Skip to main content

Game Industry

Library

Library

Search

Ask AI

News

Connect your AI

Browse

The Catch Up

Topics

Collections

Writers

Help

Subscribe

Game Industry

Library

Library

Search

Ask AI

Saved

Library

223 reports matching your filters

All Types

Reports

Articles

Presentations

Whitepapers

Financial

Legal

Other

Search

Japan

Market Analysis

Investment

Mobile

Global

Game Publishing

Advertising

Monetization

Game Development

Console

Asia

Marketing

RPG

Player Behavior

Market Forecast

Mergers & Acquisitions

USA

South Korea

Clear

Filters

1

Japan

Recently added

Newest first

Oldest first

Title A–Z

Title Z–A

Report

2 pages

Summary of main supplementary explanations questions and answers at the FY2026 Second Quarter GREE Holdings, Inc. results briefing held on February 5, 2026

GREE Holdings revised its FY26 earnings downward due to recent performance softness in existing game titles.

The company is shifting its long-term strategy toward continuous growth businesses to reduce reliance on volatile game revenue, maintaining its medium-term targets for FY28.

GREE plans to acquire anime production capabilities through in-house development and M&A within the next 2–3 years to secure control over output quality and timing.

Monetization

Investment

Mobile

+1

GREE

Report

37 pages

Earnings Results: Q3 Fiscal Year Ending March 2026

For the nine-month period ending December 2025, consolidated net sales reached 202,991 million yen, representing a 1.7% decrease compared to the same period in the previous fiscal year.

Quarterly performance for the October–December 2025 period mirrored the nine-month trend, with net sales of 69,058 million yen, also reflecting a 1.7% year-over-year decline.

The absolute decline in net sales for the nine-month period amounted to 3,595 million yen compared to the 206,587 million yen recorded in the same period of the previous fiscal year.

Market Analysis

Investment

Japan

+1

Kadokawa Corporation

Report

21 pages

Results Briefing Materials: Fiscal Year Ending March 2026, First Half

Marvelous Inc. reported a 157.5% surge in net sales to ¥20,281 million for the first half of fiscal year 2026, driven by the release of three major titles and strong Pokémon-branded amusement machine sales.

Operating profit declined 38.2% to ¥226 million due to increased development costs, though net income rose 234.7% primarily due to foreign-exchange gains.

The Digital Contents Business segment saw revenue grow 198.7% to ¥12,414 million, while the Amusement Business grew 136.3% to ¥5,982 million, offsetting an 84.0% decline in the Audio & Visual Business.

Market Analysis

Game Publishing

Game Development

+2

Marvelous

Report

20 pages

Results Briefing Materials: Third Quarter Fiscal Year Ending March 31, 2026

Daemon Machina reported a 140.5% surge in net sales to ¥29,121 million for Q3 FY2026, driven by the release of three core titles and strong amusement-machine performance.

Operating profit grew by 6.1% to ¥1,776 million, as significant development costs partially offset the substantial revenue gains.

The Digital Contents segment saw a 169.2% increase in sales to ¥9,985 million, while the Amusement segment grew 125.1% to ¥7,435 million, bolstered by overseas Pokémon-branded machine sales.

