FinancialCyberAgent

FY2024 Second Quarter Consolidated Financial Results: Japan

9 pages~16 min full read

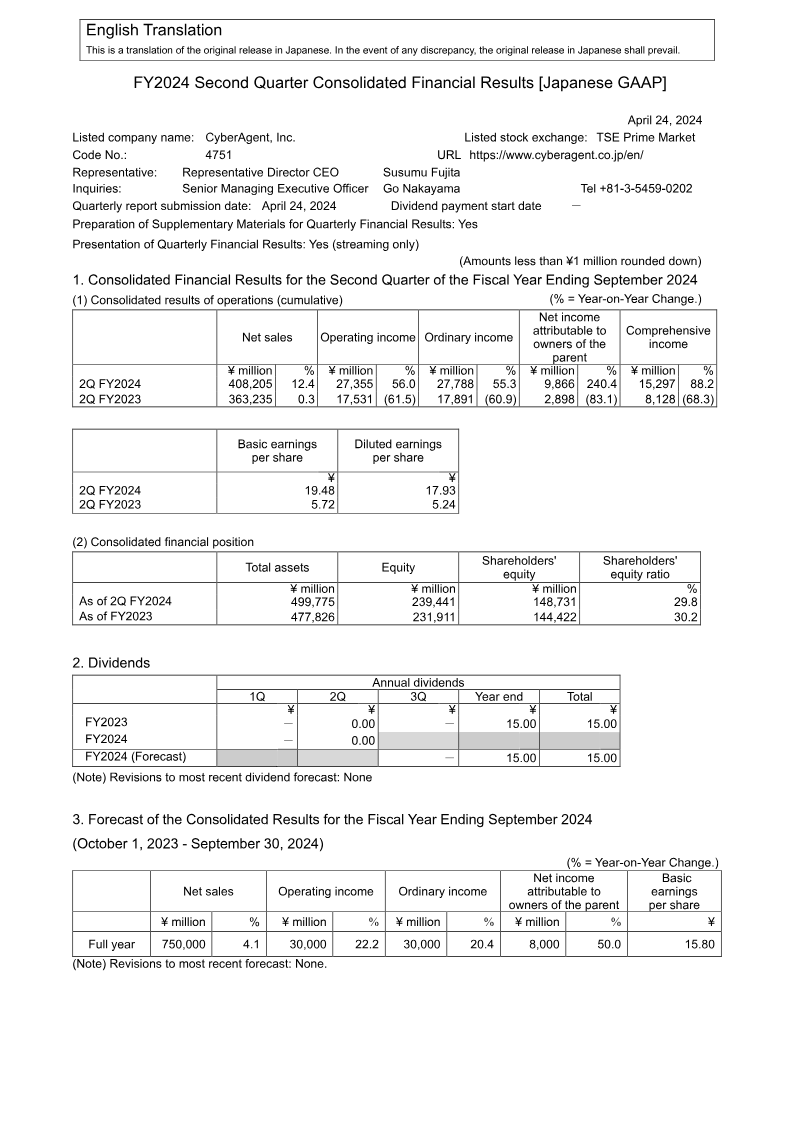

CyberAgent reported a significant surge in profitability for FY2024 Q2, with operating income rising 56% to ¥27,355 million and net income attributable to the parent jumping 240% to ¥9,866 million.

See it on page 1Net sales for the quarter increased by 12.4% to ¥408,205 million, supported by growth across all primary segments including media, internet advertising, and games.

See it on page 4The media segment, driven by ABEMA, saw the strongest growth with a 26.8% increase in sales to ¥84,880 million, while game sales rose 8.9% to ¥112,213 million and internet advertising grew 8.6% to ¥212,658 million.

See it on page 4Cash flow from operations improved significantly to a net inflow of ¥23,008 million, compared to ¥14,080 million in the same period of the prior year.

See it on page 4The company maintained its full-year FY2024 guidance, projecting ¥750 billion in net sales and ¥30 billion in operating income.

See it on page 1The investment development segment experienced a 27.6% decline in sales to ¥880 million, signaling a strategic shift away from venture activities.

See it on page 4Total assets reached ¥499,775 million, supported by an increase in cash and cash equivalents to ¥205,575 million.

See it on page 4CyberAgent’s FY2024 second‑quarter results show a robust 12.4 % rise in net sales to ¥408,205 million, driven by growth across its media, internet advertising, and game segments. Operating income surged 56 % to ¥27,355 million, while ordinary income climbed 55 % to ¥27,788 million. Net income attributable to the parent ballooned 240 % to ¥9,866 million, with earnings per share rising from ¥5.72 (basic) to ¥19.48 in the quarter.

Segment performance highlights include a 26.8 % increase in ABEMA‑related media sales to ¥84,880 million, an 8.6 % rise in internet advertising revenue to ¥212,658 million, and an 8.9 % rise in game sales to ¥112,213 million. The investment development segment recorded a 27.6 % decline in sales to ¥880 million, reflecting a shift away from venture activities.

Total assets grew by ¥21.9 billion to ¥499,775 million, with current assets expanding due to higher receivables and contract assets. Total liabilities increased by ¥14.4 billion, mainly from higher accounts payable and tax payables, while equity rose by ¥7.5 billion to ¥239,441 million. Cash and cash equivalents increased by ¥3.8 billion to ¥205,575 million.

Cash flow from operations improved markedly, providing ¥23,008 million in net inflow versus ¥14,080 million the prior year. Investing cash outflows were lower than in 2023, and financing activities shifted from a net inflow to a net outflow due largely to dividend payments.

The company maintains its FY2024 full‑year forecast of ¥750 billion in net sales and ¥30 billion in operating income, unchanged from the November 2023 guidance. No revisions to accounting policies or significant subsidiary changes were reported, and the forecast remains subject to market uncertainties.