FinancialTencent Holdings Limited

Interim Results: Six Months Ended 30 June 2007

62 pages~89 min full read

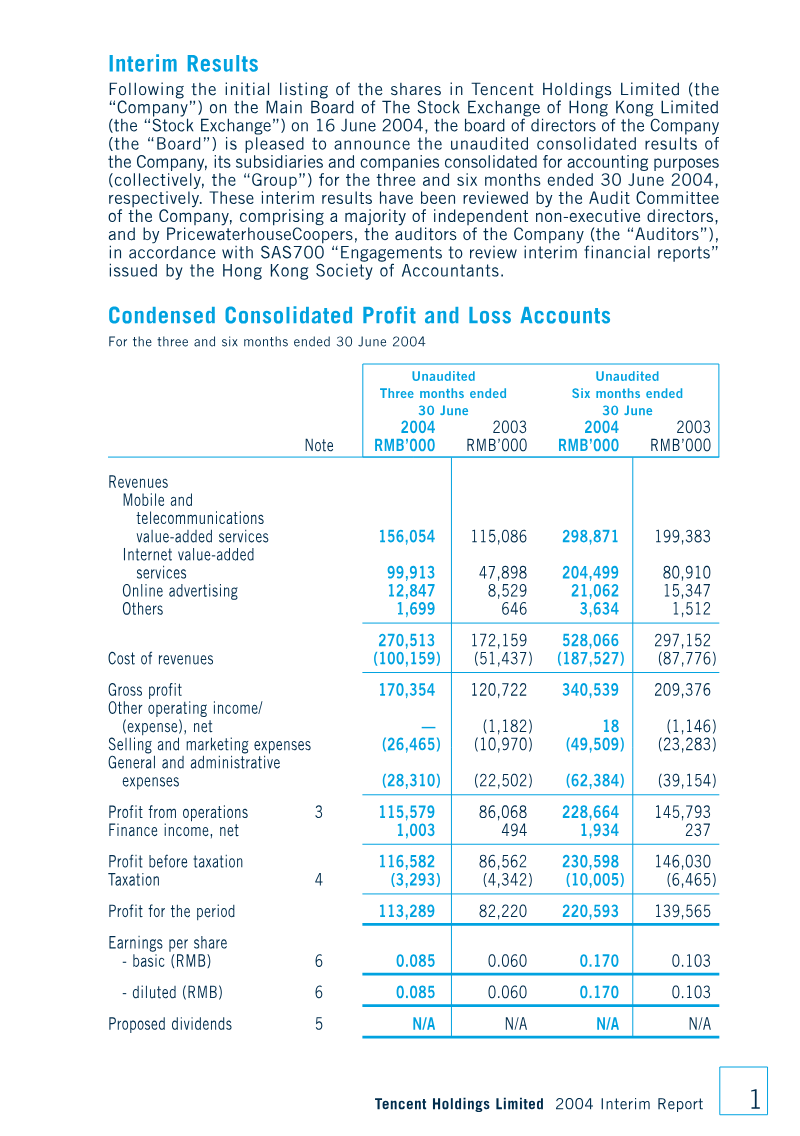

Tencent demonstrated robust financial and operational growth during the first half of 2007, characterized by a 21.5% year-over-year revenue increase to RMB 1.64 billion. Profitability remained strong, with the company reporting a net profit of RMB 624.7 million for the period. This performance was primarily fueled by significant gains in internet value-added services and a notable 54.7% surge in online advertising revenue. These core segments successfully offset the impact of a more challenging regulatory environment for mobile and wireless services, which necessitated stricter account security measures and resulted in a decline in mobile value-added service subscriptions.

Operational expansion remained a central focus throughout the first half of the year, as the company grew its workforce to 3,296 employees and increased its issued share capital to 1.78 billion shares. Infrastructure investments and rising staff costs contributed to total expenses of approximately RMB 1.01 billion, yet the company maintained a healthy profit margin of 38.5% during the second quarter. The platform’s reach continued to scale, with registered instant messaging accounts climbing to 647.1 million and fee-based internet value-added service subscriptions rising by 16.7% to 17.5 million.

Looking forward, the company is positioned to leverage seasonal summer demand and an expanded pipeline of new game launches to sustain its growth trajectory. Despite regulatory headwinds in the mobile sector, the firm maintains a stable corporate governance structure, with MIH QQ (BVI) Limited holding a 35.36% stake. By prioritizing the monetization of its massive user base and continuing to refine its equity-based incentive schemes, the organization remains focused on balancing aggressive business expansion with the operational demands of a rapidly evolving Chinese internet market.

Tencent

XD

Tencent

Kingsoft Corporation

GREE

Tencent

Tencent

Tencent

IGG

Niko Partners · 2026

Giant Network Group · 2026

Archosaur Games · 2026