ReportGREE

Summary of Main Supplementary Explanations Questions and Answers: FY2021 First Quarter GREE Results Briefing

2 pages~2 min full read

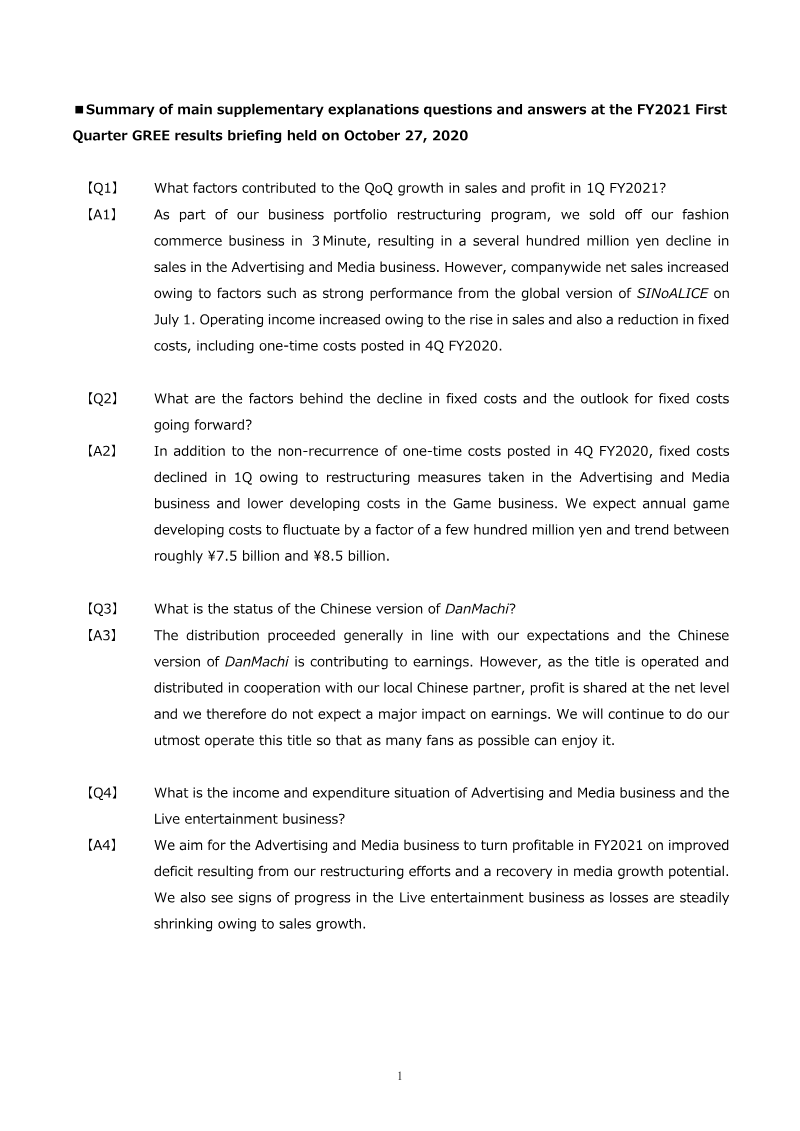

GREE achieved Q1 FY2021 growth in sales and operating income driven by the July 1 global launch of SINoALICE and a reduction in fixed costs.

See it on page 1Operating income for Q2 FY2021 is projected to remain stable between ¥0.5 billion and just under ¥1.0 billion as SINoALICE momentum slows and development spending increases.

See it on page 2Annual game development expenses are forecasted to range between ¥7.5 billion and ¥8.5 billion, with total fixed costs expected to fluctuate by a few hundred million yen.

See it on page 2The divestiture of the 3Minute fashion commerce unit reduced Advertising and Media sales by several hundred million yen, though the division is targeting overall profitability for FY2021.

See it on page 1The Chinese version of DanMachi is meeting performance expectations, though its contribution to total company profitability remains modest due to the net-level profit share model.

See it on page 1The Live Entertainment segment is showing improved financial health, characterized by a narrowing loss margin resulting from recent sales growth.

See it on page 1The briefing explains that first‑quarter FY2021 sales and operating income rose despite a divestiture of the 3Minute fashion commerce unit, which reduced Advertising and Media sales by several hundred million yen. Growth was driven mainly by the launch of SINoALICE’s global version on July 1, coupled with a reduction in fixed costs. One‑time expenses incurred in Q4 FY2020 were eliminated, and restructuring within Advertising and Media cut development costs for the Game business. Operating income is projected to remain stable in Q2 FY2021, with a forecasted range of ¥0.5 billion to just under ¥1.0 billion, reflecting a decline in SINoALICE momentum and an uptick in game development outlays.

Fixed‑cost trends are expected to fluctuate by a few hundred million yen annually, with game development expenses projected between ¥7.5 billion and ¥8.5 billion. The Chinese version of DanMachi is performing as anticipated, contributing to earnings through a net‑level profit share with the local partner; however, its impact on overall profitability is modest. The Advertising and Media division aims to achieve profitability in FY2021, while the Live Entertainment segment shows a narrowing loss margin due to sales growth.

Overall, the company’s restructuring and strategic releases have bolstered revenue and controlled costs, positioning it for steady profitability in the second quarter while maintaining a cautious outlook on development spending and partner‑shared titles.