Market Analysis

Game Publishing

Investment

+2

Marvelous

Report

4 pages

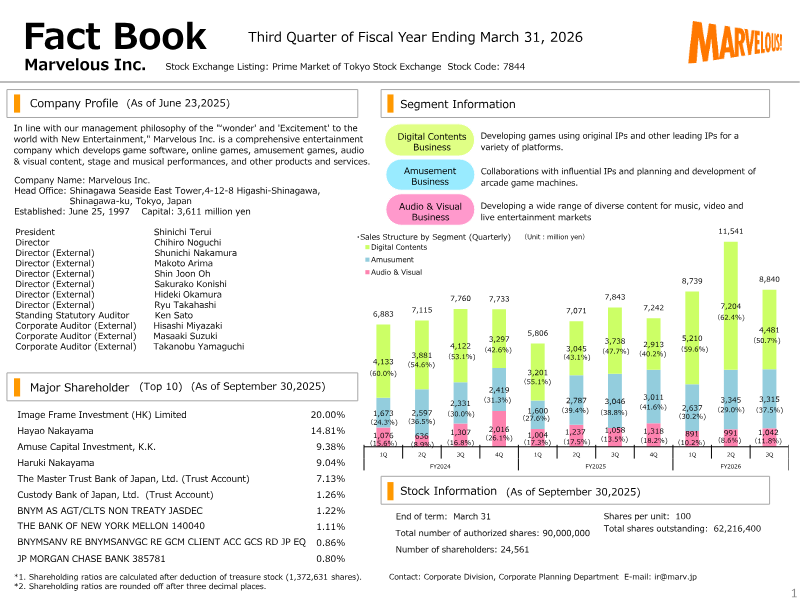

Factbook: Third Quarter of Fiscal Year Ending March 31, 2026

Marvelous Inc. reported Q3 revenue of ¥29.1 billion, representing a 10.6% year-on-year increase driven by digital content sales of ¥7.2 billion and amusement revenue of ¥3.0 billion.

Operating profit declined 12% quarter-on-quarter to ¥1.8 billion, primarily due to an increase in selling, general, and administrative expenses from ¥7.9 billion in Q2 to ¥8.6 billion.

Gross operating profit rose 9% year-on-year to ¥10.4 billion, reflecting improved cost control in production and marketing despite the overall pressure on net margins.

Market Analysis

Game Publishing

Game Development

+3

Marvelous

Report

80 pages

Integrated Report 2025

Sega Sammy Holdings is prioritizing the expansion of its intellectual property, highlighted by the strategic use of the Sonic the Hedgehog 3 movie as a core visual and growth driver for the 2025 fiscal period.

The group is focusing on the integration of non-financial capital to bolster its long-term corporate value and competitive positioning.

Management has identified specific materiality goals to align its business operations with sustainable growth objectives through 2025.

Game Publishing

Game Development

Mergers & Acquisitions

+2

Sega Sammy Holdings

Report

53 pages

Results Presentation: Q3 for the Fiscal Year Ending March 2026

The provided report for Q3 of the fiscal year ending March 2026 contains no specific performance data, financial figures, or operational metrics.

Management explicitly states that all forward-looking statements regarding market forecasts and performance outlooks are based on current judgment and do not guarantee future results.

The document serves as a disclaimer regarding the speculative nature of the company's strategic plans and outlooks.

Market Analysis

Market Forecast

Investment

+1

Sega Sammy Holdings

Report

13 pages

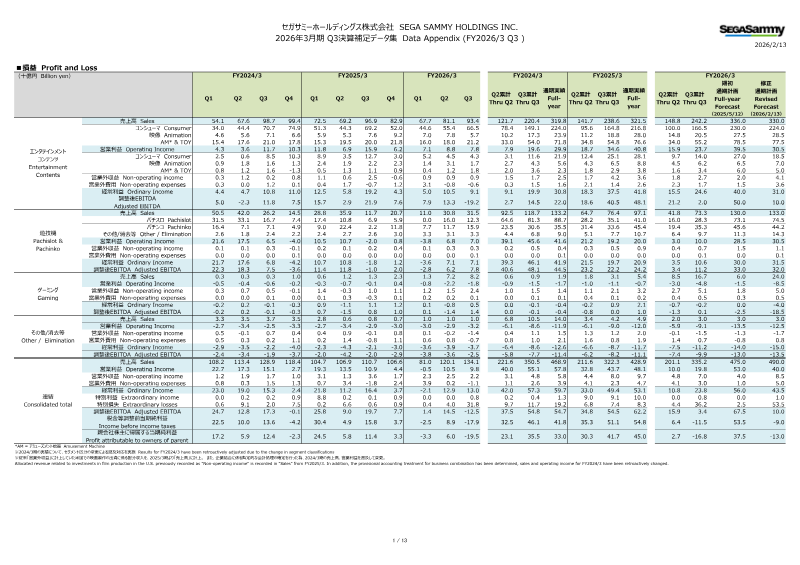

FY2026/3 Q3 Data Appendix

The provided report content contains only headers and structural placeholders, lacking the actual financial figures or performance data required to generate specific insights.

