IGG Inc. is a global developer and operator of online games, specializing in the free-to-play model where revenue is primarily generated through the sale of virtual items. Headquartered in Singapore with significant research and development operations in the People’s Republic of China, the company maintains a diverse portfolio of browser, client-based, and mobile titles. The primary purpose of the prospectus is to facilitate the company’s listing on the Growth Enterprise Market (GEM) of the Stock Exchange of Hong Kong, with an offering of 327,434,000 shares expected to raise between HK$588.4 million and HK$711.9 million. These proceeds are earmarked for marketing, strategic acquisitions, and the expansion of development teams to support the company’s transition toward mobile gaming.

The company has demonstrated strong financial growth, with revenue increasing by 42.9% in the first five months of 2013 compared to the same period in 2012. While historical financial statements reflected net losses due to the fair value accounting of redeemable convertible preferred shares, these instruments were converted to equity by May 2013, resulting in a significantly improved balance sheet and a shift to a net current asset position. Despite this growth, the company faces substantial operational risks, including a high concentration of revenue within a small number of titles, reliance on third-party platforms like Facebook and mobile app stores, and the inherent volatility of the global gaming market.

To navigate PRC foreign investment restrictions, the company employs a series of structured contracts to maintain control over its domestic operating subsidiary, Fuzhou Tianmeng. While legal counsel has confirmed the enforceability of these arrangements, they remain a point of regulatory uncertainty. Furthermore, the company must manage complex tax compliance issues across multiple jurisdictions, including potential changes to its preferential tax status in Singapore and China. Following the listing, controlling shareholders will retain over 30% of the issued share capital, and the company will continue to operate under a governance framework designed to mitigate conflicts of interest and ensure ongoing regulatory compliance.

