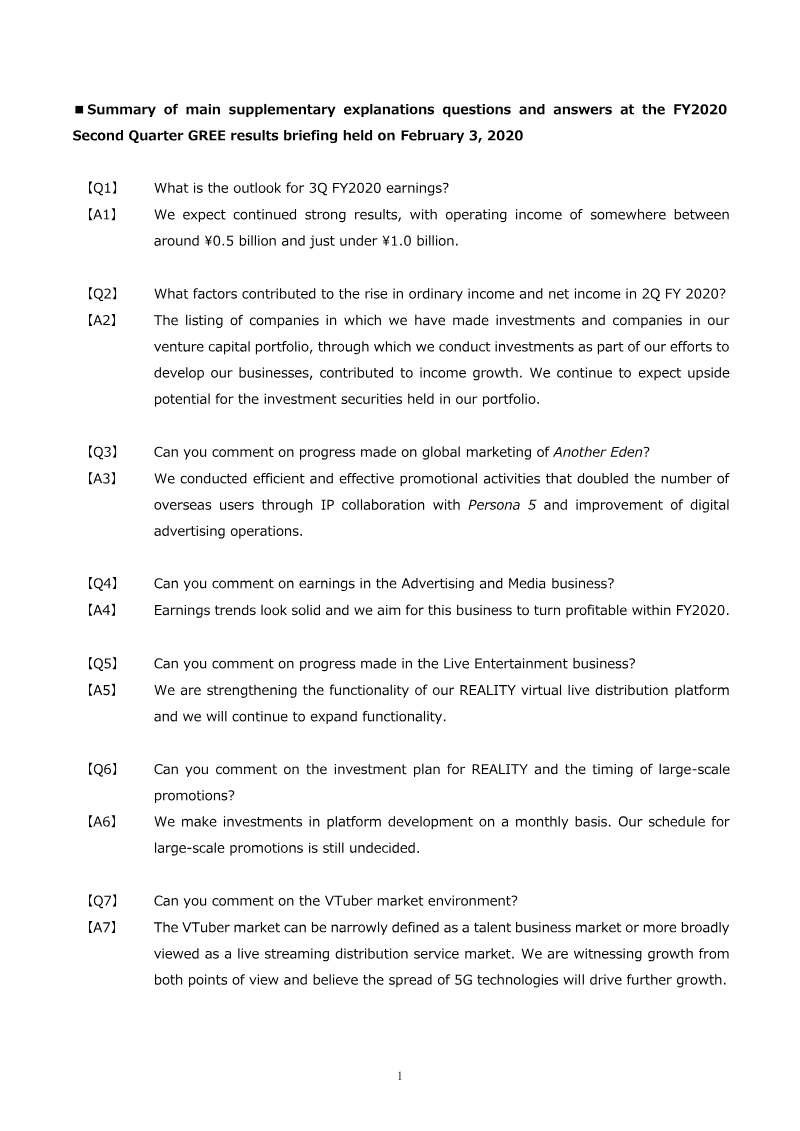

Mobile

Report

FY2026 Second Quarter Financial Results Briefing

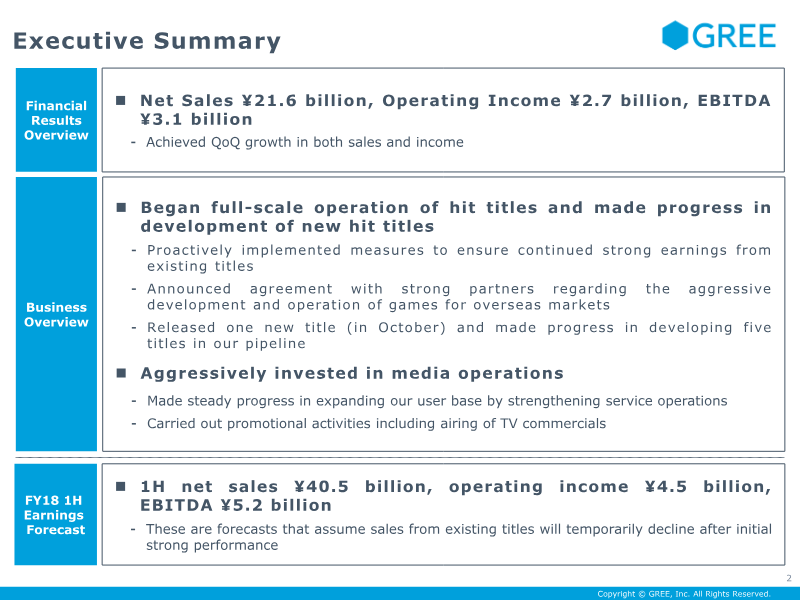

The briefing presents FY2026 second‑quarter results for GREE Holdings, emphasizing four core segments—Game, VTuber, IP, and DX—and the Investment Business. Consolidated net sales reached ¥12.7 billion, operating profit stood at ¥0.4 billion, and ordinary profit rose to ¥0.58 billion, the latter boosted by foreign‑exchange gains from yen depreciation. Segment analysis shows net sales of ¥12.1 billion and operating profit of roughly ¥0.6 billion, with variable costs flat at ¥4.0 billion but fixed costs climbing by ¥0.63 billion due to labor, rental, and outsourcing expenses linked to console game development and VTuber production. Operating profit fell from ¥1.11 billion in Q1 to ¥0.59 billion, reflecting higher fixed costs despite a modest sales increase of ¥0.15 billion. The Game Business delivered ¥7.1 billion in sales and ¥0.5 billion in operating profit, turning profitable after a prior negative forecast; live‑service titles and upcoming console releases are highlighted. VTuber sales hit a record high, with operating profit at ¥0.2 billion; the Production Business grew 50% QoQ, driven by events and commerce. IP sales rose 41% QoQ to ¥0.5 billion, with anime distribution and new smartphone game launches cited as key drivers. DX sales were ¥1.84 billion with operating profit of ¥0.18 billion, noting a shift toward recurring‑earnings models and planned roll‑up M&A. Full‑year forecasts adjust sales downward due to Game Business trends but lift operating profit expectations to ¥4.4 billion, surpassing the initial ¥3.6 billion forecast through cost control. Medium‑term targets remain unchanged, aiming for a profit bottom in FY2026 followed by growth from FY2027 onward. The Investment Business recorded moderate distributions but incurred valuation losses, with a long‑term positive cumulative profit outlook and IRR above benchmarks.

