The study demonstrates that the United Kingdom’s esports industry has experienced robust growth, expanding at an average annual rate of 8.5 % between 2016 and 2019. In 2019 alone, the sector generated approximately £60 million in revenue—about eight per cent of global esports earnings—and contributed £111.5 million to the national Gross Value Added, supporting more than 1,200 full‑time equivalent jobs. These figures underscore the sector’s role as a significant driver of the UK digital creative economy.

Key drivers identified include the proliferation of professional teams, high‑profile tournaments hosted by organisations such as ESL, Gfinity and Epic.LAN, and the rise of streaming platforms that have broadened audience reach. Dedicated venues like Belong Gaming Arenas further stimulate grassroots participation and local economic activity. Modelling of direct, indirect and induced effects reveals a total impact of roughly 216 FTEs and £19.5 million in GVA, while spill‑over benefits from event tourism—estimated at £234 k per 1,000 visitors and nearly five FTEs—highlight additional value for host communities.

The analysis projects that hosting a major global esports event could add 238 full‑time equivalents and £12 million in GVA to the UK economy, signalling substantial upside potential. The findings point to opportunities for further investment, clearer regulatory frameworks and strategic positioning to attract international events, thereby consolidating esports as a pivotal growth sector within the United Kingdom’s broader digital economy.

British Esports · 2025

Ukie · 2025

Ukie · 2025

Ukie · 2025

Newzoo · 2025

UKIE – UK Interactive Entertainment · 2025

Ukie · 2024

Nordicity · 2024

Ukie · 2024

Ukie · 2024

Ukie · 2023

Olsberg SPI · 2020

Newzoo · 2022

Niko Partners · 2026

Ocean Entertainment Group · 2026

GamesBeat · 2026

SpielFabrique · 2026

Deloitte · 2026

Decision Lab · 2026

Frontier Developments · 2026

InvestGame · 2025

Frontier Developments · 2025

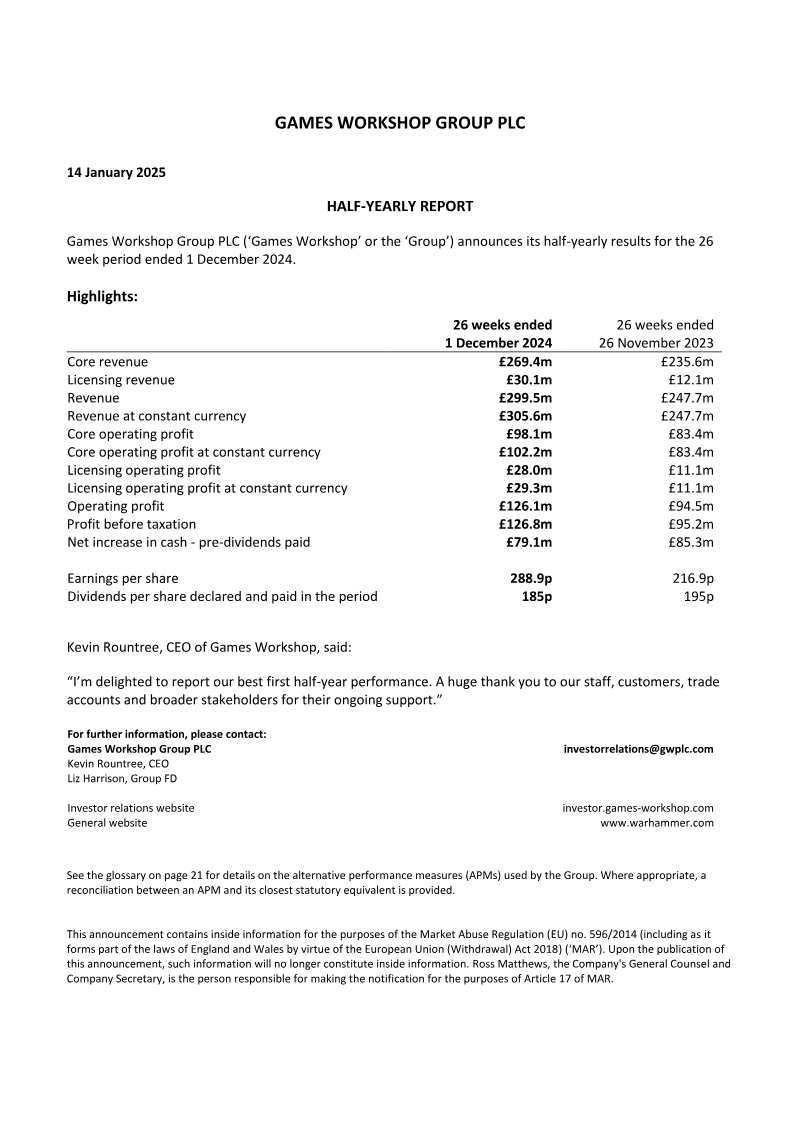

Games Workshop Group · 2025

Games Workshop Group · 2025