No revenue, profit, or growth metrics are present in the provided text to analyze the company's FY2026/3 Q3 performance.

The source material is limited to a document title and a table schema, providing no actionable business intelligence.

Market Analysis

Japan

Global

Sega Sammy Holdings

Report

64 pages

Annual Report 2005

The 2005 annual report categorizes business performance across five primary segments: offline games, online games, mobile phone content, publications, and other miscellaneous activities.

Financial data for the 2004 and 2005 fiscal years is structured to allow for direct year-over-year performance comparisons across all operational divisions.

The organization maintains a focus on environmental sustainability by utilizing recycled paper for the production of its 2005 annual report.

Market Analysis

Mobile

Console

+3

Square Enix

Report

70 pages

2004 Annual Report

Square Enix Co., Ltd. operated as a consolidated corporate group during the 2004 fiscal year.

The company's 2004 annual report includes both historical financial data and forward-looking statements regarding future performance.

Management strategies and business plans for the 2004 period were formally documented within the annual report.

Market Analysis

Investment

Japan

+1

Square Enix

Report

68 pages

Annual Report 2006

Offline games represented the largest segment of Square Enix's business in 2006, accounting for 36.9% of total net sales.

Online gaming operations contributed 12.6% of the company's total net sales for the 2006 fiscal year.

Mobile phone content accounted for 4.1% of Square Enix's total net sales in 2006.

Market Analysis

Game Publishing

Investment

+3

Square Enix

Report

64 pages

2012 Annual Report

Square Enix defines its corporate mission as the global delivery of high-quality content, services, and products to facilitate unforgettable consumer experiences.

The company's primary objective is to enable customers to discover individual definitions of happiness through the use of its entertainment offerings.

The organization operates under a unified corporate philosophy that prioritizes the creation of memorable experiences for its global user base.

Game Publishing

Global

Japan

Square Enix

Report

60 pages

2009 Annual Report

Square Enix Group defines its corporate mission as providing high-quality content, services, and products to facilitate unforgettable customer experiences.

The company’s stated objective is to spread happiness globally by enabling customers to define and discover their own unique experiences.

Investment

Global

Japan

+2

Square Enix

Report

1 pages

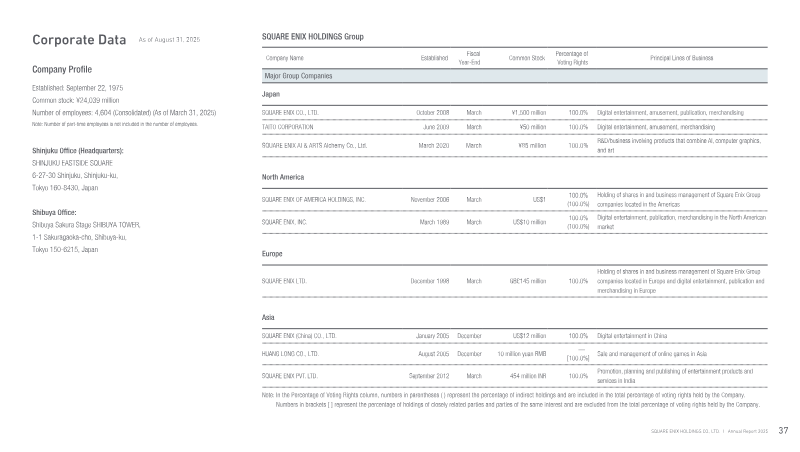

Corporate Data: August 2025

Square Enix Holdings Group maintains a unified global governance structure with 100% voting control over all international subsidiaries.

As of March 31, 2025, the parent company reports consolidated common stock of ¥24,039 million and a total workforce of 4,604 full-time employees.

Core operations are divided into digital entertainment, amusement, publication, and merchandising, supported by regional holding entities in North America, Europe, China, and India.

Game Publishing

Employment

Japan

Square Enix

Report

6 pages

Annual Report 2025: Review of Operations

Square Enix Group reported a 63.7% surge in profit attributable to owners to ¥24.4 billion for the fiscal year ending March 31, 2025, despite an 8.9% decline in net sales to ¥324.5 billion.