IGG · 2025

IGG · 2024

IGG · 2023

IGG · 2023

IGG · 2022

IGG · 2022

IGG · 2020

IGG · 2020

IGG · 2019

IGG · 2019

IGG · 2018

IGG · 2017

IGG · 2013

GREE

Giant Network Group · 2026

Archosaur Games · 2026

InvestGame · 2026

Nippon Ichi Software · 2026

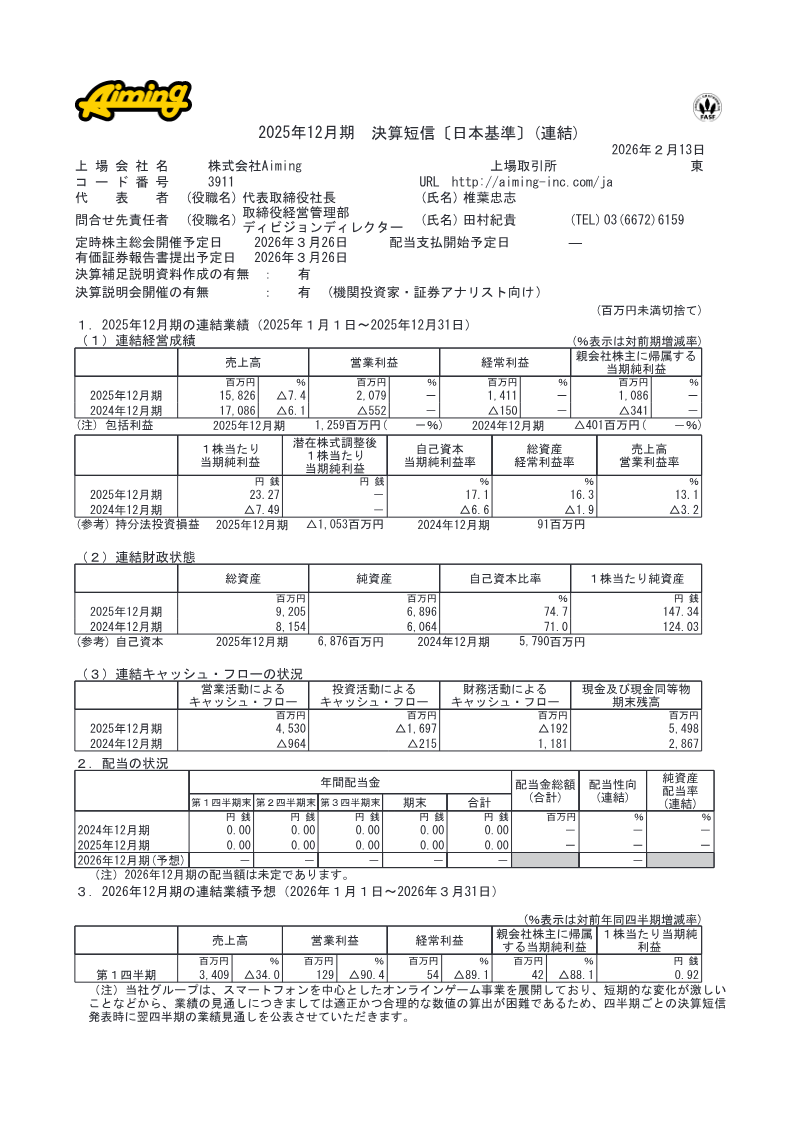

Aiming · 2026

Stillfront Group · 2026

Meridian Play · 2026

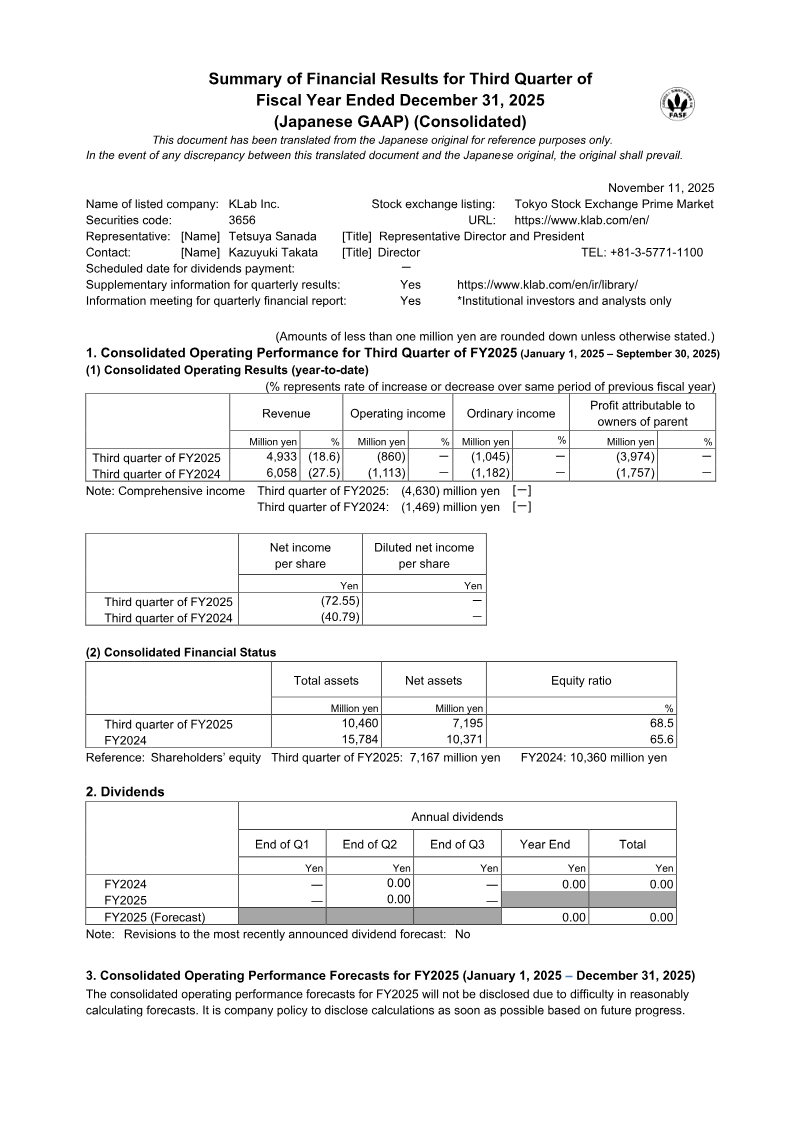

KLab · 2025

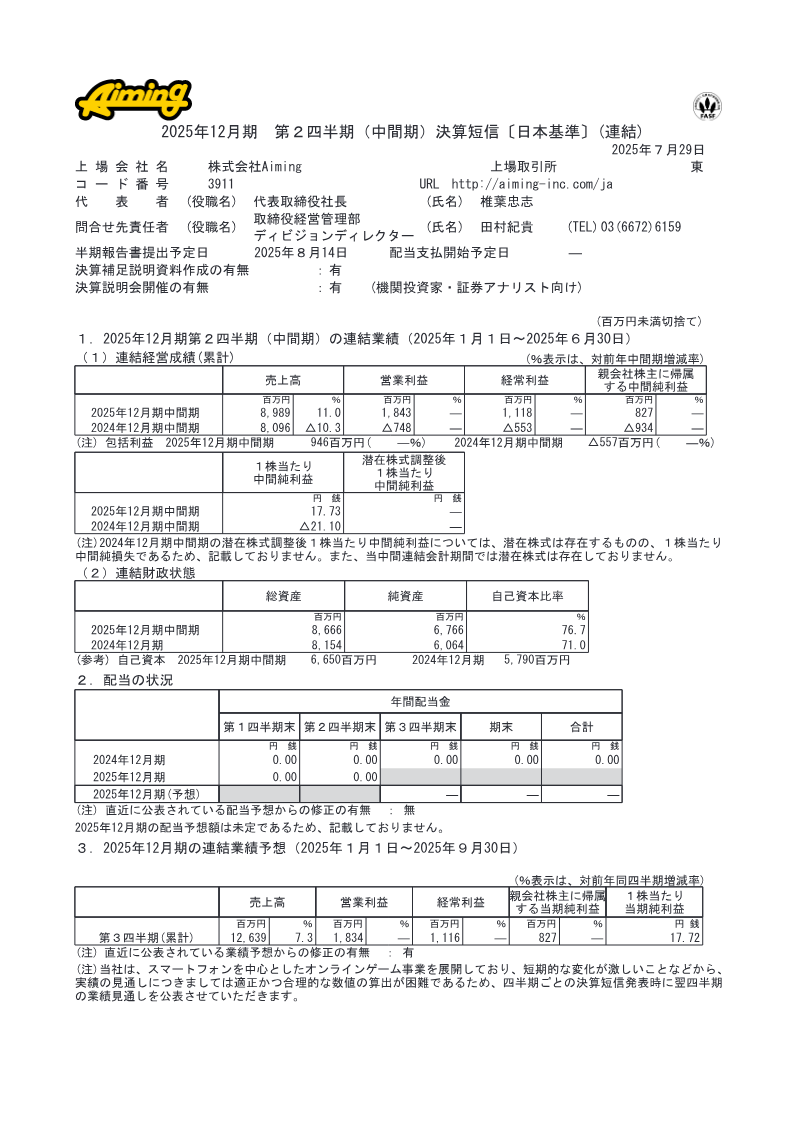

Aiming · 2025

PCF Group · 2025