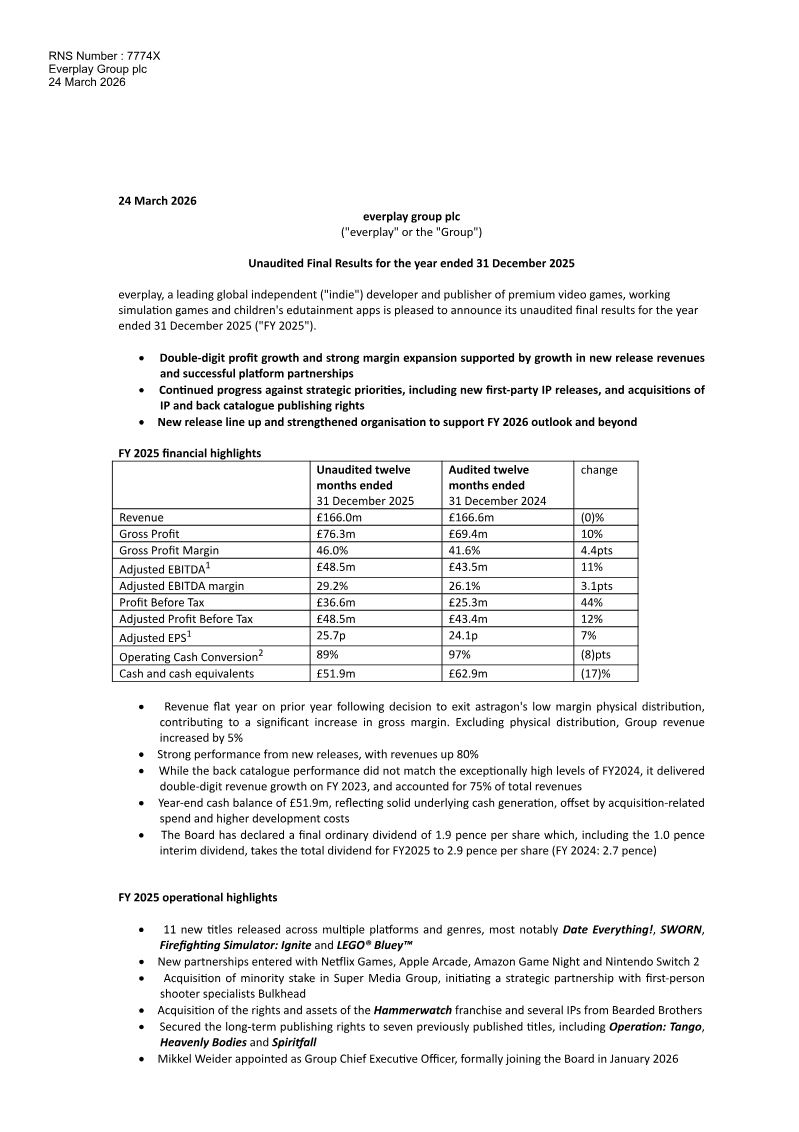

ReportModern Times Group

Annual Report 2019: Shaping the Future of Entertainment

103 pages~250 min full read

Key insights

5 takeaways · ~2 min read- 01

In March 2019, MTG underwent a corporate split, resulting in the formation of two separate entities: Nordic Entertainment and the new MTG.

See it on page 5 - 02

The 2019 Annual Report serves as the primary documentation for the company's segmental performance, financial policies, and risk management strategies following the corporate restructuring.

See it on page 24 - 03

Corporate responsibility and sustainability initiatives for the period are detailed in a separate MTG Corporate Responsibility Report published alongside the annual financial disclosures.

See it on page 2 - 04

The report provides a comprehensive overview of internal control systems and governance responsibilities for the newly formed organizational structure.

See it on page 43 - 05

Financial reporting for the 2019 fiscal year includes specific sections dedicated to alternative performance measures and other group-level information.

See it on page 48