Back to Library

Summary

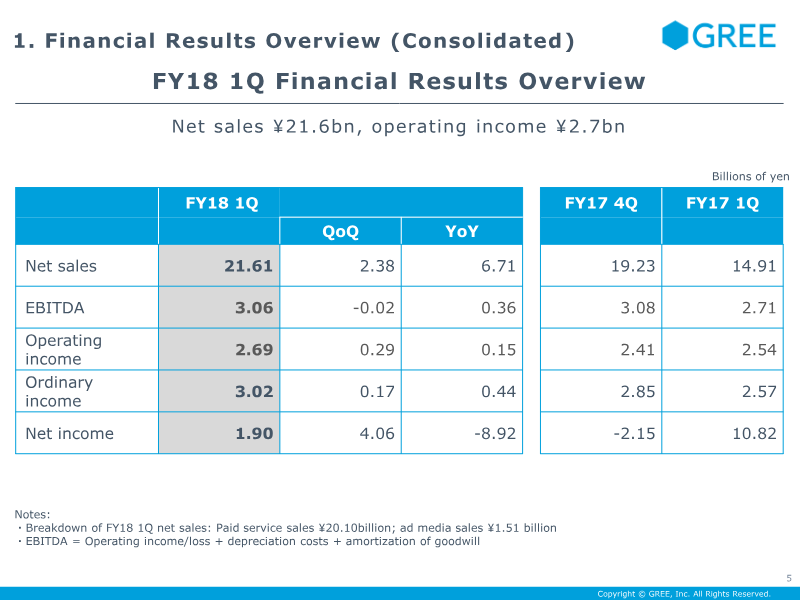

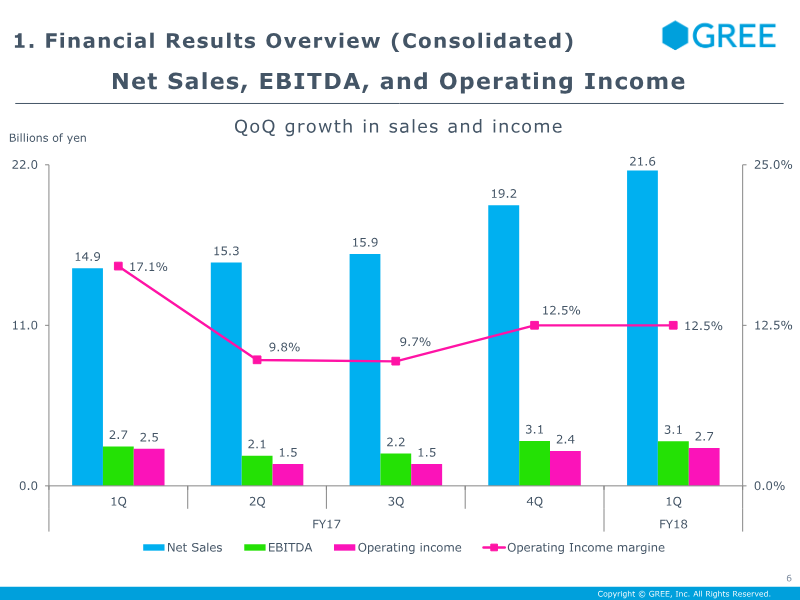

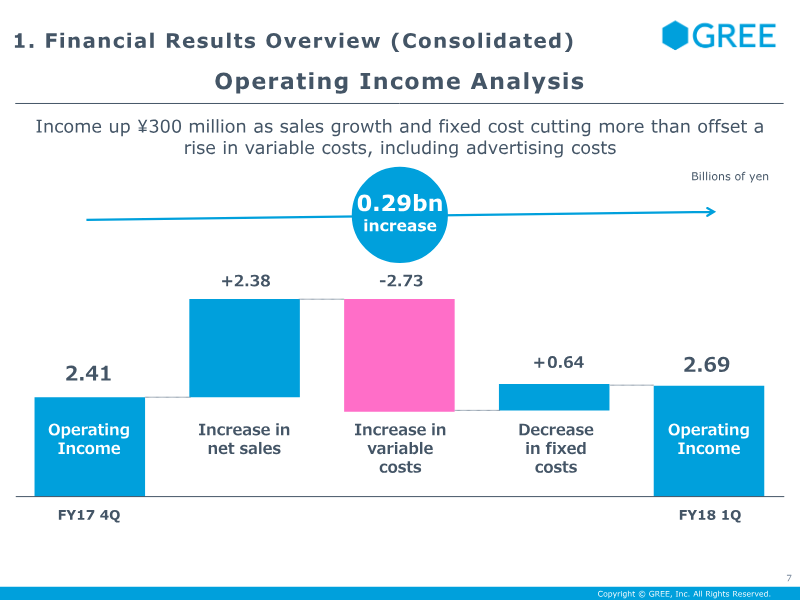

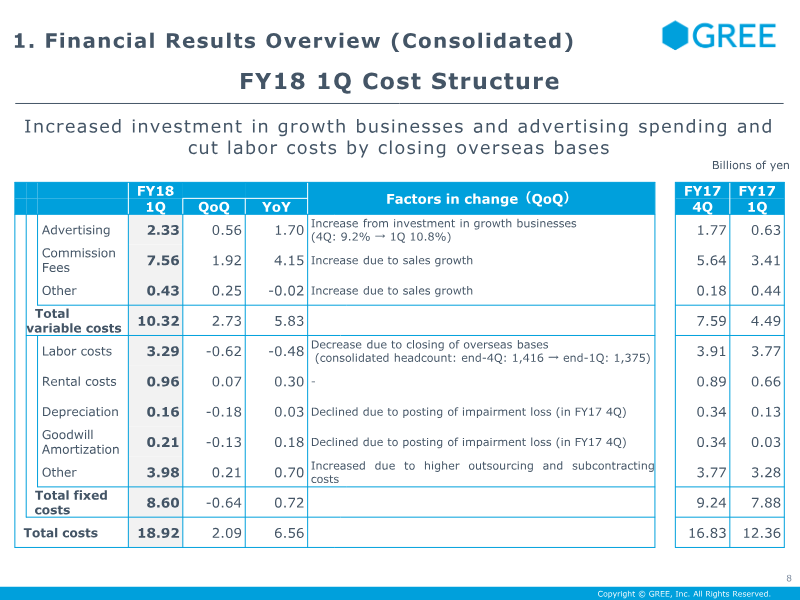

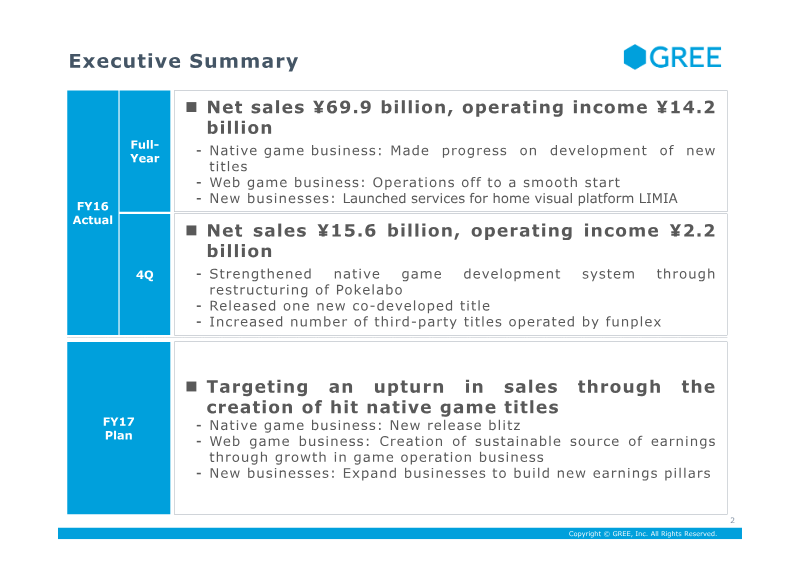

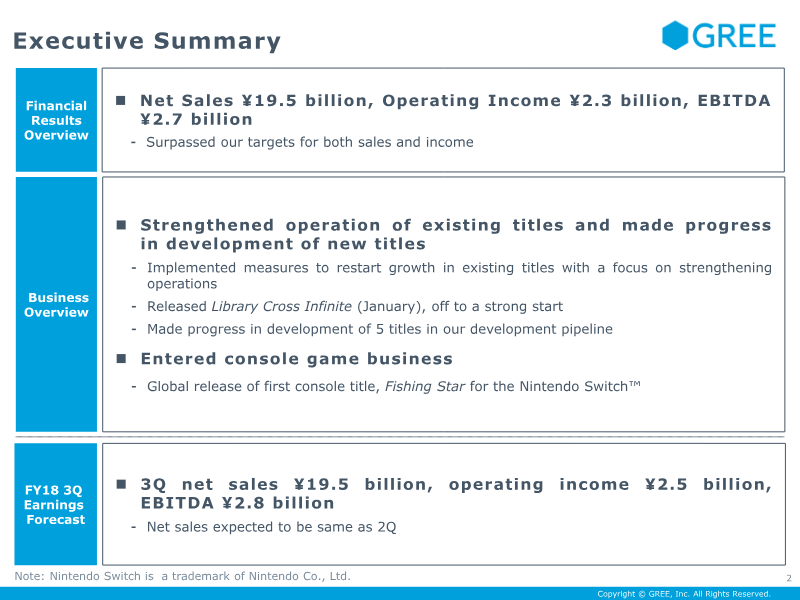

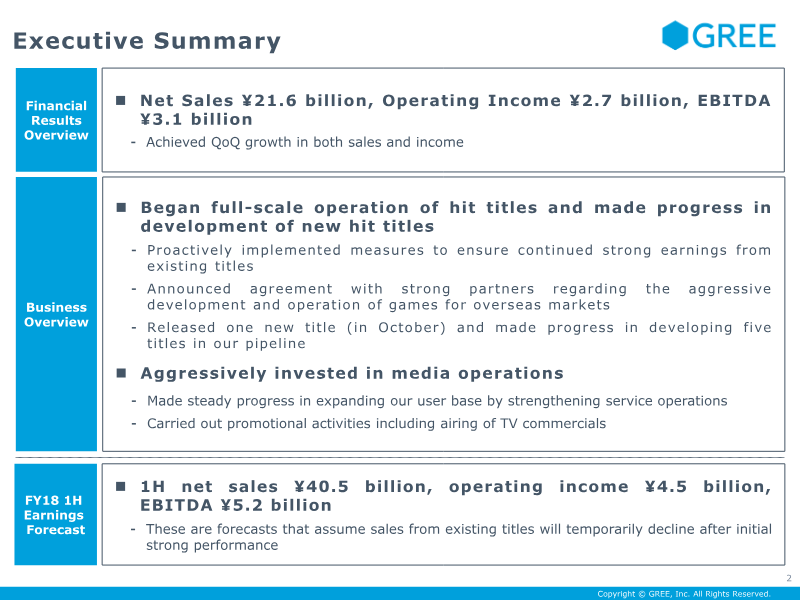

The quarterly results demonstrate a robust first‑quarter performance for FY2018, with net sales reaching ¥21.6 billion and operating income of ¥2.7 billion, reflecting a 17.1 % year‑over‑year increase and a 25 % quarter‑on‑quarter rise in sales. EBITDA stood at ¥3.1 billion, up from a negative figure the previous quarter, underscoring improved profitability after a sharp rebound in operating income. The company attributes growth to full‑scale operation of existing hit titles, aggressive media investment, and the launch of a new title in October. Advertising spend surged to ¥2.33 billion, driven by media‑operations expansion and promotional activities such as TV commercials, while labor costs fell due to overseas base closures. Financial forecasts for the first half of FY2018 project net sales of ¥40.5 billion and operating income of ¥4.5 billion, assuming a temporary dip in sales from mature titles and conservative earnings targets for new releases. The company plans continued investment in advertising to support high‑growth business segments. Operationally, the native game portfolio expanded from one released title to five in development, including first‑party and third‑party IPs. Existing titles received major updates and large‑scale collaborations, boosting coin consumption to 15 billion units in the quarter. The advertising and media arm reported a 2.4× QoQ increase in page views, driven by the LIMIA app’s growth to over one million monthly active users. Geographically, revenue is split between domestic and overseas markets, with overseas operations contributing a growing share of sales. The company’s headcount totaled 1,424 employees across game entertainment, advertising, and corporate functions. Overall, FY2018 Q1 results indicate strong top‑line momentum, improved profitability, and a strategic focus on expanding both domestic and international market presence.