Operating income for the Digital Entertainment segment rose 33% to ¥33.9 billion, driven by reduced amortization and advertising costs in the HD Game sub-segment and the launch of 'FINAL FANTASY XIV: Dawntrail' in the MMO sub-segment.

Digital Entertainment net sales fell 16.8% to ¥206.5 billion, impacted by lower sales from new HD titles and weaker performance in the Games for Smart Devices/PC Browser category.

Market Analysis

Investment

Game Publishing

+2

Square Enix

Report

1 pages

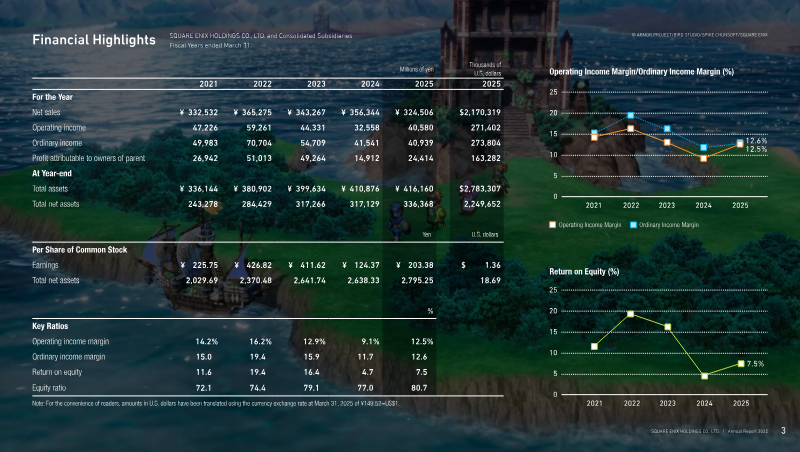

Financial Highlights: Fiscal Years Ended March 31

Square Enix experienced significant earnings volatility between 2021 and 2025, with net sales peaking at ¥365.3 billion in 2022 before falling to ¥324.5 billion in 2025.

Operating income declined sharply from a 2022 peak of ¥59.3 billion to ¥32.6 billion in 2024, with a projected recovery to ¥40.6 billion in 2025.

Profit attributable to owners of the parent dropped significantly from its 2022 high of ¥51.0 billion to a projected ¥24.4 billion for the 2025 fiscal year.

Market Analysis

Investment

Japan

+1

Square Enix

Report

72 pages

Annual Report 2010: Bandai Namco Holdings Inc.

Bandai Namco Holdings Inc. operates as a diversified entertainment conglomerate spanning toys, video games, arcade hardware, visual media, and music.

The company manages and operates physical amusement facilities as a core component of its business model.

The group's primary corporate objective is to achieve status as a 'Globally Recognized Entertainment Group.'

Market Analysis

Game Publishing

Investment

+2

Bandai Namco

Report

92 pages

Integrated Report 2017

BANDAI NAMCO operates as a diversified entertainment conglomerate spanning toys, network content, home video games, arcade games, amusement facilities, and visual and music content.

The company’s core business strategy is centered on the development and global distribution of entertainment products and services.

Game Publishing

Market Analysis

Global

+2

Bandai Namco

Report

100 pages

Integrated Report 2018

The Group launched a new Mid-term Plan in April 2018 focused on the strategic initiative titled 'CHANGE for the NEXT'.

The organization's core business segments include home video games, amusement machines, and amusement facilities.

The company's operational portfolio extends beyond gaming to include entertainment-related toys, network content, and visual and music content.

Global

Game Publishing

Mergers & Acquisitions

+3

Bandai Namco

Report

27 pages

Fact Book 2019

The Bandai Namco Group operates across diverse sectors including toys, hobby products, figures, capsule toys, card products, candy toys, and children's lifestyle sundries.

The report provides a comprehensive breakdown of consolidated business performance and key management indicators for the 2019 fiscal period.

Market data analysis covers specific performance metrics for the toy and hobby industry, including specialized segments like capsule toys and card products.

Market Analysis

Global

Japan

Bandai Namco

Previous

1

…

7

8

9

…

12

Next