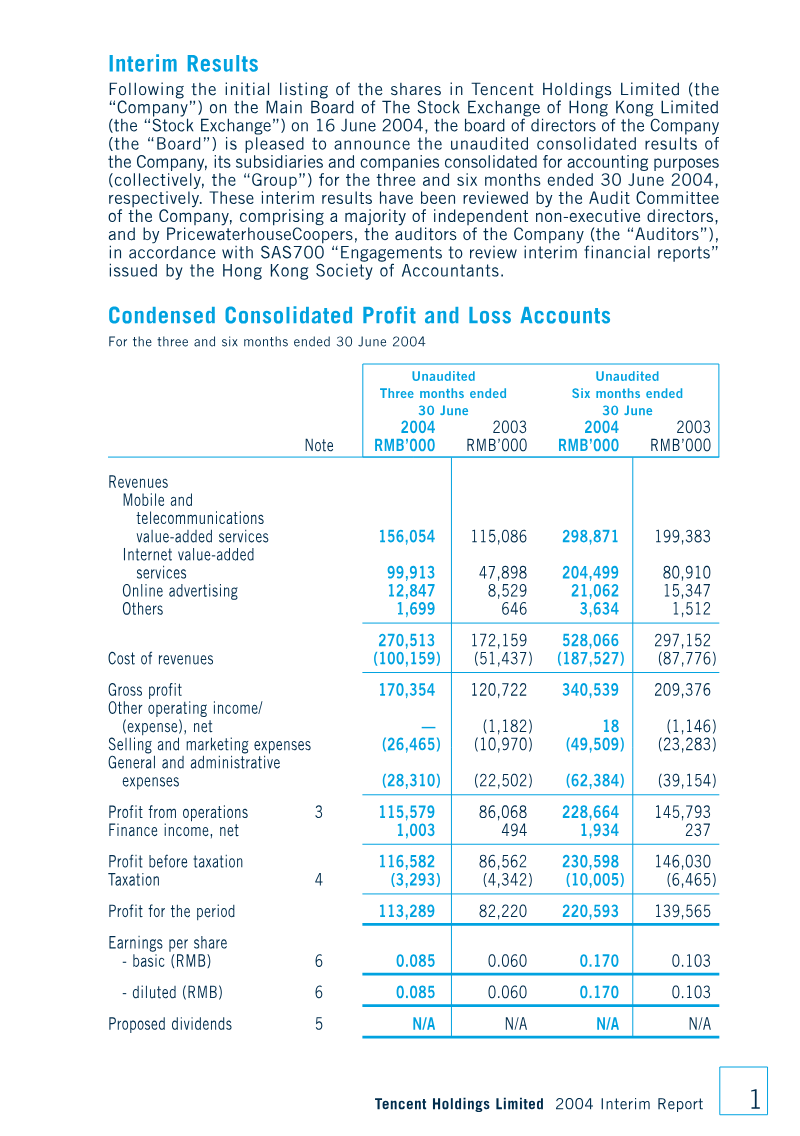

Tencent Holdings Limited experienced a period of rapid expansion during the first half of 2004, characterized by substantial revenue growth and a successful transition to a publicly traded entity. Total revenues for the six-month period ending June 30, 2004, reached RMB 528.1 million, representing a 77.7% increase over the previous year. This financial momentum was largely fueled by the robust performance of mobile, telecommunications, and internet value-added services, which remain the core pillars of the company’s business model. Profit for the period rose by 58.1% to RMB 220.6 million, reflecting a strong operational foundation despite rising costs associated with bandwidth, server capacity, and revenue-sharing agreements.

The company’s strategic position was significantly bolstered by its initial public offering on June 16, 2004, which raised RMB 1,656.7 million and resulted in cash and cash equivalents totaling RMB 1.95 billion by the end of the half-year. While the second quarter saw a slight contraction in certain internet value-added services due to the proactive removal of inactive user accounts, the overall growth trajectory remained positive. The company also demonstrated significant organizational scaling, more than doubling its workforce to 804 employees to support its expanding operations.

Looking ahead, management intends to leverage its strengthened capital position to drive further growth through the diversification of payment channels, the expansion of QQ-based value-added services, and the pursuit of strategic acquisitions. By maintaining a focus on corporate governance and operational efficiency, the company aims to sustain its market leadership within the Chinese internet and mobile services sectors. These results underscore a pivotal phase of institutional development, setting the stage for continued investment in infrastructure and service innovation.

