Key insights

7 takeaways · ~3 min read- 01

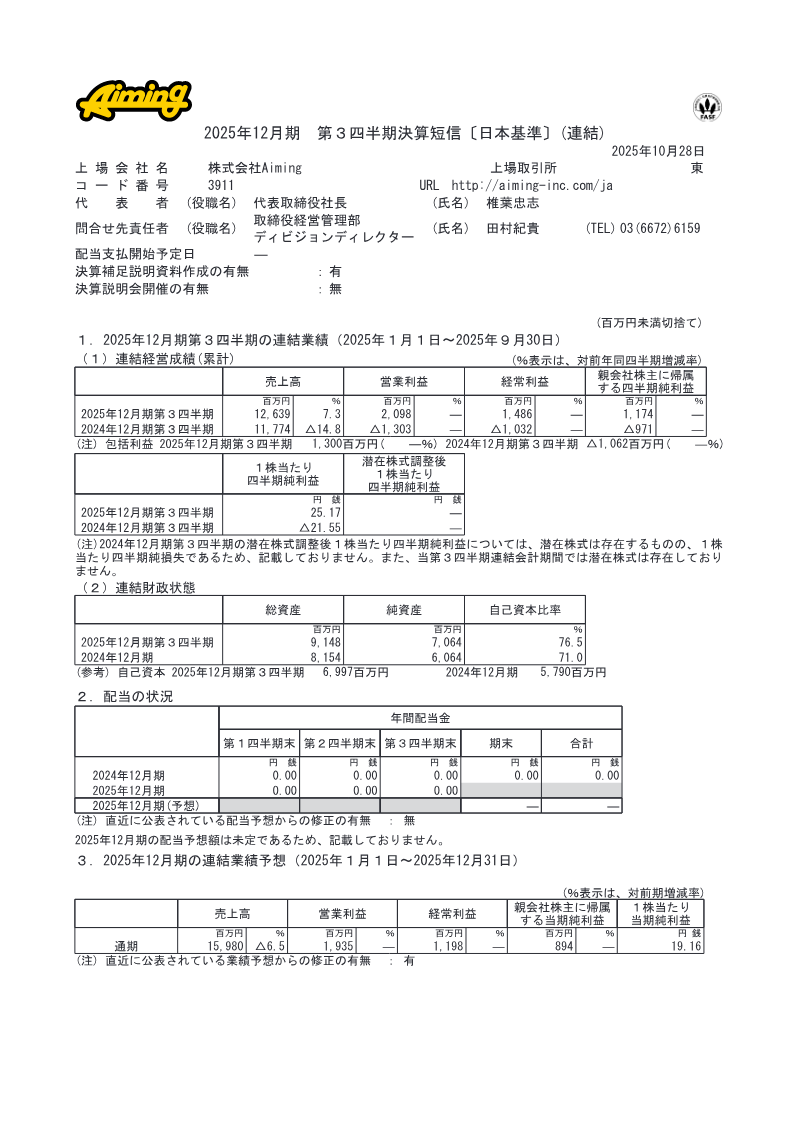

Aiming Inc. achieved a significant financial turnaround in Q3 2025, reporting a net profit of ¥1,174 million compared to a ¥971 million loss in the same period of 2024.

See it on page 1 - 02

Total revenue for Q3 2025 reached ¥12,639 million, representing a 7.3% year-over-year increase driven by the company's core online-game segment.

See it on page 4 - 03

Operating profit swung from a ¥1,303 million loss in Q3 2024 to a ¥2,098 million profit in Q3 2025, with earnings per share rising to ¥25.17.

See it on page 7 - 04

The company strengthened its balance sheet, increasing total assets to ¥9,148 million and net equity to ¥7,064 million as of September 30, 2025.

See it on page 6 - 05

Growth in the online gaming segment was supported by event-driven content and IP collaborations, most notably with Square Enix.

See it on page 4 - 06

Aiming Inc. forecasts full-year revenue of ¥15,980 million with a net profit margin of 1.9%.

See it on page 1 - 07

The dissolution of the “2.5次元の誘惑” joint-venture production committee on September 30, 2025, is expected to have a minimal impact on fiscal year results.

See it on page 10