Tags

Pages

View all

Citation

Citation

Generating citation...

Similar Documents

Report

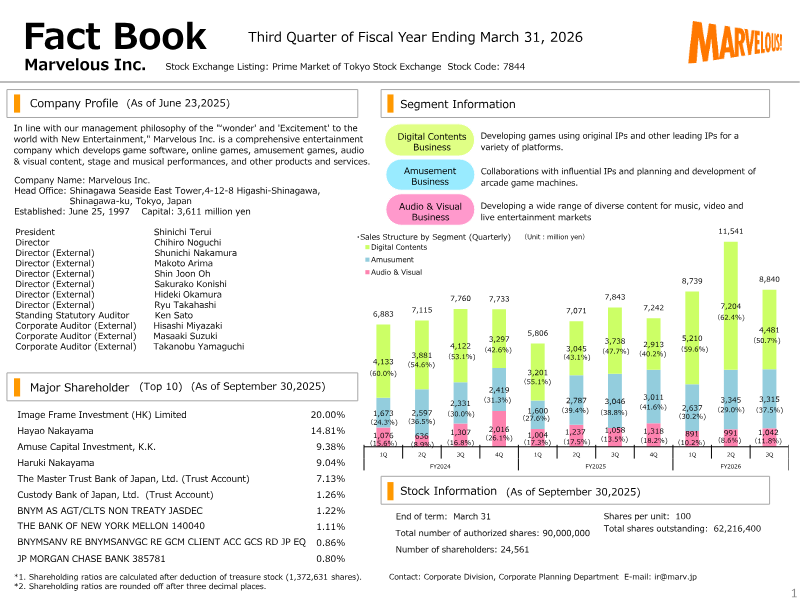

Factbook: Third Quarter of Fiscal Year Ending March 31, 2026

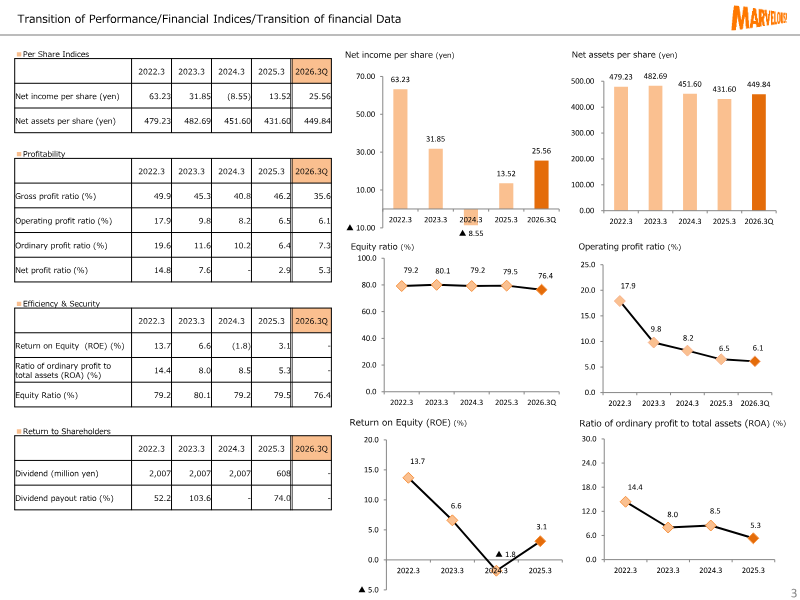

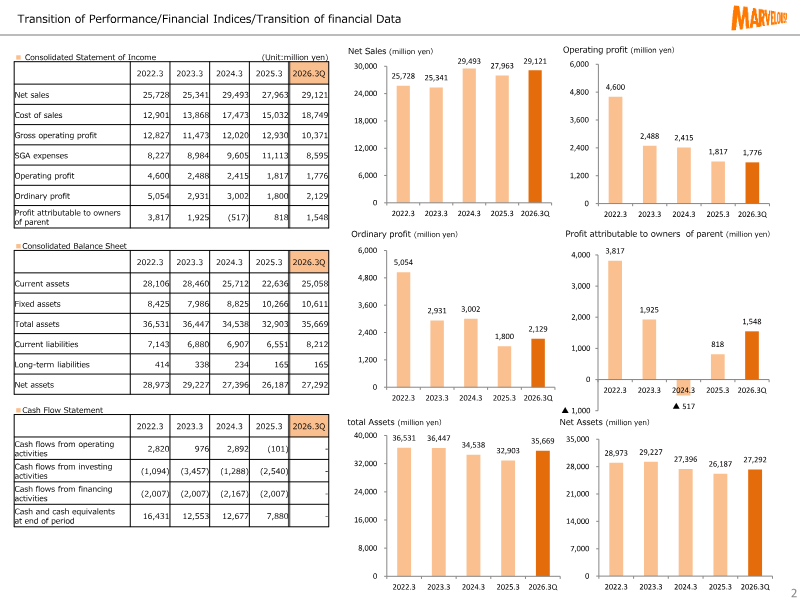

Marvelous Inc., listed on Tokyo’s Prime Market, released its third‑quarter financial results for the fiscal year ending March 31 2026. The company’s core business spans digital content, amusement, audio‑visual production and live entertainment, with a focus on original IPs and collaborations. Revenue rose to ¥29.1 billion in Q3, up 4.5% from the prior quarter and 10.6% year‑on‑year, driven primarily by digital content sales of ¥7.2 billion and amusement revenue of ¥3.0 billion. Gross operating profit reached ¥10.4 billion, a 12% increase over Q2 and a 9% rise versus the same period last year, reflecting improved cost control in production and marketing. Operating profit fell to ¥1.8 billion, a 12% decline from Q2, largely due to higher selling‑general‑administrative expenses of ¥8.6 billion compared with ¥7.9 billion in Q2. Net income attributable to shareholders was ¥1.5 billion, down 18% from Q2, with a net profit margin of 5.3%. The company’s cash‑flow position remained solid, with operating cash flow of ¥2.8 billion and a cash‑equivalent balance of ¥16.4 billion at quarter end. Geographically, the report covers Japan and overseas markets where Marvelous operates. The data derive from consolidated financial statements prepared under Japanese GAAP, covering all subsidiaries and affiliates. Key metrics such as return on equity (13.7%) and asset turnover (0.82) indicate healthy profitability, while dividend payout remained at 52% of net income. Overall, the quarter shows revenue growth but margin pressure from higher operating costs, prompting management to focus on cost efficiency and portfolio diversification.

