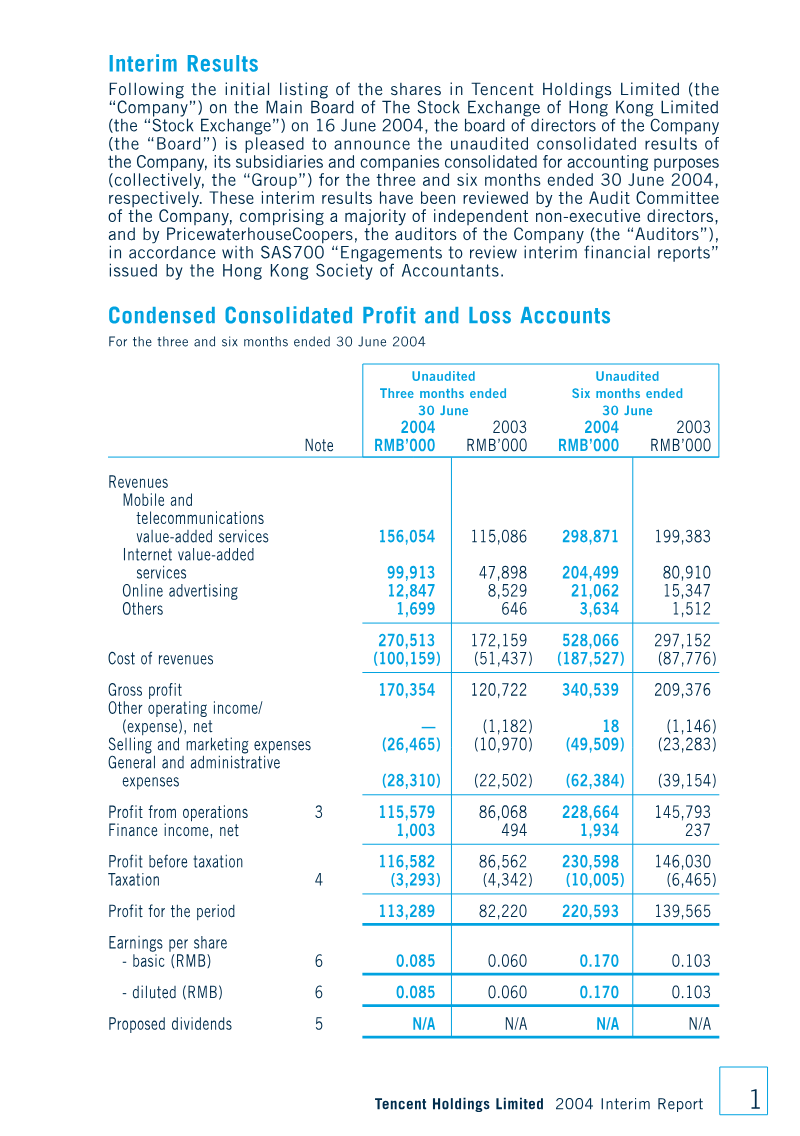

Tencent Holdings Limited’s 2006 annual report demonstrates a dramatic expansion of its internet‑based business, with total revenues rising 96.3 % to RMB 2,800 million and net profit increasing 119 % to RMB 1.06 billion. Growth is driven primarily by a 132 % increase in Internet value‑added services and a 136 % jump in online advertising, while mobile/telecom services also contributed significantly. Operating profit surged to RMB 1.16 billion, and the net margin improved from 34 % to 38 %. Cash and investments totaled RMB 3.22 billion, largely in U.S. dollar‑denominated assets that expose the group to Renminbi appreciation risk.

The company’s financial health is reinforced by a strong balance sheet: total assets rose to RMB 1.77 billion, and the group maintained no interest‑bearing borrowings as of year‑end. Shareholder value initiatives included a final dividend of HKD 0.12 per share, the repurchase and cancellation of 18.4 million shares during 2006, and a cumulative share buyback of over 32 million shares since its IPO. Governance structures feature a board with executive, non‑executive and independent directors, audit and remuneration committees, and compliance with Hong Kong listing rules. Key executives hold significant share positions through BVI entities, while Naspers‑controlled MIH QQ holds 35.6 % of issued shares.

Geographically, operations are concentrated in mainland China (≈70 % of segment assets), with subsidiaries and customers spread across Asia, Africa, and the Mediterranean under Naspers’ umbrella. The report covers fiscal year 2006, detailing revenue streams from internet services, mobile telecoms, and online advertising, and outlines accounting policies such as IAS 39 adoption, fair‑value measurement for available‑for‑sale securities, and share‑based compensation recognition. Overall, Tencent’s 2006 performance reflects rapid scaling of core digital services, robust profitability, and a commitment to shareholder returns within a growing but still low‑penetration Chinese internet market.

Tencent · 2024

Tencent · 2024

Tencent · 2022

Tencent · 2021

Tencent

Tencent

Tencent

Tencent

Tencent

Tencent

Tencent

Tencent

Giant Network Group · 2026

Tencent Holdings Limited

Pearl Abyss · 2026

Archosaur Games · 2026

Kakao Games · 2026

Aream & Co · 2026

Meridian Play · 2026

Kakao Games · 2025

Niko Partners · 2025

Meridian Play · 2025

Konvoy · 2024

Niko Partners · 2020