FinancialXD

Monthly Return of Equity Issuer on Movements in Securities: May 2026

10 pages~8 min full read

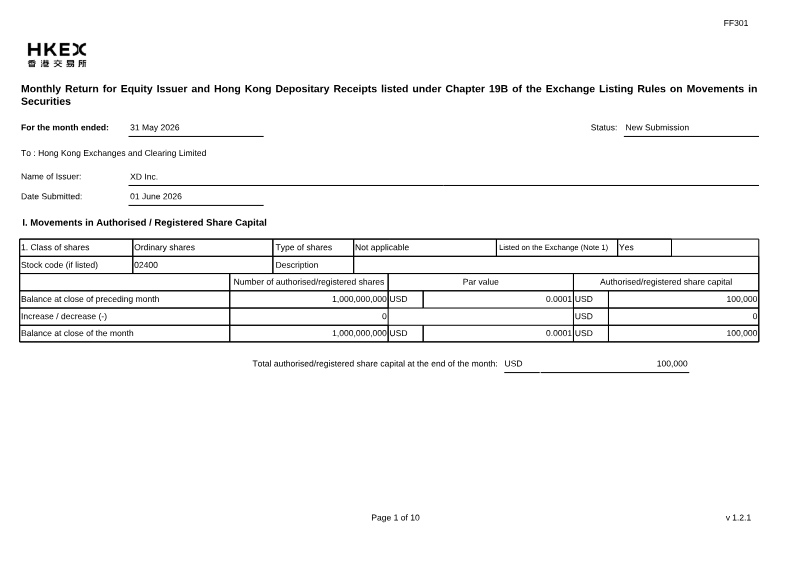

The submission reports the equity movements of XD Inc. for May 2026, detailing authorised capital, issued shares, treasury holdings, and public float compliance. Authorised share capital remained unchanged at 1 billion ordinary shares with a nominal value of HKD 0.0001, equating to USD 100,000 in authorised capital. Issued shares decreased from 492,433,164 to 489,302,364, a net reduction of 3,130,800 shares, all of which were ordinary shares. Treasury share balances stayed at zero throughout the month.

Share‑option activity under a plan adopted in June 2021 contributed 5,200 new ordinary shares to the issued pool, raising HKD 172,858. Concurrently, share repurchases and cancellations reduced the issued count by 3,136,000 shares; 285,000 of these were repurchased but not yet cancelled as of May 31, and 3,136,000 shares were repurchased and cancelled on May 19. No other convertible or alternative share‑issuance mechanisms were employed.

Public float sufficiency was confirmed, with the company meeting the 25 % minimum threshold based on total issued shares excluding treasury holdings. The issuer affirmed that all board authorisations, regulatory compliances, and financial settlements related to the movements were satisfied. No new listing conditions or legal filings were outstanding beyond routine corporate obligations.

Overall, XD Inc.’s May 2026 equity activity involved a modest net dilution from option exercise offset by significant share repurchases, maintaining compliance with Hong Kong Exchange listing rules and preserving adequate public float.

Tencent

Tencent

IGG

Tencent

GREE

Tencent Holdings Limited

Tencent

Kingsoft Corporation

Tencent

Niko Partners · 2026

Giant Network Group · 2026

Archosaur Games · 2026