Marvelous

Report

FY2020 1Q Financial Results Presentation

The presentation reports fiscal year 2020 first‑quarter results for a Japanese entertainment company. Net sales reached 15.8 billion yen, operating income was 1.2 billion yen and EBITDA 1.3 billion yen, surpassing the mid‑to‑high hundred‑million yen forecast and maintaining a stable operating margin despite a quarter‑on‑quarter sales decline driven by post‑anniversary event effects and the transfer of some game titles to improve profitability. Cost controls, particularly a 1.5 billion yen reduction in advertising and outsourcing expenses, offset the sales drop and kept operating income flat. An extraordinary income from equity issuance related to a listing event contributed positively to net income. Geographically, the company expanded its flagship title “DanMachi” into 27 European markets and continued global distribution in Japan, Asia, North America, and Europe. The live‑entertainment segment launched a reality virtual platform, hosting festivals and new program formats to broaden content offerings. The advertising and media arm focused on strengthening community engagement through targeted campaigns and anime tie‑ins, while the game development pipeline aimed to release two new titles in FY 2020 and plan four to six additional releases for FY 2021. Methodologically, the figures derive from consolidated financial statements and internal cost‑tracking systems. The outlook for Q2 projects operating income around 0.5 billion yen, with increased advertising spend to activate promising titles and a continued decline in browser game revenue. The company’s investment securities, notably the Bushiroad listing, are expected to continue appreciating in value.

GREE