GREE

Report

FY2026 1Q Financial Results Briefing: GREE Holdings

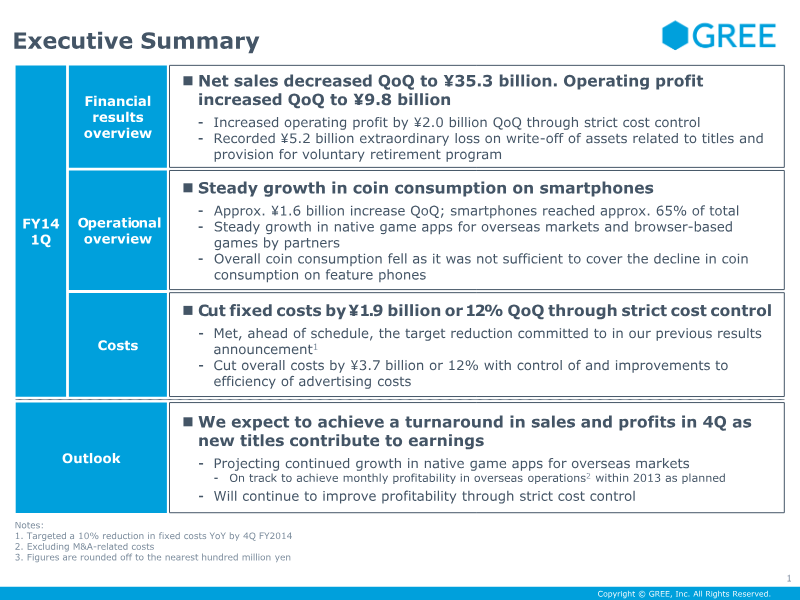

The briefing presents FY2026 1Q financial results for GREE Holdings, emphasizing a re‑segmentation of the former Metaverse Business into distinct Platform and Production units under the VTuber umbrella. Net sales reached ¥12.0 billion with operating profit of ¥1.1 billion, surpassing FY2025 full‑year expectations; consolidated figures including the Investment Business were ¥12.8 billion in sales and ¥1.1 billion in operating profit, buoyed by foreign‑exchange gains from yen depreciation and investment security sales. Variable costs fell due to lower advertising spend and commission fees, while fixed costs remained stable. Segment‑level analysis shows the Game Business experiencing a temporary sales dip from declining momentum of recent titles, yet operating profit rose thanks to overseas development contracts and a live‑service game pipeline. The VTuber Business recorded a 9 % YoY sales increase and a 142 % jump in operating profit, driven by cost controls on payment processing and gradual profitability of the Production arm. The IP Business saw modest sales decline and sharper profit erosion, with Anime and Entertainment Solution units posting delayed revenue but expected to normalize in the second half. The DX Business maintained a gradual uptrend, with consulting projects offsetting outsourcing declines. Forecasts for 2Q FY2026 anticipate sales growth but a profit decline due to console‑game development expenses. Full‑year FY2026 projections expect profits to exceed initial targets, with medium‑term goals unchanged: a profit trough in FY2026 followed by rebound in FY2027–FY2028, and a focus on recurring revenue models and M&A to drive long‑term growth.

GREE