Tencent · 2024

Tencent · 2024

Tencent · 2022

Tencent · 2021

Tencent

Tencent

Tencent

Tencent

Tencent

Tencent

Tencent

Tencent

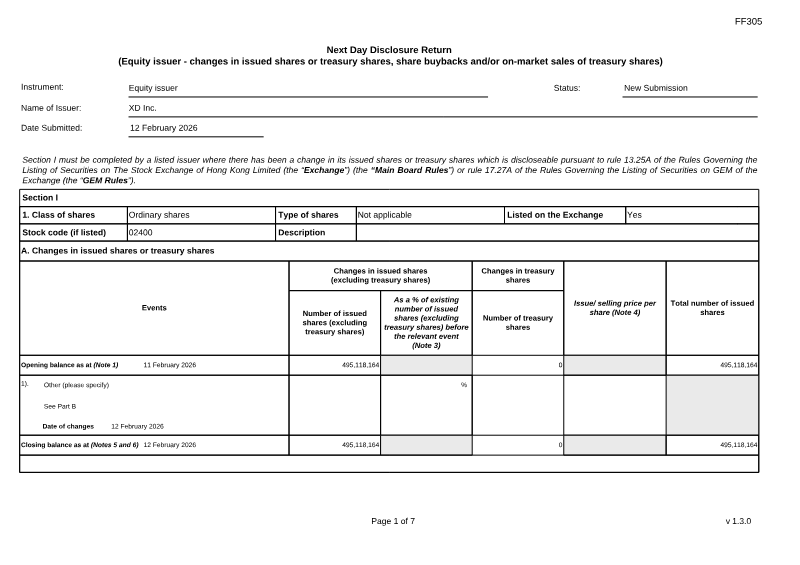

XD

Kingsoft Corporation

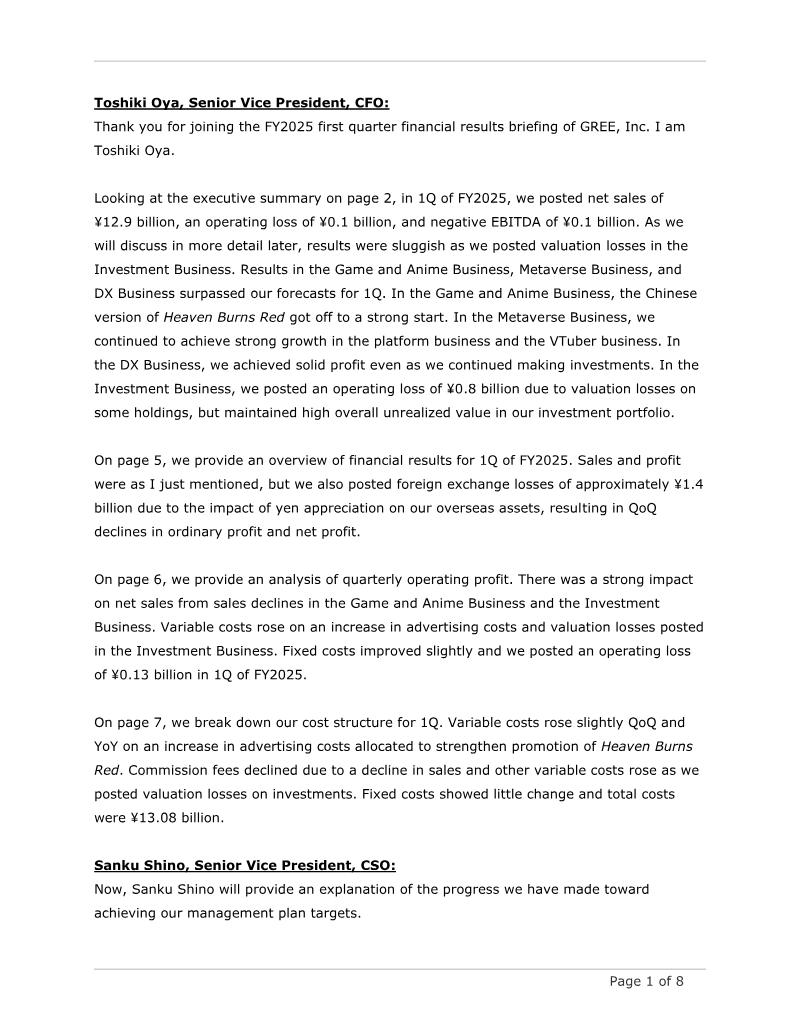

GREE

Tencent Holdings Limited

Tencent

IGG

Niko Partners · 2026

Giant Network Group · 2026

Archosaur Games · 2026

Nippon Ichi Software · 2026

Stock Exchange of Hong Kong · 2026

Stillfront Group · 2026