Market Analysis

Report

2025 Q4 Earnings Report

The quarterly performance for the fourth quarter of 2025 shows a sharp decline in revenue and profitability, driven by a lack of new releases and reduced impact from major updates. Total sales fell 25.8 % YoY to 98.9 billion KRW, with mobile gaming contributing the largest drop (−38.7 %) and PC gaming partially offsetting losses through a 44.9 % YoY increase in the fourth quarter, though overall PC revenue remained down 29.8 % QoQ. Operating expenses decreased by 18.4 % YoY to 112.0 billion KRW, largely due to reductions in personnel costs and marketing spend; however, operating losses widened to −131 billion KRW (−13.2 % margin), the largest quarterly loss on record. Net income mirrored this trend, slipping to a −1,106 billion KRW loss (−111.8 % margin) after a brief turnaround in the third quarter that produced a 346 billion KRW profit. The company’s balance sheet shows a contraction in total assets to 2,676 billion KRW and a significant reduction in equity to 1,199 million KRW, reflecting accumulated losses. The outlook for the next fiscal year remains cautious; a pipeline of new titles slated for 2026 and beyond is highlighted, but current financials indicate continued operating deficits. The report relies on KIFRS‑compliant consolidated statements and acknowledges that audited results may differ once external audit is completed.

Kakao Games

Report

Financial Results for the Second Quarter Ending December 2025: Japan

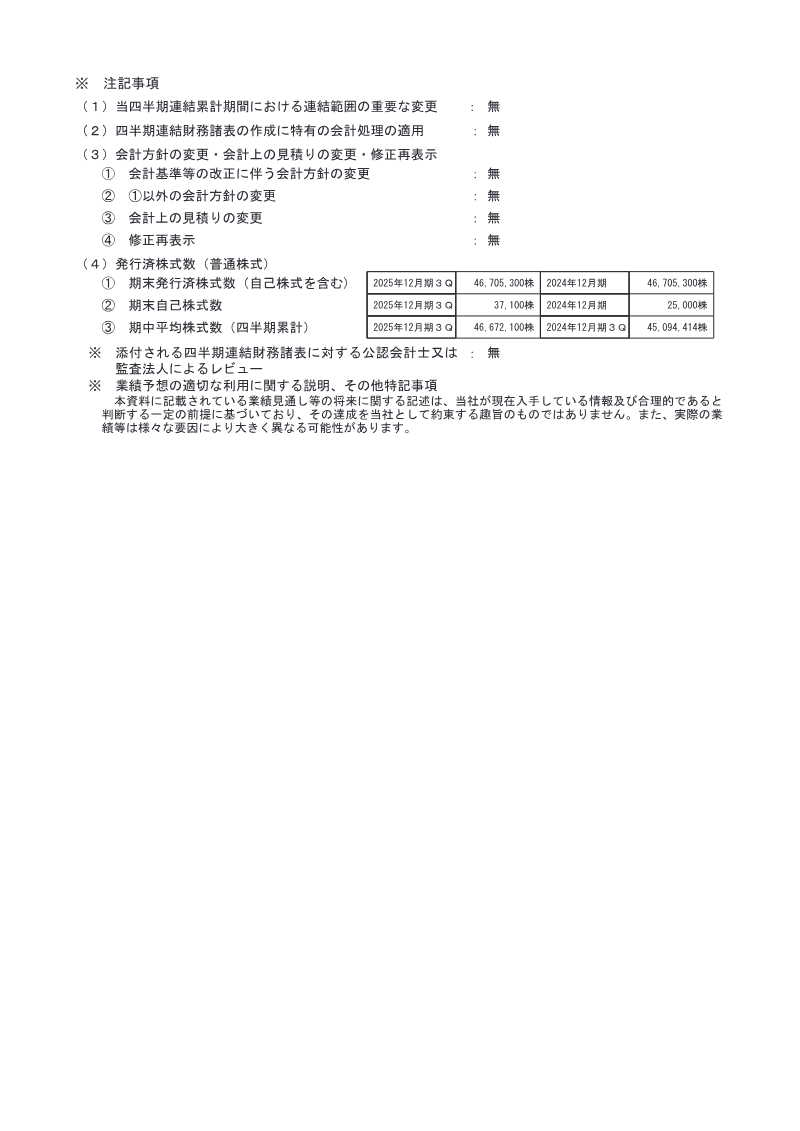

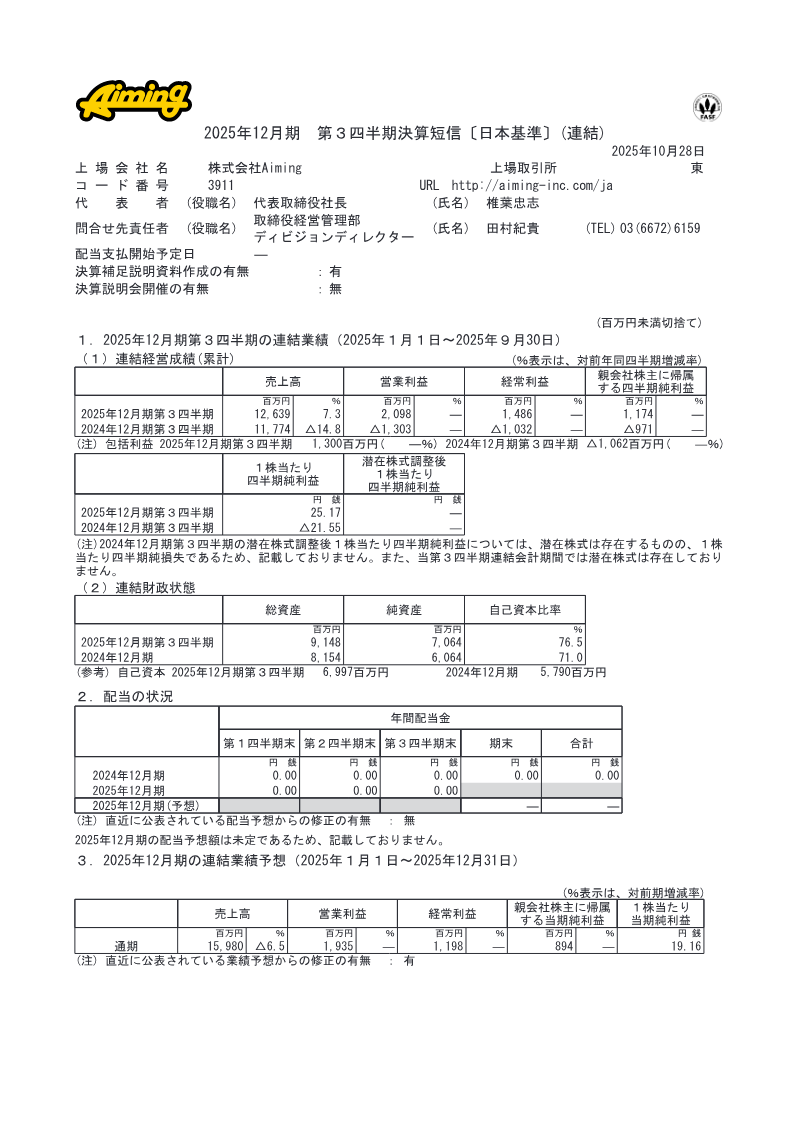

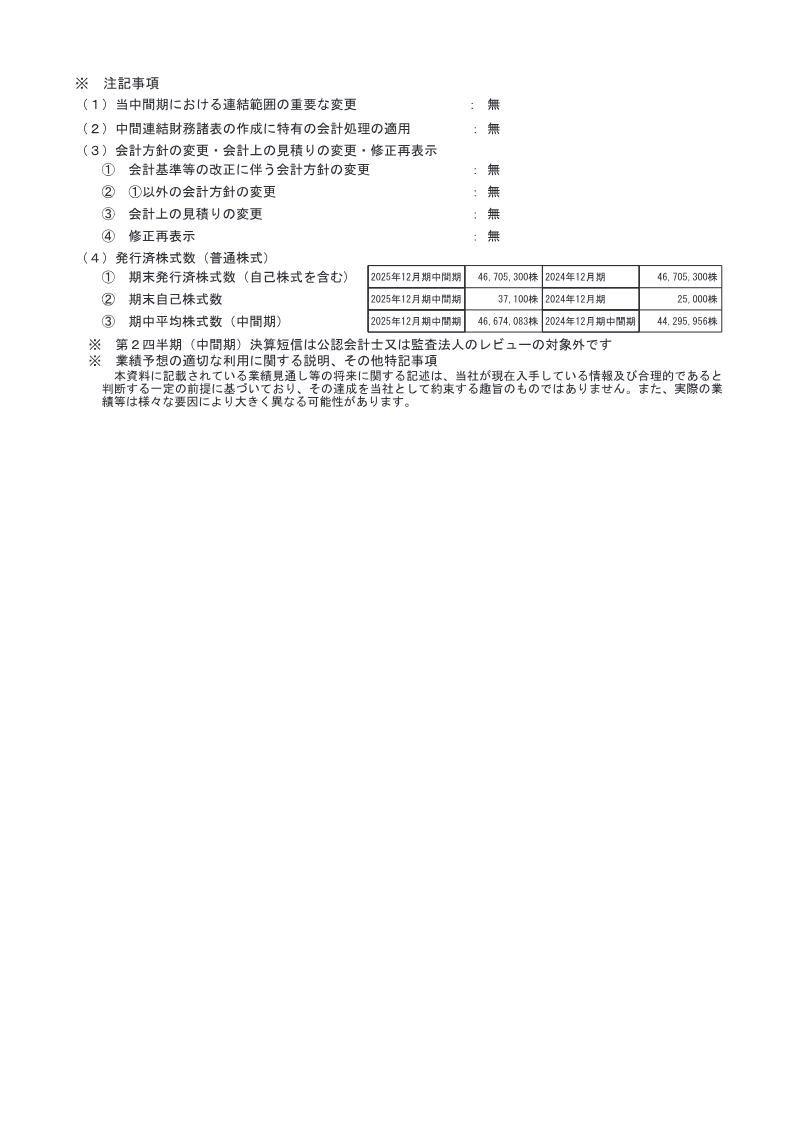

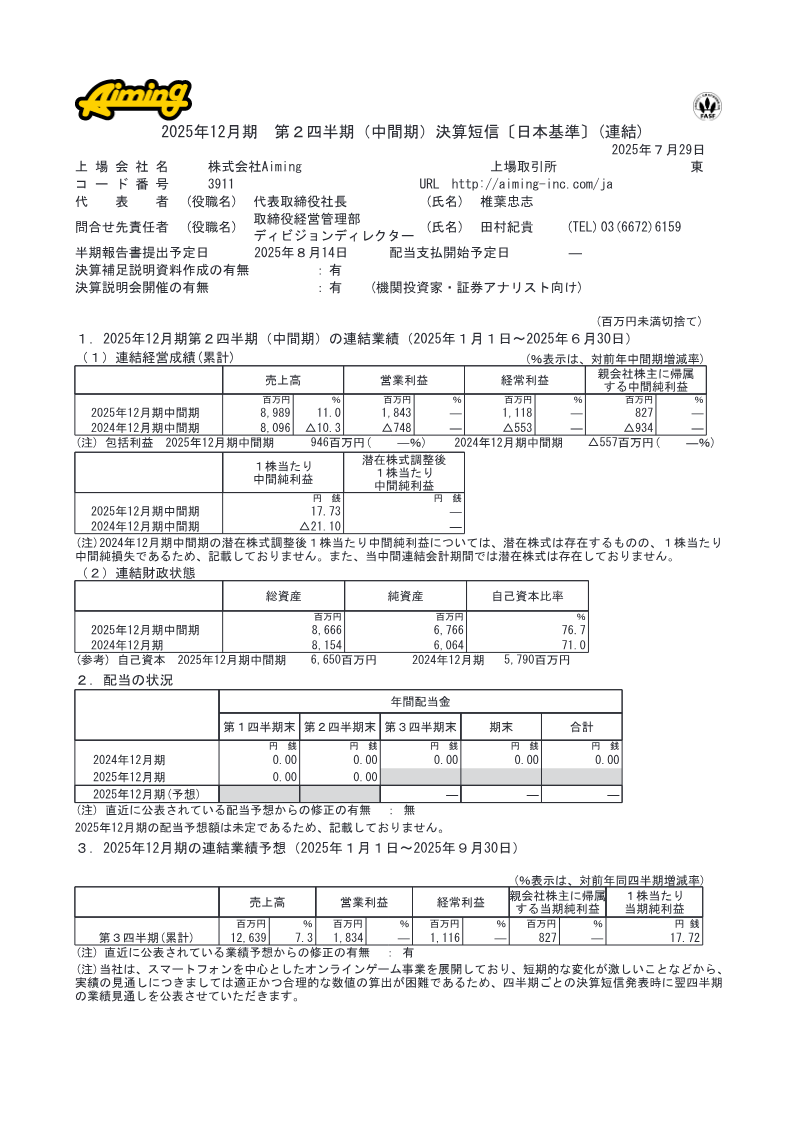

Aiming Inc. reported its second‑quarter results for the fiscal year ending December 2025, covering January 1 to June 30. Consolidated revenue rose 11.0 % year‑over‑year to ¥8,989 million, while operating profit improved from a loss of ¥748 million in the same period 2024 to a gain of ¥1,843 million. Ordinary profit increased from a loss of ¥553 million to ¥1,118 million, and net income attributable to parent shareholders grew from a loss of ¥934 million to a profit of ¥827 million. Earnings per share remained flat at ¥17.73, reflecting the absence of dilutive potential shares during this period. Total assets expanded to ¥8,667 million from ¥8,154 million, with shareholders’ equity rising to ¥6,766 million and the equity ratio climbing from 71.0 % to 76.7 %. Cash and cash equivalents increased markedly, while accounts receivable fell, indicating stronger liquidity management. The company’s only operating segment is online gaming, primarily on smartphones, and it noted that short‑term market volatility hampers precise forecasting. Dividend guidance for 2025 remains undetermined, and no dividends were declared in the first half. The company provided a third‑quarter outlook for the remainder of 2025, projecting cumulative revenue of ¥12,639 million and operating profit of ¥1,834 million. No material accounting policy changes or restatements were reported for the period. The results reflect a turnaround in profitability driven by higher gross margins and reduced operating expenses, positioning the firm for continued growth within its single‑segment online gaming market.

Aiming