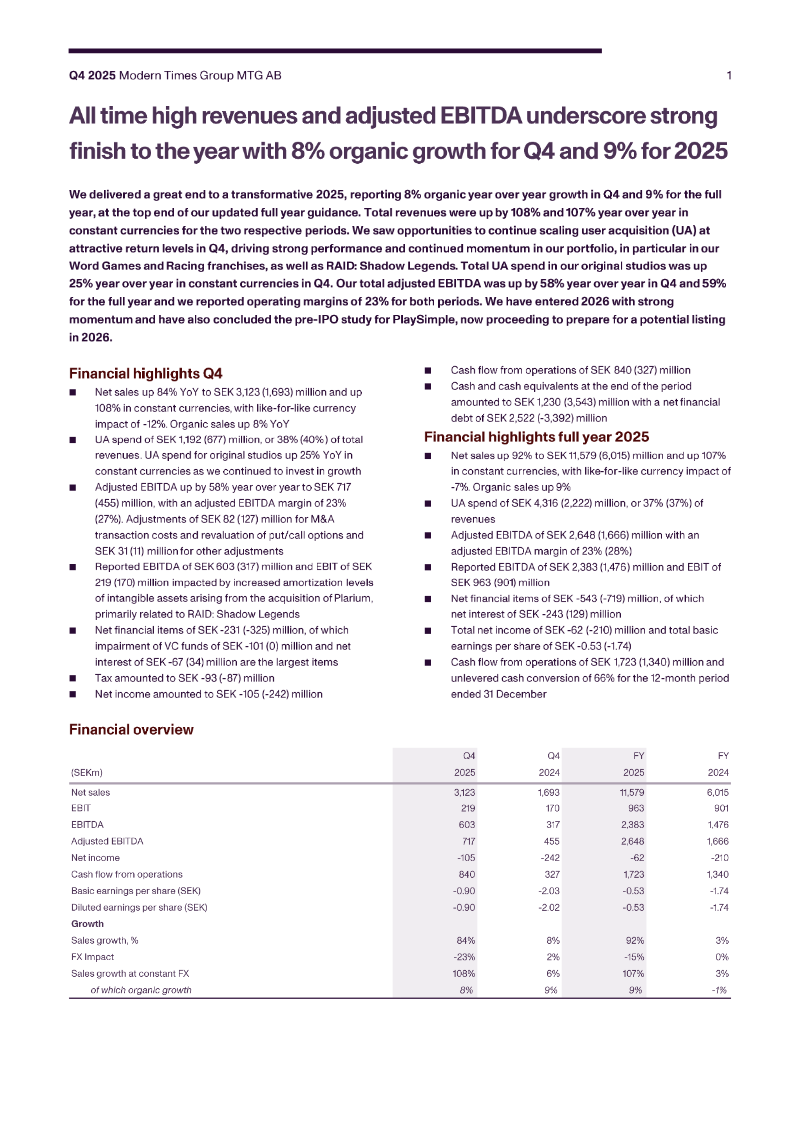

Modern Times Group · 2026

Direcció General d’Innovació i Cultura Digital · 2025

PCF Group · 2025

Departement Cultuur · 2025

PCF Group · 2025

Starbreeze · 2025

Polish Agency for Enterprise Development · 2025

AEVI · 2025

PCF Group · 2024

PCF Group · 2024

PCF Group · 2023

PCF Group · 2023